Innventure: The Latest Iteration Of A Decades-Long Grift Propped Up By A Fake 300MW Data Center Deal

Summary

- Innventure (NASDAQ: INV) is a self-described “technology commercialization company” that licenses promising but undeveloped technologies from multinational corporations (“MNCs”) and then builds and operates companies around those technologies. Bulls believe 75%+ of Innventure’s ~$538 million valuation is based on its “crown jewel” portfolio company, a liquid cooling startup called Accelsius, built around IP sourced from Nokia.

- In 2025, Accelsius reported just ~$1.5 million in revenue, primarily from demonstration units. Last November, however, it signed a landmark agreement to deploy its tech across a 300MW AI Data Center campus in Ontario on behalf of Canadian company DarkNX. Management has assured shareholders that DarkNX is a “vertically-integrated and funded AI data center developer” and that the deal will pave the way to a $100 million annualized revenue run rate and positive cashflow by the end of 2026.

- We believe the DarkNX deal is a complete fabrication and that Accelsius has booked zero significant commercial deals. We believe that DarkNX itself is a shell company, and we see the announcement as the latest iteration of a 5-year attempt to convince investors that Accelsius has explosive revenue growth potential… just around the corner.

- A 300MW AI Data Center campus would represent one of the largest new builds in all of Canada, requiring billions in funding, a large and experienced team, dozens of contractors, significant back-and-forth with local governments and community stakeholders, resulting in significant media coverage. We found zero evidence this project exists or that DarkNX has the team or funding to even contemplate such a project.

- DarkNX was incorporated just 12 months before Accelsius’s deal announcement out of a single-family home in a Toronto suburb, according to Ontario corporate records. It has no discernible presence in the data center industry or commercial operations of any type. It has just 9 employees on LinkedIn who have no visible experience in the data center industry, and many of whom appear to have other full-time jobs.

- Innventure’s management claims that DarkNX is “funded,” implying that it has access to billions in funding needed to complete the 300MW data center campus. Yet, DarkNX shows zero signs of having access to institutional funding: It has no outside board members, has not made any funding announcements, and Canadian lien records do not reveal any secured interest on its assets, implying it has no current commercial relationships with lenders.

- DarkNX’s website featured a “partner” page that listed companies like Dell, Schneider Electric and Supermicro. When we contacted Dell’s press team, they told us that DarkNX was not “currently within our formal partner program” while Schneider Electric said “our global and North America team are not aware of any partnership or relationship.” Likewise, Supermicro told us it “does not currently have a direct relationship with DarkNX.”

- Former Accelsius employees were skeptical of the deal, with one saying that “this is not a real win” and that they “would not make a business decision based on this announcement.” The former employee explained that DarkNX’s “data center” in Mississauga appeared to be a “trucking terminal or something like that.”

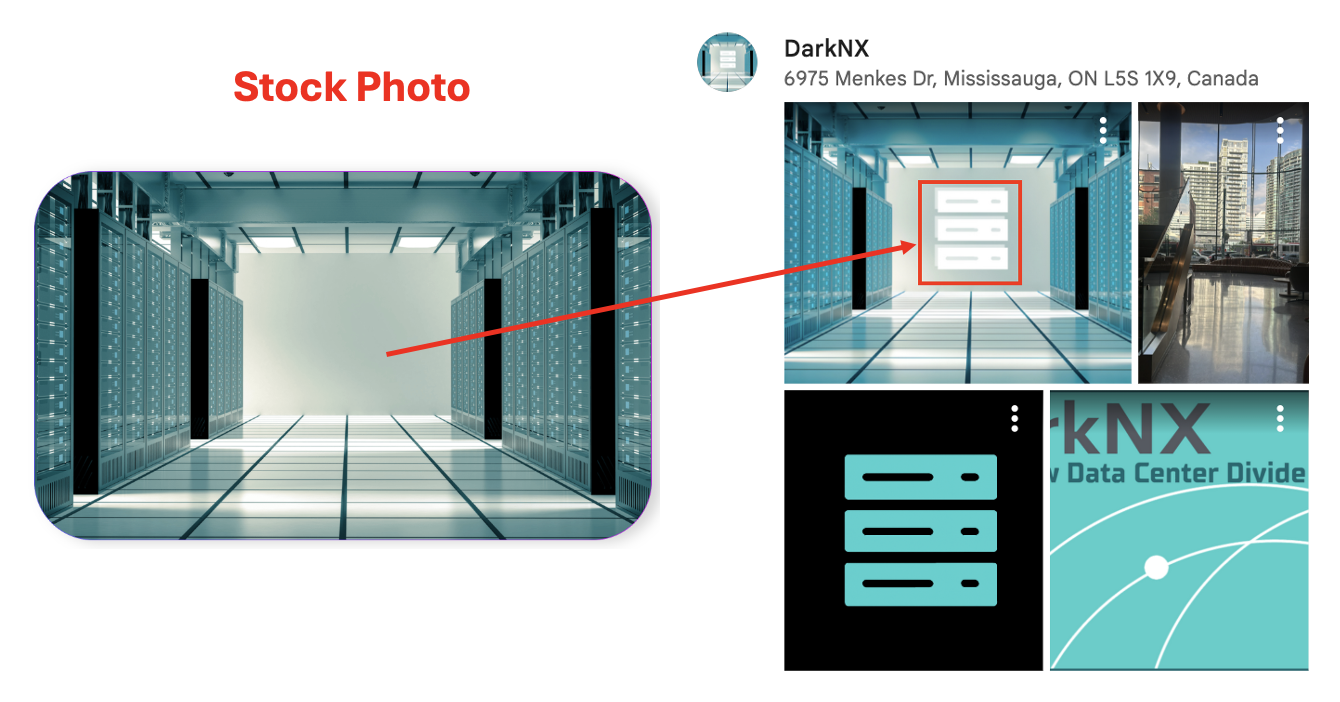

- Corroborating the former Accelsius employee’s claims, DarkNX’s Google page features an address in Mississauga, Ontario, for a supposed “data center.” DarkNX appears to have uploaded a stock photo of futuristic-looking servers to Google with an obviously photoshopped DarkNX logo in the background.

- We checked this address and found a commercial trucking company where the founder of DarkNX worked for a few months nearly 8 years ago. We called the trucking company, and they had never heard of DarkNX and confirmed they do not share their space with any other company.

- A second former Accelsius employee told us: “I think, you know, we've never heard of the company, they don't have customers, there's no data center. This isn't like another known entity … So there's just a lot of obvious, missing pieces it feels like. That's the skepticism I think you're maybe detecting from a lot of us.”

- DarkNX has made laughably impossible claims on its website, including having “998 GW” of data center capacity – which would require enough electricity to power ¾ of the United States. DarkNX also claimed it has distributed 3 million MVA of power equipment - which would make it one of the largest providers of such equipment on the planet.

- Its website also features a “case study” of an 85MW deployment where DarkNX supposedly handled the entire project from permitting to commissioning over a 25-month period. This timeline would indicate the project started 8 months before DarkNX was even incorporated. This case study includes zero real details and, in our view, bears the hallmarks of AI-generated copy and seems to be a complete fabrication.

- DarkNX appears to be the latest gimmick in a years-long attempt to lure investors into the Accelsius story. According to a former Innventure executive, management was using “false information” and revenue projections that were “pure fiction” to solicit investments into Accelsius as far back as 2021, before the Nokia deal was even closed. According to the former executive, management described the Nokia tech as “useless for any real commercialization” as far back as 2022.

- Leading into its SPAC deal, Innventure claimed in its registration statements that it had multiple “revenue-generating” deals to deploy to “operating data centers” by mid-2024. When the SEC asked Innventure to file exhibits with more details on these deals, Innventure walked back its claims and admitted that none of the deals were “material” and that some were just MOUs.

- In its first annual report as a public company, Innventure’s auditor BDO highlighted a material weakness related to “forecasts for Accelsius,” an oddly specific and uncommon call-out from an auditor, in our experience. 4 months later, Innventure dismissed BDO in favor of WithumSmith - an auditor infamous for “widespread quality control” failures in SPAC audits.

- During the last two earnings calls, management continued to tout huge deals, citing “real production orders” in the 8-figure and even 9-figure ranges. Despite these supposed wins, we are skeptical that any other deals exist, with a former Accelsius employee telling us "I'm not aware of anything like that" and "I don't think they're anywhere near mass production conversations."

- Innventure executives Bill Haskell, Mike Otworth, and John Scott paid themselves $31.2 million in total compensation in 2024 and 2025 despite reporting just $3.2 million in revenue, $371 million in net losses, and increasing share count by 88.4% in just ~18 months. In 2026, they paid themselves an “earnout” bonus of 2 million shares that was unlocked by Accelsius signing its first large commercial deal. We believe this was based on the DarkNX deal.

- As soon as the lock-up agreement expired, and a month before the DarkNX deal was publicly announced, Innventure’s largest shareholder began dumping shares and has now exited at least ~60% of his position and is now under the threshold for public reporting.

- Activist investors have aggressively and publicly criticized Innventure’s management team for excessive executive compensation, rapid shareholder dilution, and overall poor governance. They believe, however, that Innventure’s stake in Accelsius makes the stock attractive nonetheless. We think they are vastly overestimating Accelsius’s commercial prospects, and severely underestimating the governance risks associated with this management team.

- Since the ‘90s, Innventure’s senior executives, including John Scott, Michael Otworth and Bill Haskell, have founded numerous technology companies, many of which touted groundbreaking technology, blue-chip partnerships, and the imminent arrival of hockey-stick revenue growth. Virtually all of these companies failed spectacularly, resulting in numerous bankruptcies, delistings, and blow-ups that wiped out shareholders. We think Innventure will end the same way.

Initial Disclosure: After extensive research, we believe the evidence justifies a short position in shares of Innventure Inc (NASDAQ: INV). Morpheus Research holds short positions in INV. This report represents our opinion, and we encourage all readers to do their own due diligence. Please see our full disclaimer at the bottom of the report.

Introduction & Background: A Technology Incubator Leveraging A Proprietary “DownSelect” Strategy To Identify, License, And Commercialize Tech From Multinational Corporations

Innventure, Inc. (NASDAQ: INV) is a technology incubator that leverages a supposedly proprietary “DownSelect” process to identify and license promising but undeveloped tech from multinational corporations (“MNCs”), around which it then builds companies.

Innventure believes this strategy enables them to earn the high returns associated with venture capital investing, but with a lower risk profile.

Innventure executives John Scott, Bill Haskell, and Mike Otworth first pioneered this strategy in the ‘90s and early 2000s with the formation of XL Vision and XL TechGroup, technology incubators that “created the foundational business building methodology upon which Innventure is based,” according to the company’s annual report.[1]

John Scott was the founder and CEO of XL Vision and XL TechGroup, according to his LinkedIn profile. Bill Haskell was a co-founder and President of XL Vision and XL TechGroup, according to Innventure’s annual report. Mike Otworth was an early hire of XL Vision and was “CEO of multiple start-ups at XL TechGroup,” according to his bio. ↩︎

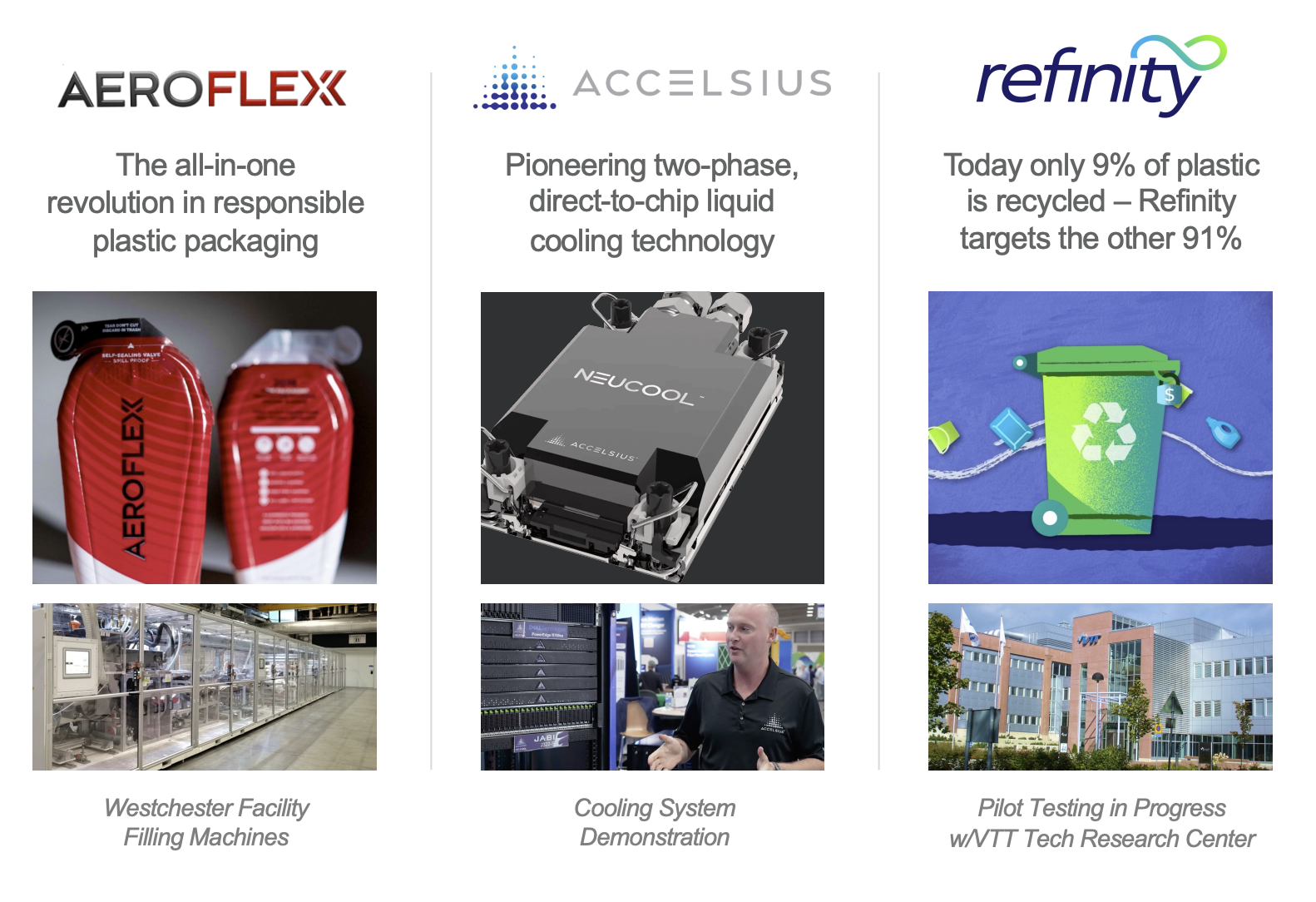

Innventure is primarily focused on commercializing its 3 portfolio companies: AeroFlexx, Accelsius, and Refinity. These companies supposedly has breakthrough technology, blue-chip partners, and management would like you to believe that they are on the cusp of parabolic revenue growth.

Bulls See Accelsius As The “Crown Jewel” Of Innventure’s Portfolio Due To Its Blue-Chip Backers And A Landmark Deal To Deploy Its Industry-Leading, Liquid-Cooling Technology Across A 300MW AI Data Center Mega Campus In Ontario

Innventure reported just ~$1.4 million in Q1 2026 revenue with a pre-tax net loss of ~$20 million, but management claims that its operating companies are experiencing "commercial momentum” that it believes will “translate into strong revenue and adjusted EBITDA growth” in the second half of this year:

“We are now seeing third-party validation at our operating companies, resulting in commercial bookings, operational scale and clear milestone achievement across the entire enterprise.” — CEO Bill Haskell, Q1 2026 Earnings Call

Despite management’s bullish commentary regarding all of its operating companies, sell-side analysts ascribe little value to Refinity and Aeroflexx and instead appear primarily focused on Accelsius.[1]

Roth Capital, April 28, 2026 Innventure update, says “we derive the majority of our valuation from Accelsius.” The same update had a 12-Mo. Price Target of $16.00. ↩︎

Founded in 2022 on IP licensed from Nokia, Accelsius is focused on commercializing a liquid cooling technology that uses two-phase refrigerants and a direct-to-chip design to deliver superior thermal control for increasingly powerful GPUs in data centers.

Last year, Accelsius reported modest revenues of ~$1.6 million from what Innventure CEO Bill Haskell described as “one-off pilots.”[1]

That seemingly changed in November 2025, when Accelsius announced a landmark agreement with a Canadian data center company, DarkNX, to deploy its liquid cooling tech across a 300 MW AI Data Center campus in Ontario. According to management, the deal provides a clear path to $100 million in annualized revenue run rate by EOY 2026 and cashflow positivity.

Following the data center deal, in December 2025, Accelsius raised $65 million in a Series B round from Johnson Controls (NYSE: JCI) and Legrand (EPA: LR) – valuing Accelsius at $665 million post-money and largely seen as institutional validation of its technology and commercial prospects.

Innventure retains a 43.2% stake in Accelsius, which is seen as the “crown jewel” asset underpinning the vast majority of Innventure’s ~$540-million valuation, with one analyst estimating that the Accelsius stake makes up ~77% of Innventure’s value.[1]

Northland Securities ascribes a $10 valuation to Accelsius without warrant exercise, as part of a total $13 valuation, per its report dated March 31, 2026. In 2025, Innventure reported $1.55 million revenue from its Technology segment, which includes “the business activities of Accelsius,” per Innventure’s financials. ↩︎

Part 1: Accelsius’s Flagship Deal With DarkNX Appears To Be Completely Fake

At 300MW, the DarkNX AI Data Center campus would be one of the largest data center projects in all of Canada. We would expect to see significant media coverage, wide-ranging engagement from community members and local politicians, and a vast array of contractors and third parties coordinating permits, community notices, and grid connection applications.

As an example of the attention given to projects of this magnitude, in March 2026, Canadian Broadcasting Corporation (“CBC”) reported that telco Bell Canada would build a 300MW AI data center in the province of Saskatchewan. The announcement featured the CEO of Bell Canada, the Premier of Saskatchewan and other community leaders, and the project was described as “Canada’s largest AI data center.”

With DarkNX, however, we found zero evidence its project even exists. Further, DarkNX itself appears to be a newly established shell company with no discernible operations, no clear financial backing, and zero experience.

Accelsius’s Flagship Customer “DarkNX” Claims To Be A Vertically-Integrated Data Center Builder-Operator With Dozens Of Data Center Deployments Under Its Belt

Reality Check: DarkNX Is A Newly Established Shell Company Registered Out Of A Toronto Suburban Home With No Discernible Operations And Just ~9 Employees On LinkedIn Who Appear To Have Zero Experience In The Data Center Industry

Innventure CEO Haskell has described DarkNX as a “vertically-integrated data and funded AI data center developer.”

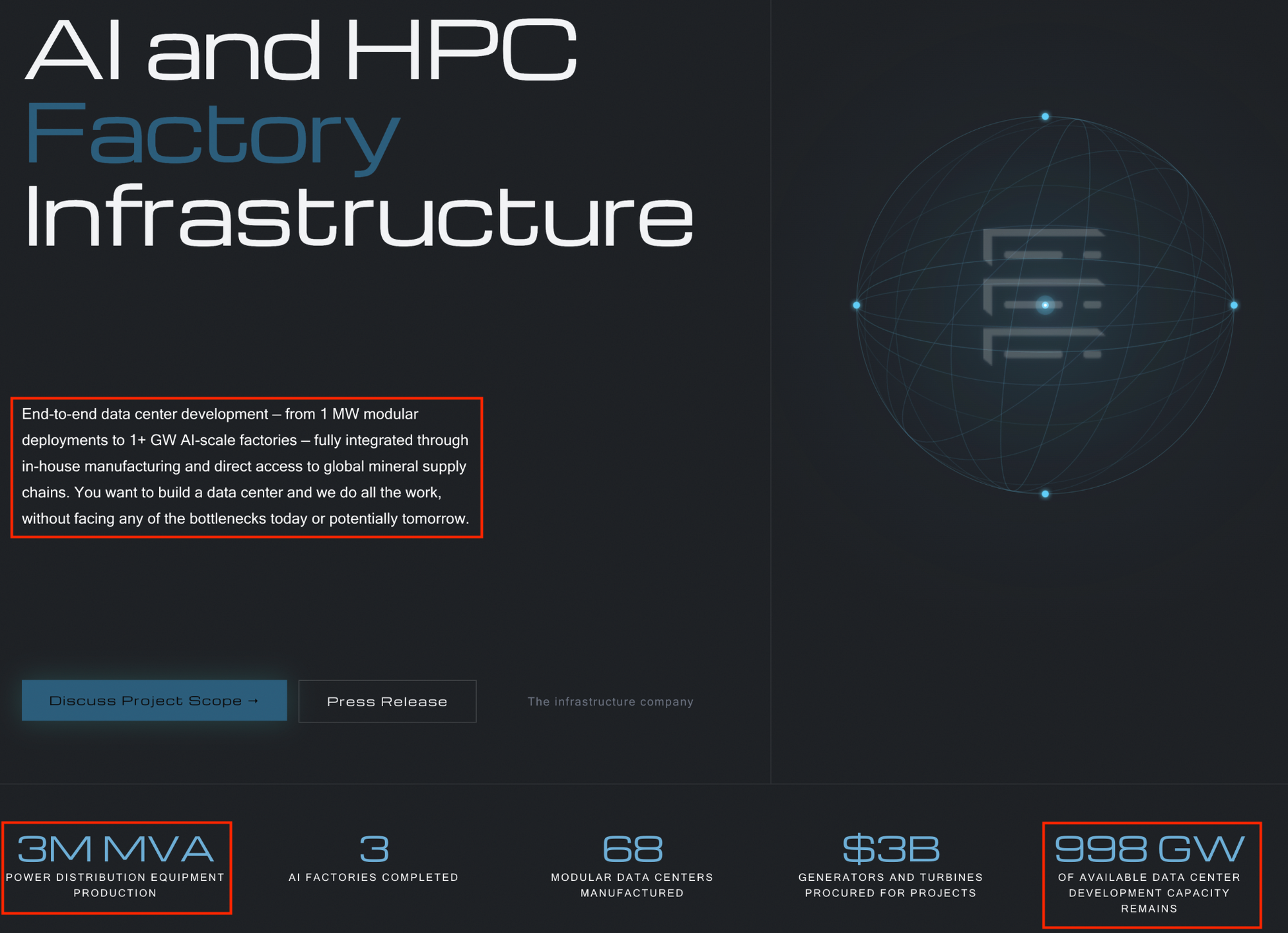

At first glance, this description seems plausible, with DarkNX’s website claiming it is an “end-to-end data center development” with “in-house” manufacturing, capacity for gigawatt-scale AI data centers, 68 modular data centers manufactured, and 156 MW of “AI Factories” deployed.[1]

Industry experts, however, seem unable to ascertain details about DarkNX or its team. For example, the day after the DarkNX deal announcement, leading industry publication Data Center Dynamics wrote that “few details” about DarkNX or its projects were available.

The analysts who cover Innventure’s stock appear to have the same problem. During Innventure’s Q4 earnings call, one analyst noted that “it’s hard to find information on [DarkNX]” and asked Innventure’s management to provide more clarity around DarkNX’s funding sources.

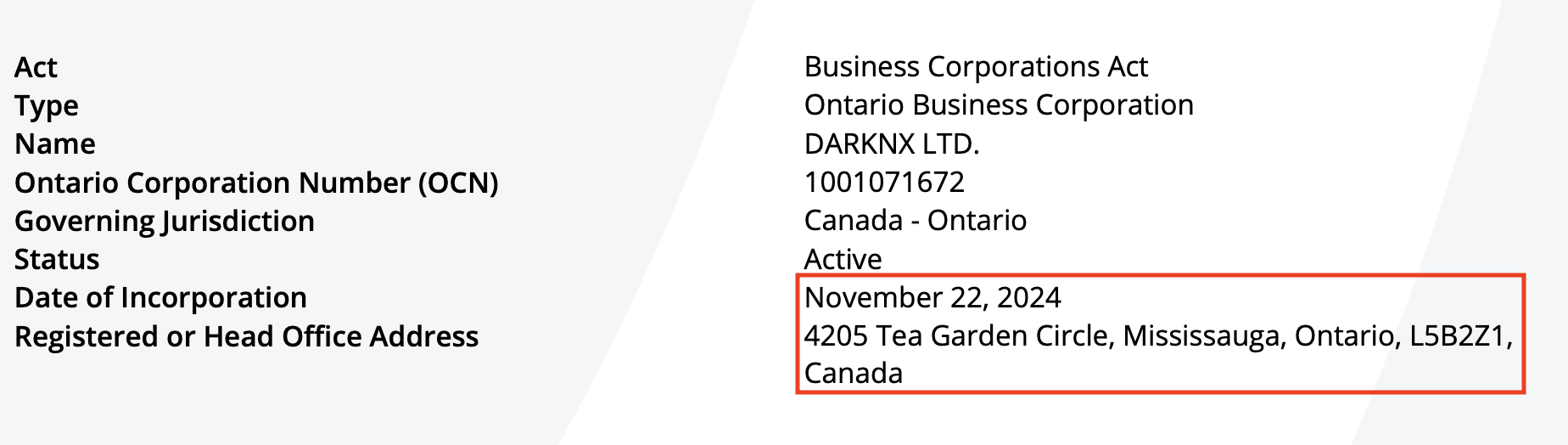

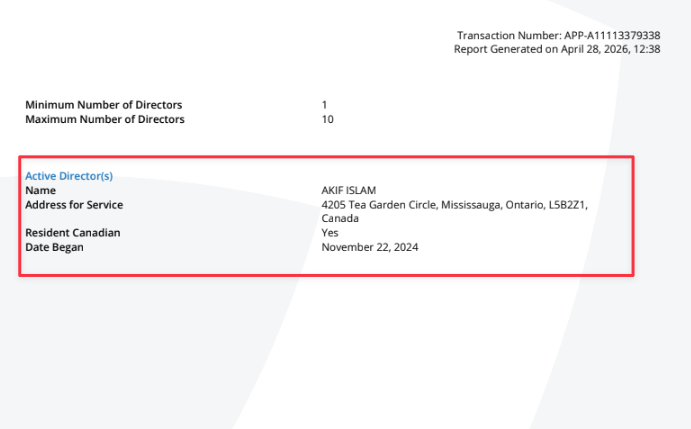

DarkNX was incorporated on November 22, 2024, just 12 months prior to the Accelsius deal announcement, according to Ontario corporate records.

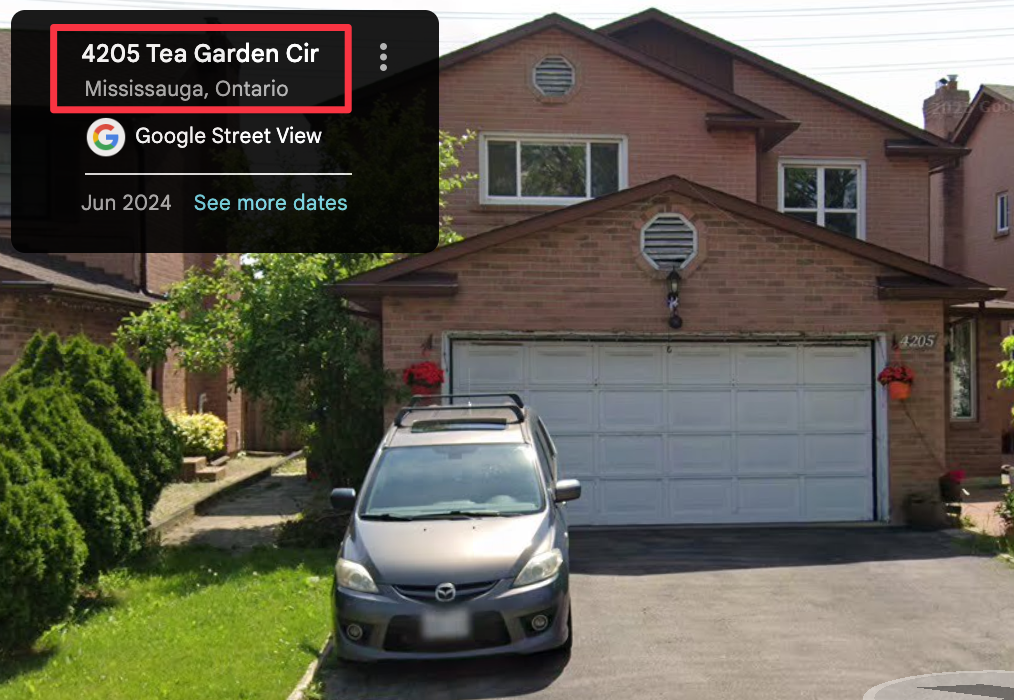

DarkNX current “registered or head office address” leads to a house in a Toronto suburb, according to Ontario’s corporate records.

The property appears to be owned by the family of Isaac Islam, the CEO & Chairman of DarkNX, according to Ontario property records.[1]

Ontario corporate records obtained as of April 28, 2026. Property records obtained as of May 20, 2026. The property was acquired by Syed Masud-Ul Islam and Dil Afrose Islam in 2003, according to Ontario property records. ↩︎

Beyond its corporate records, DarkNX’s website features two addresses for its “Head Offices,” one of which leads to a WeWork in Toronto. The other appears to belong to a small metal fabricator in Seattle called Skyline Electric, which has 11 employees on LinkedIn.

DarkNX appears to be just one of several shell companies founded over the last ~18 months by Isaac Islam, who appears to have zero experience building or operating data centers, per his Linkedin profile. DarkNX’s other 8 employees display zero data center experience on their LinkedIn profiles, and many of them appear to have other full-time jobs.[1]

For example, Arman Salah acts simultaneously as CTO of DarkNX and Chief Business Development Officer for Skyline Electric, the small metal fabricator at the address of the purported US office of DarkNX, per his LinkedIn profile. Shaun Khan’s LinkedIn profile shows that since February 2026, he has been doing “Sales” at DarkNX while he also acts as a Business Activation Specialist for Canadian telco, Rogers. Seena Arjomandi, currently acts as Director of Operations of DarkNX and General Counsel Stealth Foundry, per his LinkedIn profile. ↩︎

Islam also claims to be the founder of TG Venture Partners, which was incorporated in 2025. [Pg. 2] We found no evidence, however, that TG Venture Partners has made a single venture investment, that it has any employees or commercial operations. It has a basic landing page for a website.

Islam also claims to be on the board of Skyridian, a purported “orbital data center” company that was incorporated in California ~7 months ago and which has no other employees on LinkedIn. Its registered member is Arman Salah, who is also DarkNX CTO, per his LinkedIn profile. Furthermore, Skyridian claims that DarkNX is an investor and partner.

DarkNX is thus a part of this constellation of recent, shady entities with no apparent clients, revenue, or real existence outside legal formalities and basic web pages.

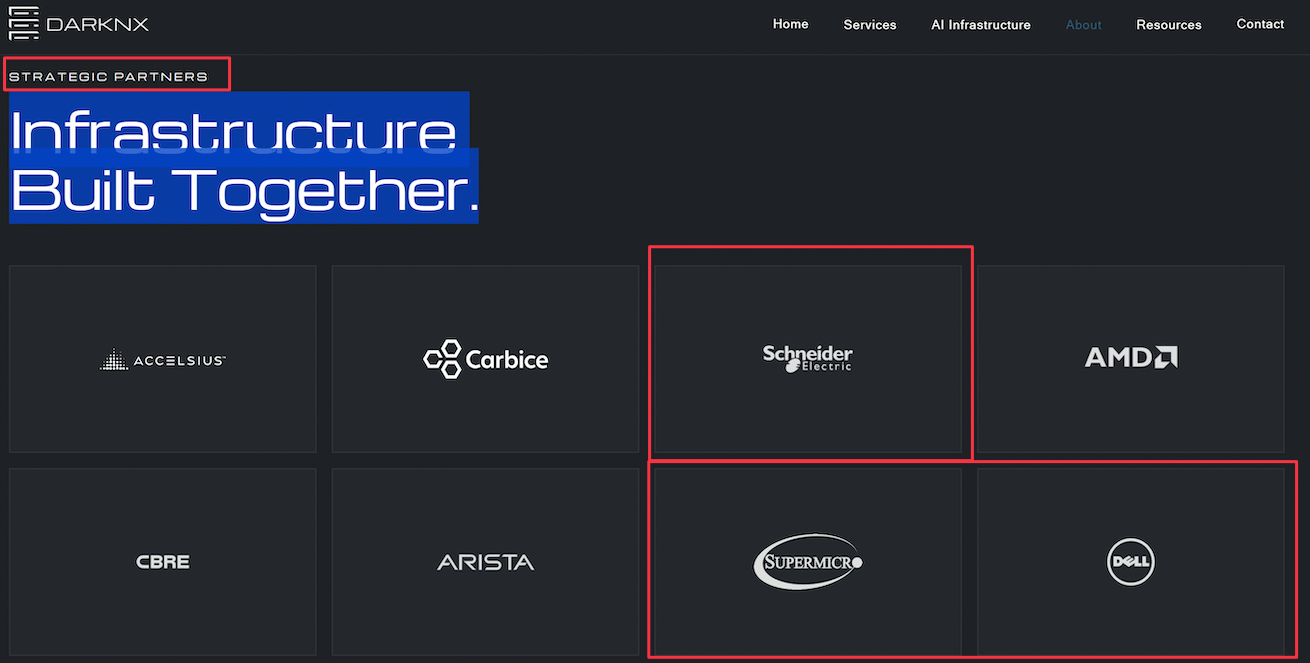

DarkNX’s Website Contains Clearly Fake Marketing Claims, Case Studies That Appear To Be Fabricated, And A “Strategic Partners” Page That Includes Dell, Supermicro, And Schneider Electric, All Of Whom Denied Being Partners With DarkNX

Until A Recent Update, DarkNX’s Website Stated It Was One Of The Largest Producers Of Power Equipment In The World And That It Had “Available Data Center Capacity” Of 998GW, On Par With The Power Needs Of The United States

We believe that DarkNX’s marketing claims are clearly fabricated and that the company’s purported product offerings are likely entirely fake.

Until a recent update to its website, DarkNX’s claimed that it had “power distribution equipment production” of 3 million megavolt-amperes (MVA) and 998GW worth of “available data center development capacity.”

We see these statements as obviously false. MVA represents the power output or capacity of electrical power equipment. “3M MVA” implies 3 million MVA. That figure would exceed the output of the largest producers of power distribution equipment in the world, such as Hitachi Energy.

Meanwhile, its claim of 998GW of “data center development capacity” would require access to ¾ of the United States nameplate generation capacity.

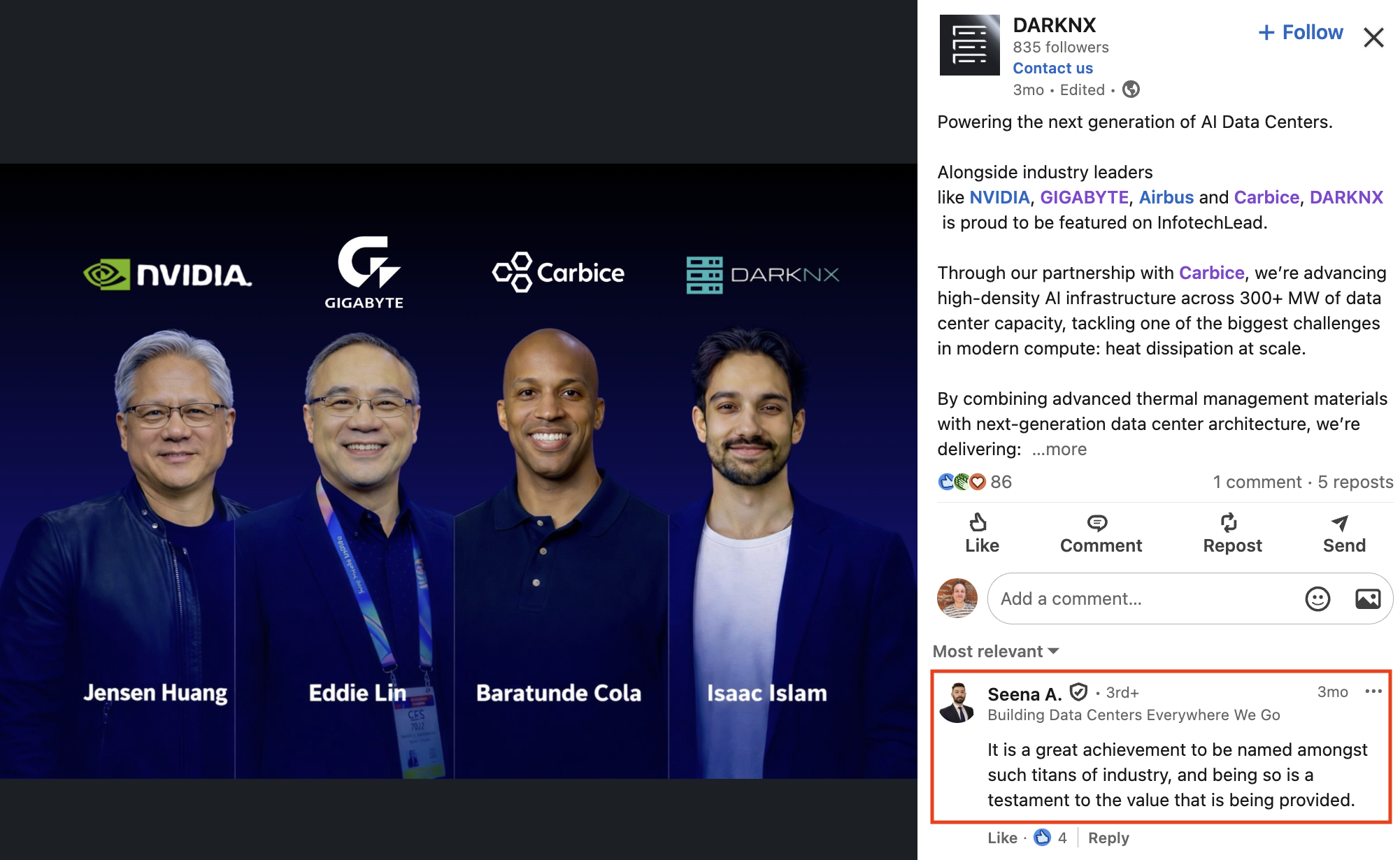

DarkNX’s marketing includes photoshopped pictures of Isaac Islam standing next to Nvidia’s Jensen Huang, with a DarkNX employee commenting that being named “amongst such titans of industry” is a “testament” to DarkNX’s value.[1]

DarkNX’s post followed an article published by InfoTech Lead, an Indian tech news site, that summarized 3 public announcements: (i) an NVDIA-Gigabyte collaboration; (ii) a Palantir-Airbus strategic collaboration; and (iii) a press release issued by Carbice announcing a partnership with DarkNX. The article did not contain an image showing Jensen Huang alongside Isaac Islam. ↩︎

As of mid-May, DarkNX’s website showed companies such as Schneider Electric, Supermicro, and Dell as “Strategic Partners.”

We inquired with the press teams from these companies to confirm whether they were partnered with DarkNX and understand the nature of the partnership.

Dell told us that DarkNX “is not currently within our formal partner program.” Supermicro told us it “does not currently have a direct relationship with DarkNX,” and Schneider Electric said it was “not aware of any partnership or relationship.”[1]

DarkNX’s website also features case studies from what appear to be completely fabricated data center projects. For example, one case study highlights a greenfield deployment of an 85MW site for a hyperscaler, which was allegedly completed in just 25 months, meaning it would have started well before DarkNX was even incorporated.

The case studies contains zero details about the site location or customer, and we found zero media coverage of this supposed build-out. We believe the case studies were done by AI.

We Found Zero Evidence That DarkNX’s 300MW “AI Data Center Campus” Exists

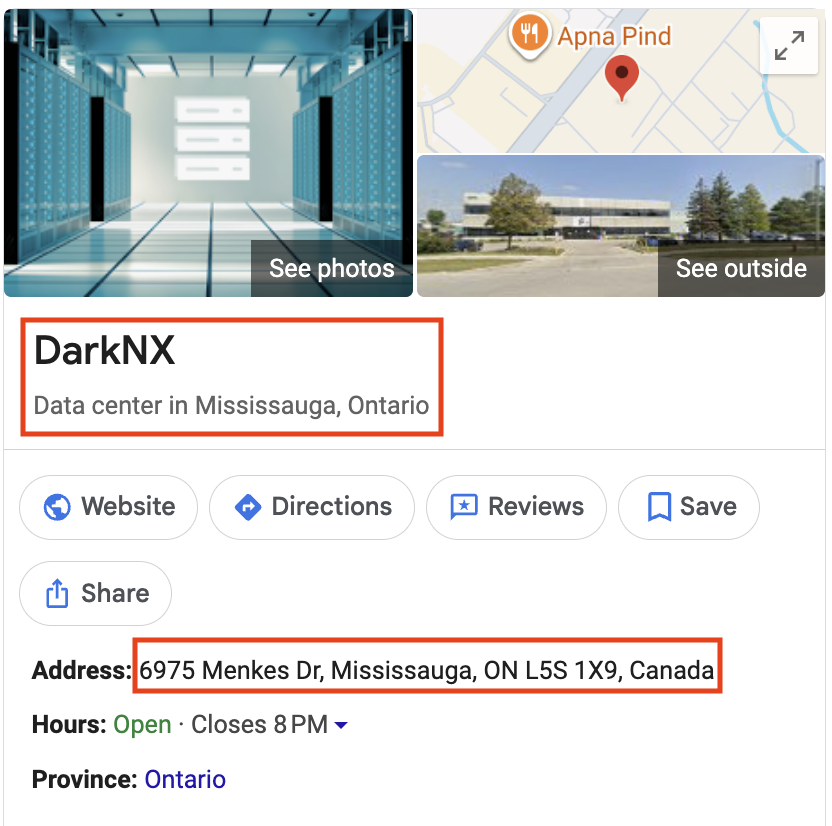

DarkNX’s Google Maps Profile Features Stock Imagery Of A Futuristic Looking Data Center With DarkNX’s Logo Photoshopped In The Background, And The Listed Address Leads To A Trucking Business Where The Founder Of DarkNX Worked For Several Months ~8 Years Ago

Former Accelsius Employee: “Just Look At Who DarkNX Is. 5 Guys And A Dog. If You Look At Their Office Is Mississauga … The Data Center Was At A Trucking Terminal Or Something Like That. It’s Just, It’s Just Not A Real Company.”

Innventure claims that its agreement with Accelsius represents “contracted backlog” and, as mentioned, that DarkNX is a “vertically-integrated and funded AI data center developer” with a “healthy tenant pipeline” for its 300MW AI Data Center campus.

We could not find any evidence that this campus exists, and our skepticism was shared by multiple former Accelsius employees we interviewed, including one who said:

“Just look at who DarkNX is. 5 guys and a dog. If you look at their office in Mississauga … the data center was at a trucking terminal or something like that. It’s just, it’s just not a real company.”

The former Accelsius employee’s reference to Mississauga appears to be corroborated by DarkNX’s Google Maps profile, which describes the company as a “data center” and features an address in Mississauga that ostensibly hosts its data center.

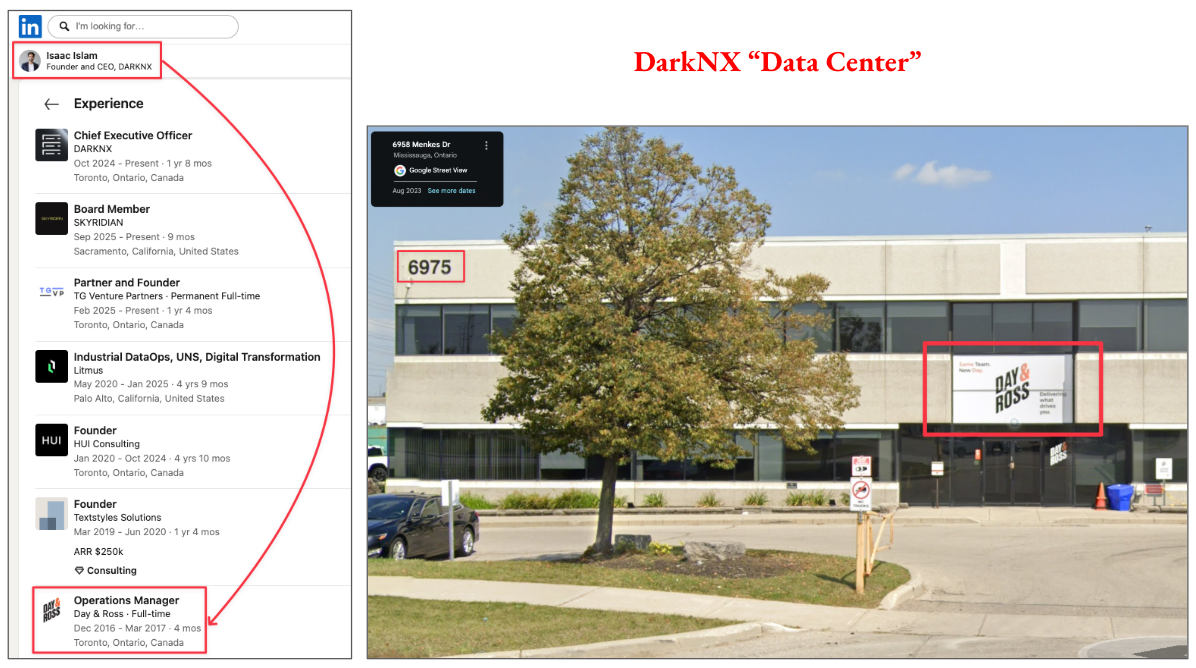

This address, however, leads to a single-tenant commercial building whose sole occupant appears to be a commercial trucking company called Day & Ross, where the founder of DarkNX worked as a manager for ~4 months in 2017, according to his LinkedIn profile.

We called Day & Ross to see if they had sold or leased this facility, or part of it, to DarkNX. They had never heard of DarkNX and confirmed that they do not share their space with anyone.

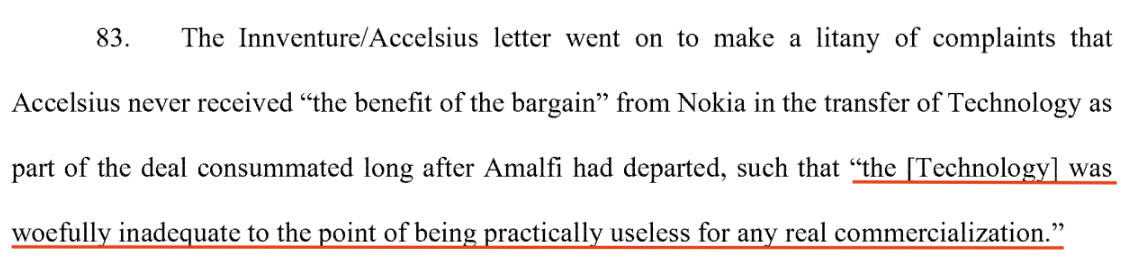

“No, we’re not sharing … we’re not sharing, no, the address, with anyone … No, I do not know that name.”

In January 2026, DarkNX added a photo to its Google web page that appears to feature the data center allegedly located at the Mississauga address. This photo, however, is a stock image with DarkNX’s logo photoshopped into the background.

Former Accelsius Employees Expressed Skepticism About The DarkNX Deal, With One Stating Clearly, “This Is Not A Real Win, I Would Not Make A Business Decision Of Investing In Accelsius Based On This Announcement”

Another Former Employee Said: “We’ve Never Heard Of This Company, They Don’t Have Customers, There’s No Data Center … So, There’s Just A lot Of Obvious Missing Pieces It Feels Like. That’s The Skepticism”

We interviewed several former Accelsius employees who expressed skepticism about the legitimacy of the DarkNX deal. For example, one former employee believed the announcement was simply a mutually beneficial market announcement, but not a real commercial win:

“I think this company DarkNX is starting to get, they want some PR, and they've gotten some great free press … I don’t see it as being credible … I just don’t, I don’t think they’re too real … I would not make a business decision based on this announcement.”

“They’re [Accelsius] chasing deals. This is not a real win. I would not make a business decision of investing in Accelsisus based upon the DarkNX announcement.”

A second former Accelsius employee also expressed skepticism about the deal:

“... where's the data center? Where are the offtakers? Where’s the customers? You know, is DarkNX going to take delivery on something if they don't have customers to consume this stuff? Those are, you know, those are the other questions, right?”

“I think, you know, we’ve never heard of the company, they don't have customers, there’s no data center. This isn’t like another known entity … So there’s just a lot of obvious, missing pieces it feels like. That’s the skepticism I think you’re maybe detecting from a lot of us.”

As we will describe in Part 4, we think the DarkNX deal mirrors Innventure’s senior leadership playbook perfectly: assure investors that massive commercial deals are just around the corner, only to have them amount to nothing in the end.

Innventure Claims That DarkNX Is “Funded,” Implying That It Has Access To Billions In Funding Needed To Complete The 300MW Data Center Campus, But DarkNX Shows Zero Signs Of Having Access To Institutional Funding

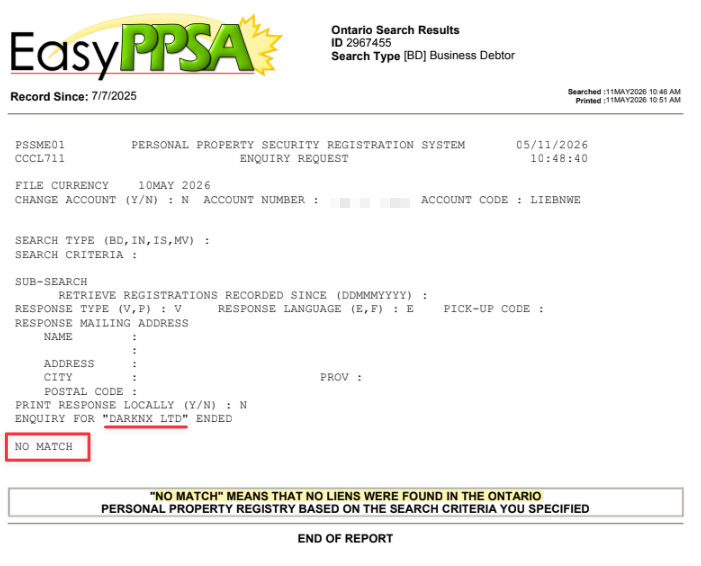

DarkNX Has No Outside Board Members, Has Not Announced Any Funding, And Canadian Lien Records Do Not Reveal Any Secured Interests On Its Assets

During Innventure’s Q4 earnings call, management assured shareholders that DarkNX has the funding to support the claimed 300MW AI Data Center campus, which in DarkNX’s own estimation would require at least $3 billion.[1]

“All I can tell you is they are funded and they represented to me directly that they're funded … I don’t know the source though, to tell you the truth.” - Roland Austrup, Chief Growth Officer, Innventure

DarkNX has not announced the closure of a financing round.

Normally, investors in new companies such as DarkNX would demand a seat on the board to oversee their investment. One would expect that a company that is “funded” to embark on a $3 billion project would have raised substantial capital from investors and would have opened its board for them or at least have characterized the source of funding.

This is not the case for DarkNX. As of April 28, 2026, the company’s founder Akif (Isaac) Islam is its only director, according to Ontario corporate records.

We also looked for indications of debt funding by searching Canadian records for registered liens against DarkNX’s assets. We found none.

Contrary to Innventure management's claims, we do not believe that DarkNX has adequate funding – or any meaningful funding at all – to undertake a $3 billion project and, in turn, meet its obligations to Accelsius.

Part 2: Innventure’s Executives Have A Long History Of Using Aggressive Projections To Lure Investors Into The Accelsius Investment Story

While we see DarkNX as the most recent and most egregious example of Innventure attempting to lure in investors to yet another “cutting-edge” technology investment, this pattern appears to extend as far back as 2021, even before the underlying IP was licensed from Nokia. Further, it appears to have continued even after the DarkNX deal announcement.

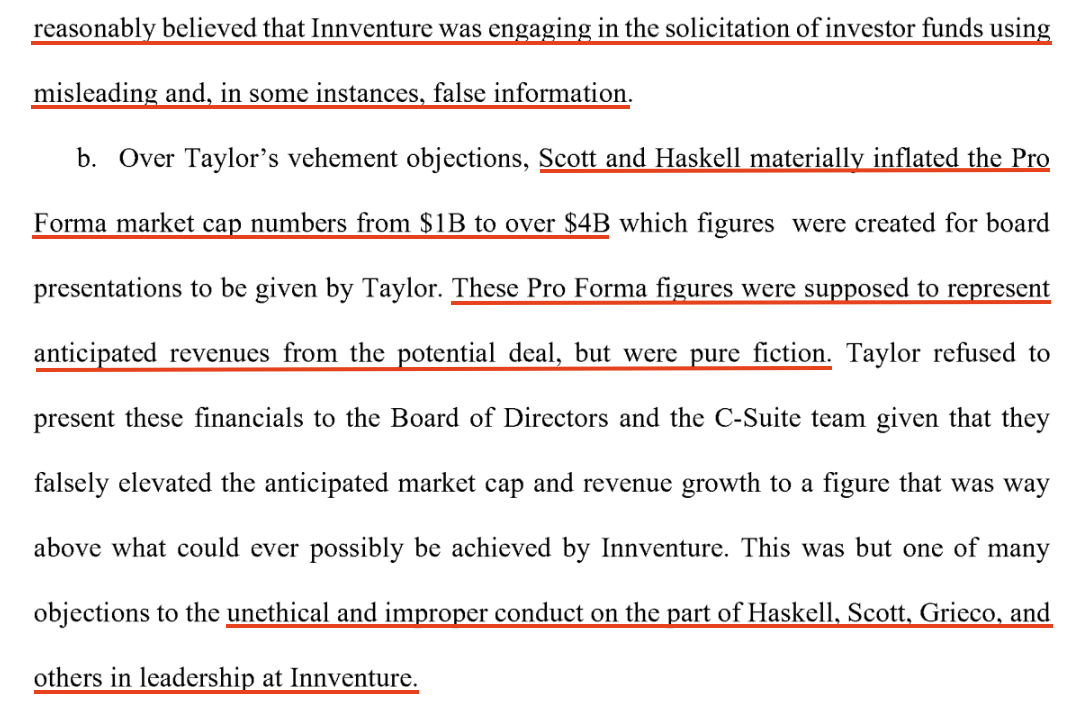

Former Innventure Executive Teresa Taylor Claimed That Executives Bill Haskell And John Scott Were Soliciting Investment For Accelsius Based On “False Information” And Revenue Projections That Were “Pure Fiction” As Far Back As 2021

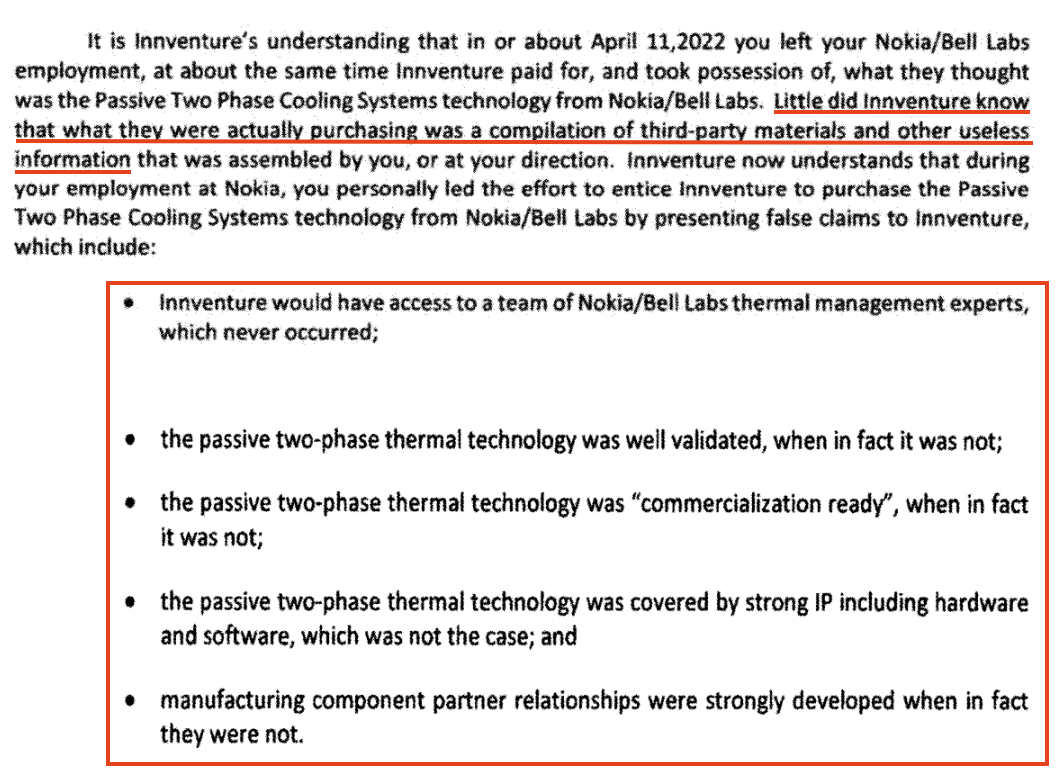

After Taylor’s Resignation, Innventure Allegedly Told Her That The Technology From Nokia Was “Useless,” Not Ready For Commercialization, Not Covered By Strong IP, And That “Any Engineer Could Replicate The Technology”

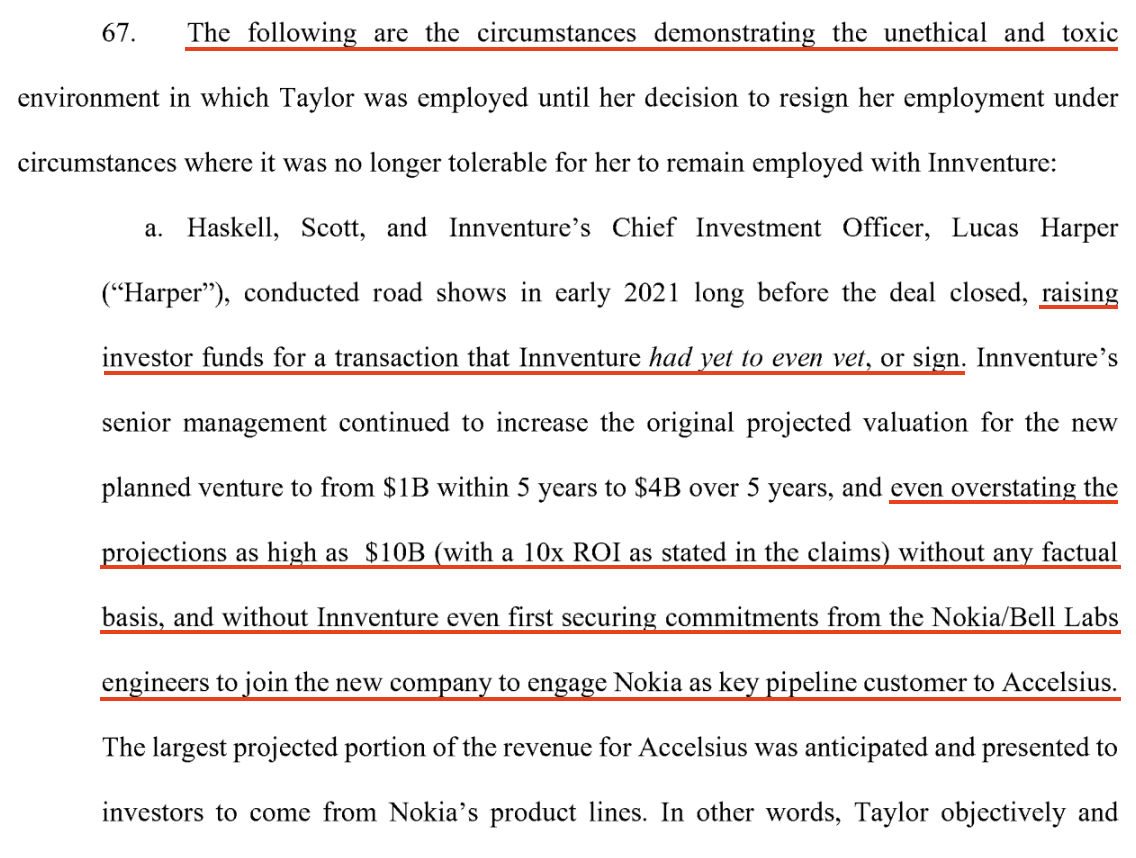

According to court filings from 2024, a former Innventure executive named Teresa Taylor resigned over what she described as an “unethical” environment where Bill Haskell and John Scott were allegedly soliciting investor funds using “misleading and, in some instances, false information.” [Pgs. 35-36]

Taylor’s claims directly relate to the original Nokia deal that underpinned the formation of Accelsius.

According to a court filing from the former executive, Haskell and Scott attempted to solicit investors for Accelsius in 2021 before the Nokia licensing deal even closed. They allegedly did so based on projections that were “pure fiction,” as well as the assumption that Nokia’s engineering team would join Accelsius and that Nokia itself would become an anchor customer. [Pgs. 35-36]

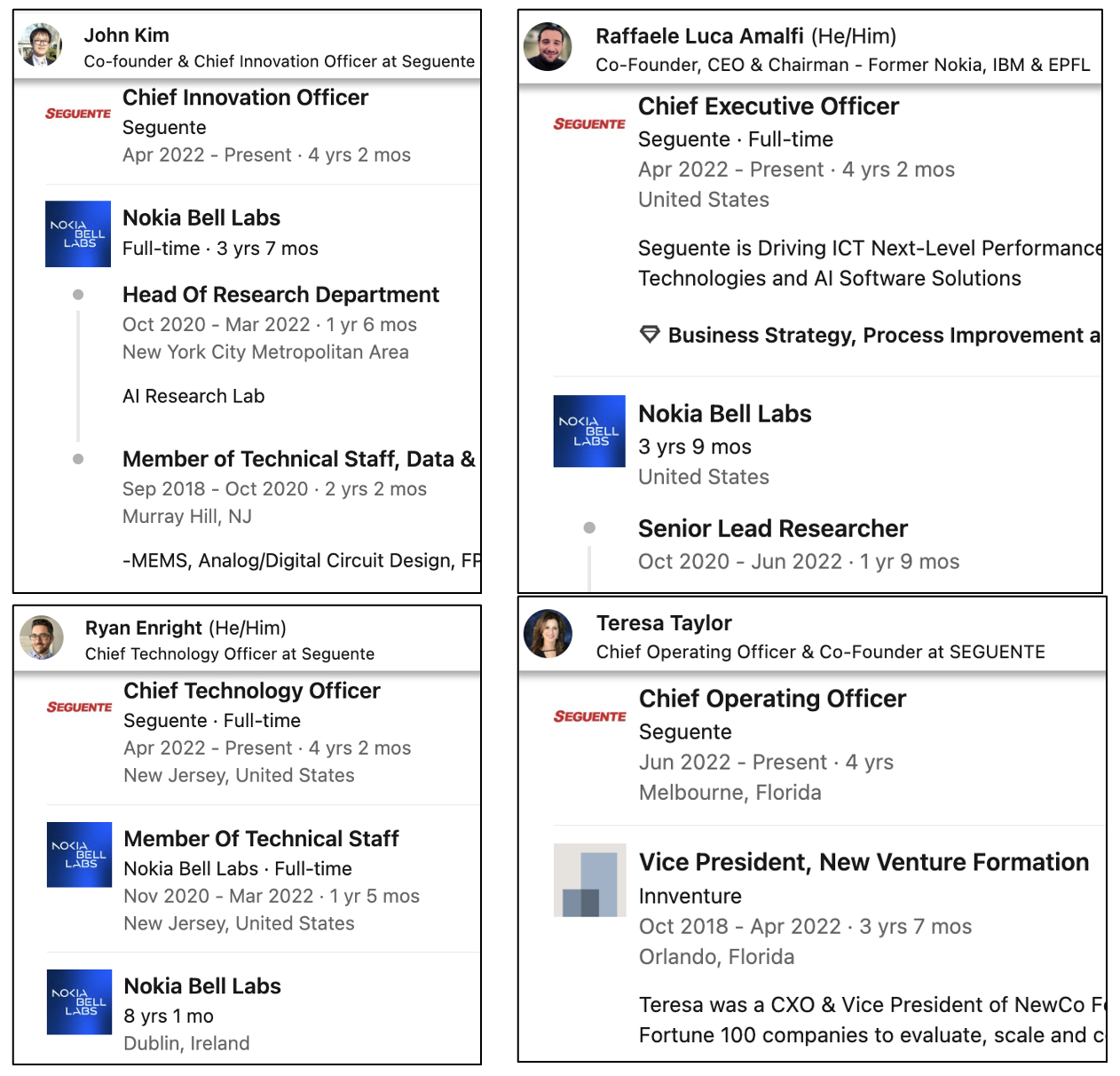

As far as we can tell, Nokia never became a customer of Accelsius. Further, much of its engineering team appears to have migrated to an entirely different liquid cooling startup called Seguente, along with former Innventure executive Teresa Taylor. Seguente appears to have a similar offering to Accelsius.

After these individuals migrated from Nokia Bell Labs to Seguente, Innventure wrote a letter to one of them expressing frustration that the technology it had acquired from Nokia was “useless,” according to the Teresa Taylor lawsuit.

According to the Taylor litigation, Innventure claimed it never received the “benefit of the bargain” with Nokia.

Overall, it seems that even before acquiring technology it would later describe as “useless” and not ready for commercialization, Innventure’s executives were putting aggressive projections in front of potential investors in an attempt to raise money, per the allegations.

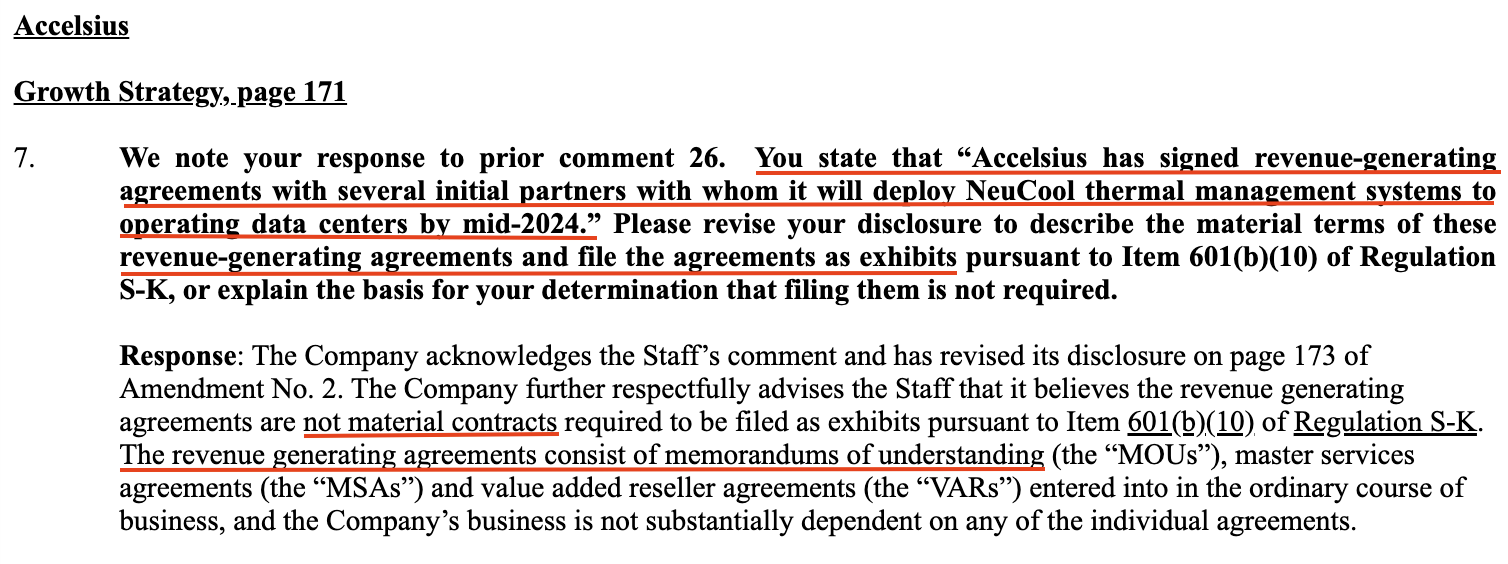

More Recently, Innventure’s Management Has Continued To Promote Accelsius’s Near Term Commercial Prospects To Shareholders, Claiming In Its Early 2024 SPAC Registration Statement That It Had Signed Several “Revenue-Generating” Agreements To Deploy To “Operating Data Centers” By Mid-2024

When The SEC Asked Innventure To Disclose The Terms Of These Agreements And File Them As Exhibits, Innventure Admitted They Were “Not Material Contracts” And That Some Of Them Were Simply MOUs

Innventure’s SPAC deal reveals other red flags related to aggressive revenue projections.

In early 2024, Innventure was preparing for its SPAC deal and filed a registration statement with the SEC stating that Accelsius had signed “revenue-generating agreements” with “several initial partners” to deploy its products in “operating data centers” by mid-2024. [Pg. 171]

14 days later, the SEC sent a letter to Innventure asking it to clarify the terms of these “revenue-generating” agreements and file them as exhibits. In response, Innventure admitted that these agreements were not material contracts, and that some were simply Memorandums of Understanding (“MOUs”).

Later That Year, Innventure’s Auditor BDO Flagged A Material Weakness In Financial Controls Related To “Forecasts Prepared For Accelsius”

Innventure Later Dismissed BDO In Favor Of An Auditor That Is Infamous For “Widespread Quality Control” Failures In SPAC Audits

In Innventure’s 2024 annual report, published in April 2025, the company’s auditor BDO highlighted five material weaknesses in the company’s financial reporting. One area of concern was that “the forecast prepared for Accelsius was not effective” — an oddly specific and uncommon call-out from an auditor, in our experience.

4 months later, Innventure dismissed BDO in favor of WithumSmith+Brown PC.

Withum is infamous for auditing a high volume of SPAC blowups and was fined by the PCAOB for “widespread quality control failures in SPAC audits” in 2024, according to Reuters.

Over The Last Year, Innventure’s Management Has Continued To Tout The Imminent Arrival Of Large-Scale Commercial Deals, Claiming Multiple 8-Figure And Even 9-Figure “Real Production Orders,” But We Do Not Believe These Orders Exist

Former Accelsius Employee: “If There’s Something That’s Materialized Like That, That Is Big News … I’m Not Aware Of Anything Like That”

In November 2025, CEO Bill Haskell claimed that Accelsius had more than $750 million in “production opportunities for 2026” in its pipeline, which he described as a “shift from proof of concept to large-scale deployments.”

Seemingly confirming the arrival of these deals, Haskell stated in March 2026 that Accelsius now has multiple 8-figure “real commercial production orders” and has even closed 9-figure deals:

“If we were sitting here a year ago, you know, our average proposal outstanding was probably worth a couple of hundred thousand dollars and now we're, not virtually, not everyone, but most of the purchase orders are either 7 or 8, or even 9 figures, in terms of scale. I would say most are probably in the 8-figure range. So that just shows you a significant transition from evaluation units to real commercial production orders.”

We do not believe orders of this scale exist. We interviewed former Accelsius employees who told us they were unaware of any commercial deals outside of DarkNX – which they expressed substantial skepticism about, as detailed above.

For example, we asked one former employee about Haskell’s claims of multiple 8-figure and 9-figure orders, and they told us that they were “not aware of anything like that” and that they did not think Accelsius was “anywhere near mass production conversations.”

“I don't think they’re anywhere near mass production conversations.”

“If there's something that’s materialized like that, that is big news. I don’t hear it coming from Accelsius, obviously. I don’t know. That’s really bullish. And I have no way of validating that.”

The former employee explained that Accelsius and Innventure are “press release happy” and would surely mention new customers if they existed, and that the company has primarily engaged in proof-of-concepts so far:

“They’re very press release happy, and if they had more referenceable customers, they would be very loud about it… that’s what I think would keep their executives up at night, is their scoreboard. So, yeah, that’s my biggest concern too … they were expecting to see more adoption in ‘26 than they have…”

“We were in POCs [Proof-of-Concepts] primarily, of which, you know, Accelsius was able to create a handful here a month or whatever. It’s not a lot. Nowhere near what you, you know, if you had a 5MW data center, they would have to do a third-party contract name manufacturers fulfill those orders … They haven’t walked on that planet yet.”

During the Q1 earnings call on May 14, Innventure announced zero new deals for Accelsius and instead reiterated the claimed “$50 million in bookings” from its previous earnings call, which we believe is largely tied to what we see as a sham deal with DarkNX.[1]

In Innventure’s Q4 2025 earnings call, an analyst asked if DarkNX made up a “significant chunk” of the company’s claimed $50 million bookings. Haskell had the following reply: “So it's fairly chunky right now. But I think what you'll see going forward is we'll have a larger framework of customers.” ↩︎

Part 3: The Mechanics Of The Insider Enrichment Scheme And Accelerating Dilution

Activist investors have criticized the excessive overhead spending at Innventure while calling for fiscal discipline and the prioritization of Accelsius over Innventure’s other operating companies.

While these activists are, in our view, right to criticize management, we think they are vastly underestimating the level of risk associated with this management team.

Despite Generating Only $3.2 Million In Revenue And Reporting $371 Million In Losses During 2024 And 2025, Bill Haskell, Mike Otworth, And John Scott Have Paid Themselves Nearly $31.6 Million In Total Compensation During The Same Period

Since Becoming A Public Company Shareholders Have Been Diluted By 41% And Face An Additional ~24% Dilution Overhang From ~18 Million Outstanding Warrants And An Equity Standby Agreement With Yorkville Advisors

Despite generating only $3.2 million in revenue in 2024 and 2025 combined and racking up combined losses of $371 million, we believe Innventure’s management has pursued deliberate and egregious self-enrichment at the expense of its shareholders.[1]

Innventure’s annual report shows the pre-SPAC revenue for Inventure LLC (“Predecessor”) and then post-SPAC transaction for Inventure Inc (“Successor”). ↩︎

Between 2024 and 2025, key management personnel, CEO Haskell, Chairman Otworth and CSO Scott, collectively took home $31.6 million in total compensation consisting of salary, bonuses, stock, and option awards.

(Source: Proxy Statements, 8-K | 1, 2, 3)

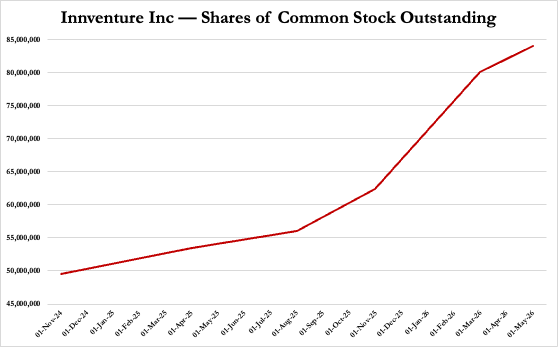

Since November 2024 to May 2026, Innventure share count has ballooned from approximately ~49.5 million to ~84 million, diluting shareholders by 41% in just ~18 months.

Looking forward, Innventure has ~18.3 million warrants outstanding as well as a Standby Equity Purchase Agreement (“SEPA”) that creates a potential additional dilution overhang of ~24%.[1]

Based on 18.3 million warrants outstanding, $55 million remaining on the SEPA, that at current market price of 6.41 could result in the issuance of ~8.5 million shares. Calculation assumes 84 million shares outstanding. ↩︎

Two Activist Investors Have Publicly Criticized Excessive Management Compensation, Overhead Spending, And Shareholder Dilution

In February 2026, two activist investors publicly criticized Innventure’s “extravagant” overhead spending and shareholder dilution, “continued governance failure,” and what one described as an “untenable” financial trajectory:

“We believe management’s active – if unintentional – value destruction is rooted in structural failures in corporate governance and strategy.” [Commonwealth Asset Investors]

“We supported this Company patiently, and privately. That patience has run out. Not because we have lost faith in what this Company could be, but because we have watched the Board fail — repeatedly, and without apparent consequence — to hold itself to the very standard it demands of every company it builds.” [Ascent Capital Partners]

These harsh critiques of Innventure’s management were softened by the extremely bullish sentiment about Accelsius, which both activists saw as the primary driver of value for shareholders.

Further, one activist wrote a follow-up letter on May 4 stating that its communications with Innventure “produced results” and that management was “engaged seriously” and executing.

While we wholeheartedly disagree with the bullish sentiments around Accelsius, we also believe that investors are largely missing the bigger picture with respect to Innventure’s management. In our view, insider enrichment is not a bug at Innventure, it’s a feature of a playbook that management has been running for decades.

Last Month, Insiders Awarded Themselves Another 2,000,000 “Earnout” Shares Worth $9.2 Million, Tied To Accelsius Signing A “Binding Contract” For At Least $15 Million

We Believe This Milestone Was Triggered By The DarkNX Deal, Which, As Explained Previously, Has All The Hallmarks Of A Sham Deal

After earning a $2.5 million bonus for simply closing the SPAC deal, CEO Haskell and other insiders were also poised to gain from an additional 5 million earnout shares tied to several commercial milestones.

For example, as part of the SPAC transaction, the holders of Innventure's outstanding equity prior to the transaction had the right to receive up to 5 million shares by meeting certain milestones. One of these milestones was simply that Accelsius had “entered into binding contracts providing … in excess of $15 million in revenue.”

On April 2, 2026, Innventure’s board recognized that Accelsius had entered into such a contract and the 2 million shares, worth $9.2 million, were issued to Innventure’s pre-SPAC equity holders, of which John Scott, Michael Otworth and Bill Haskell were among the largest holders.[1]

The single largest voting unitholder of Innventure LLC was Innventure1 LLC with 5,894,438 Class A units and 342,608 Class B-1 units. As of January 2024, Michael Otworth, John Scott, Richard Brenner were members of Innventure1 LLC. James O Donally, acted as trustee of several trusts holding interests in Innventure1 LLC. Scott and Otworth, also held 171,498 and 260,787 Innventure LLC Class B-1 units and Haskell owned 430,000 Class C units. Class A, B, B-1 and C units were converted Innventure shares after the SPAC transaction. ↩︎

The only commercial deal Innventure has touted is the DarkNX transaction. We believe it is likely that this “deal” is what allowed management to trigger this milestone and access the 2 million shares.

This came after they had already awarded themselves 2 million shares in January 2025 for the formation of Refinity, which is run by Innventure’s current Chief Technology Officer, Bill Grieco, who also worked at management’s previous blow-up, PetroAlgae (see Part 4 for more details).

Insiders Are Cashing Out: As Soon As The Lock-Up Agreement Expired, And A Month Before The DarkNX Deal Was Publicly Announced, Innventure’s Largest Shareholder Began Dumping Shares And Has Now Exited At Least ~60% Of His Position

He Is Now Under The Threshold For Public Reporting

At the time of its SPAC deal, Innventure’s largest single shareholder was an entity called We-Inn LLC, which is controlled by former Walgreens CEO Greg Wasson, who began working with the Innventure team in 2017.[1]

Mr. Wasson acted as Director of Innventure from 2017 to 2020, according to his LinkedIn profile. ↩︎

Once the SPAC transaction was completed, We-Inn received 19.5% of the common stock issued as part of the transaction, representing 8.6 million shares. However, We-Inn was subject to a one-year lock-up agreement following the SPAC transaction, which ended on October 2, 2025, according to Innventure's annual report.[1]

Within days of the expiration of the lock-up agreement, as Innventure’s operating companies were supposedly on the cusp of imminent commercial success and just weeks before the DarkNX announcement, Wasson started selling Innventure’s shares, even at prices more than 50% below today’s price.

A month after Wasson’s sales began, Innventure CEO Haskell told shareholders during an earnings call about his belief that shares were “undervalued.”

Throughout last April, Wasson sold another 1.8 million shares, taking his ownership below 5%— the reporting threshold for filing beneficial owner reports, known as Schedules 13D, which We-Inn had been filing since October 2024. This will allow Wasson to potentially exit his entire position without further public scrutiny.

We find it concerning that the majority stockholder of 8 years would run to exit most of his position just as the company is supposedly on the cusp of hockey-stick revenue growth.

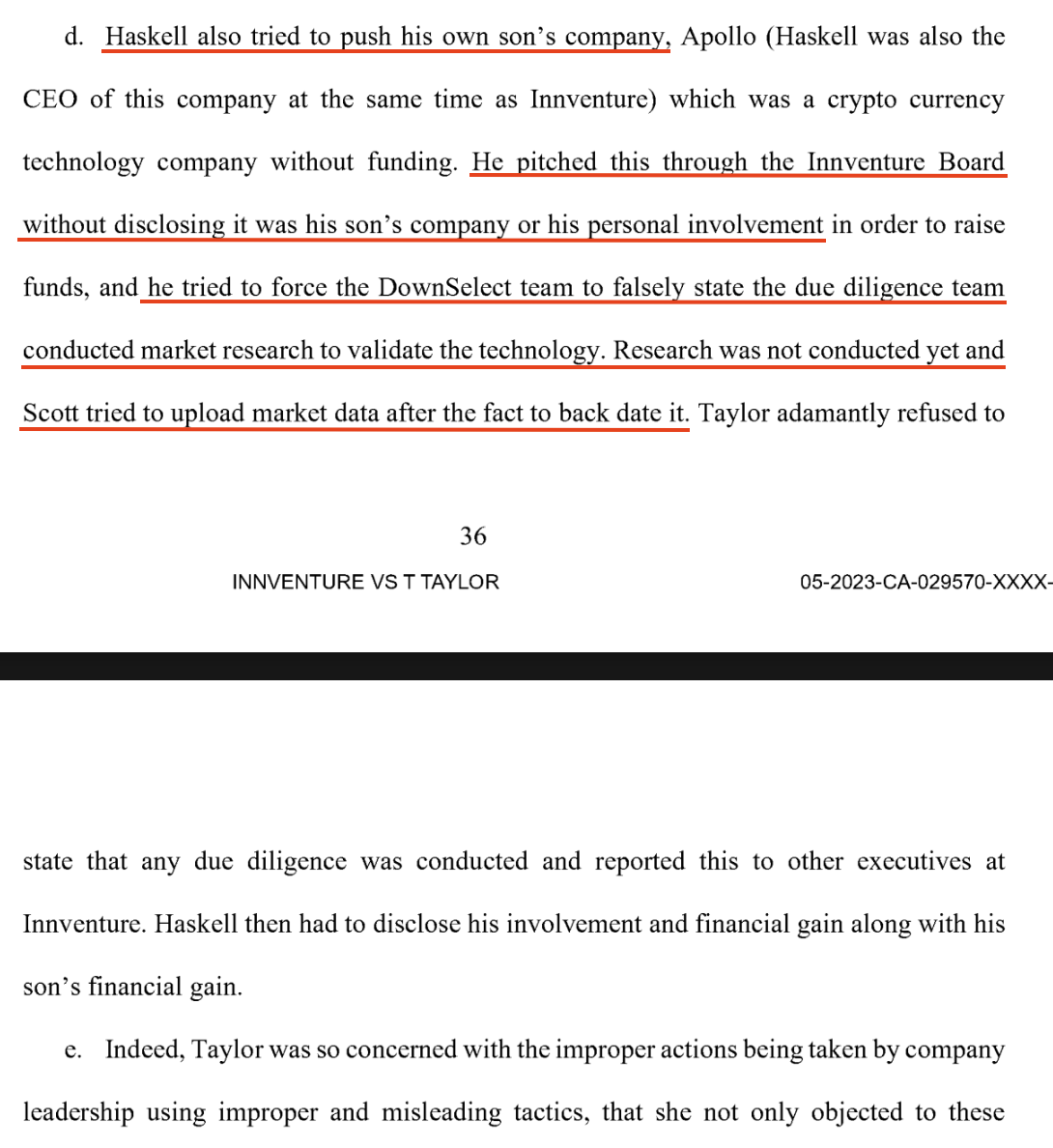

Governance Red Flag: In 2020, CEO Haskell Allegedly Attempted To Raise Funds From Innventure For His Son’s Fraudulent Crypto Trading Company, According To A Former Innventure Executive And A Third-Party Investor Who Claims To Have Been Defrauded By The Haskells

As a final example of the caliber and motivations of Innventure’s management team, Haskell allegedly attempted to foist his son’s non-existent cryptocurrency company onto Innventure shareholders in 2022, per lawsuits from a former Innventure executive and a third-party investor who claim to have been defrauded by the Haskell family.

According to former Innventure executive Teresa Taylor, Haskell did not disclose it was his son’s company or that he had a personal involvement in the business when he pitched it to the Innventure board and tried to pressure Innventure employees to say that the technology was validated.[1]

The alleged technology was associated with Apollo Blockchain Solutions LLC. (Pg. 4) Apollo was co-founded by Lew Smyrinios, who moonlighted as a Startup and Commissioning Manager of PureCycle, according to his LinkedIn profile. See Part 4 for further reference on PureCycle. ↩︎

Another lawsuit against the Haskells from a third-party investor corroborates Taylor’s claims.

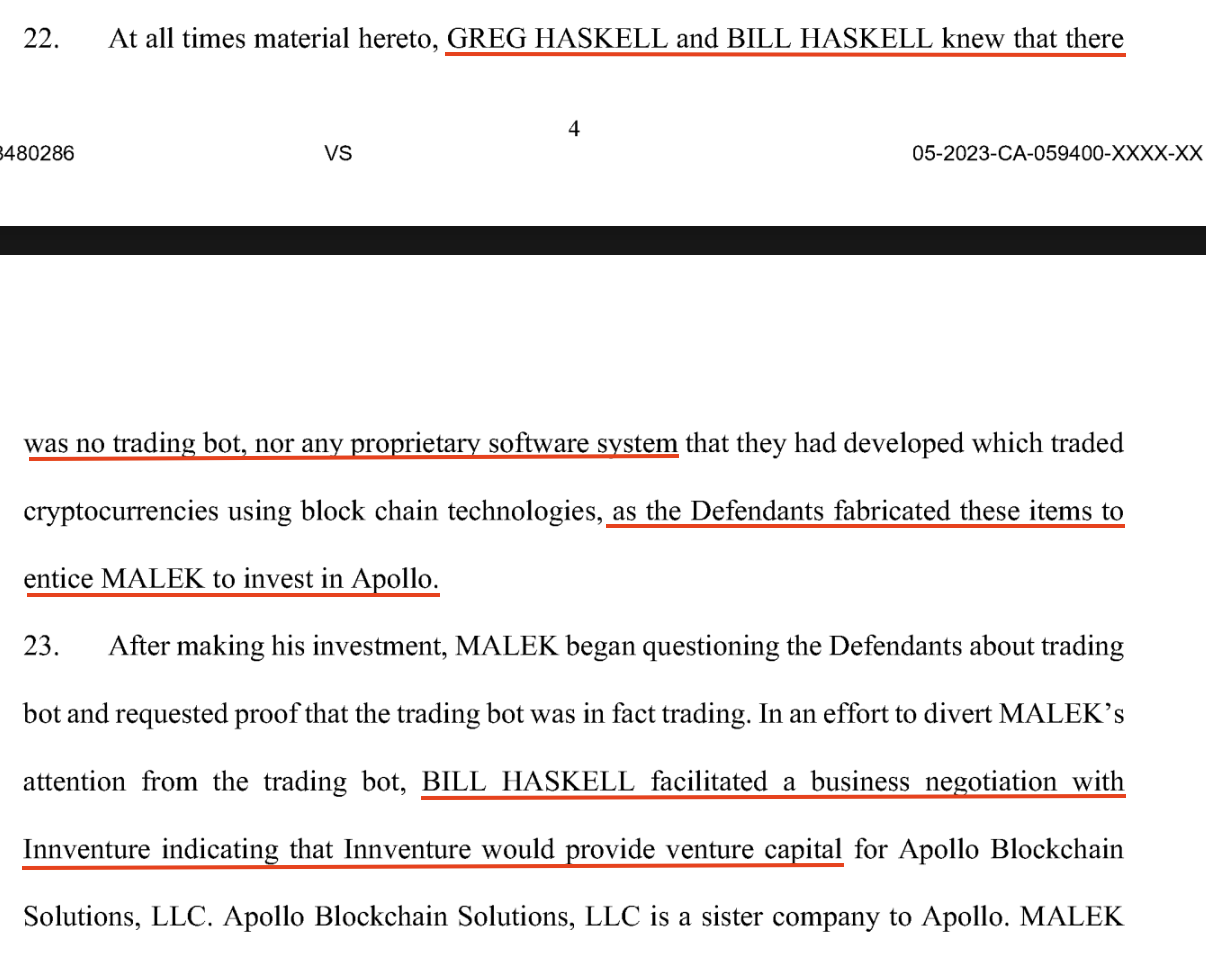

In December 2023, an investor filed a lawsuit against Haskell for fraud after investing $100,000 in a purported “developed technology to trade cryptocurrencies using blockchain technologies,” according to a complaint filed by the investor. [Pg. 2]

While Haskell’s son claimed his “trading bot” generated a 230% return in less than a year, the investor claimed that the bot did not exist, stating that the Haskell's “fabricated these items to entice” him to invest in the company. [Pgs. 2, 4-5]

According to the investor, Haskell attempted to “divert” his attention from the alleged “trading bot,” by facilitating meetings and claiming that Innventure would provide the venture capital for the business.[1]

The legal case against Haskell and his son was resolved outside court, according to a notice of dismissal filed in January 2024. ↩︎

Part 4: Innventure’s Management Team Has Been Running Failed Technology Companies For 30+ Years

None Of What Is Happening At Innventure Should Surprise Investors Since Innventure’s Executives Have Launched Numerous Technology Companies, Many Of Which Touted Groundbreaking Tech, Blue-Chip Partnerships, And The Imminent Arrival Of Hockey-Stick Revenue Growth

Virtually All Of These Companies Failed Spectacularly, Resulting In Numerous Bankruptcies, Delistings, And Blow-Ups That Wiped Out Shareholders

As mentioned, John Scott, Bill Haskell, and Mike Otworth ran two other technology incubators, XL Vision and XL Techgroup, which were predecessors to Innventure.

For readers who are unfamiliar with the history of these businesses, we strongly recommend reading the 2021 Hindenburg Research report which details how, out of 6 companies associated with XL Vision and XL TechGroup, “2 went bankrupt, 3 were delisted and 1 was acquired following a ~95% decline” while “$760 million in public shareholder capital was incinerated.”

Scott, Haskell, and Otworth’s playbook seems to revolve around promoting the involvement of blue-chip partners, breakthrough technologies sourced from “multinationals,” and the imminent arrival of hockey-stick revenue growth.

As one example, Innventure’s predecessor XL TechGroup incubated a company called TyraTech in 2004, which was focused on human-safe insecticides. A year later, John Scott claimed it was in “final negotiations” for “large-scale commercial deals.” TyraTech IPO’d in 2007 and announced “partnerships” with blue-chip companies like Kraft Foods.

Three years after the IPO, the company reported just $2 million in revenue and had accumulated losses of $69 million. Its share price had plummeted by 95%. It was later acquired at a 99% discount from its IPO price.[1]

The IPO price reported by Reuters was 505 pence. TyraTech was acquired for 3.15 pence per share. ↩︎

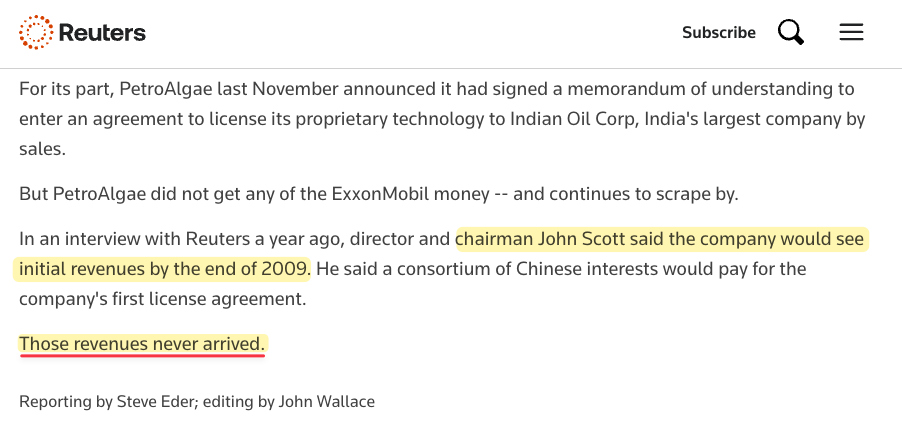

In another example, Innventure co-founder and CSO John Scott founded PetroAlgae and took it public through a reverse-merger in 2008, with Innventure’s current CEO Haskell serving as the Executive VP.[1]

PetroAlgae claimed to make fuel from “proprietary algae strains” and touted major deals to license its tech to major corporations like Indian Oil.

After PetroAlgae announced a royalty-bearing licensing deal of its technology to “construct and operate ten facilities” in China, John Scott said that revenues would flow by the end of 2009, but that revenue never arrived, according to Reuters.

As of 2011, PetroAlgae had generated zero revenue, per its financial statements. It was delisted from the OTC Bulletin Board that year.

These are just two examples of multiple companies that were heavily promoted by Innventure senior leadership – but we were unable to identify a single one that was commercially successful.

After The Collapse Of XL Vision, XL TechGroup, And Numerous Portfolio Companies, John Scott And Mike Otworth Founded Innventure, Along With Its First Portfolio Company PureCycle Technologies

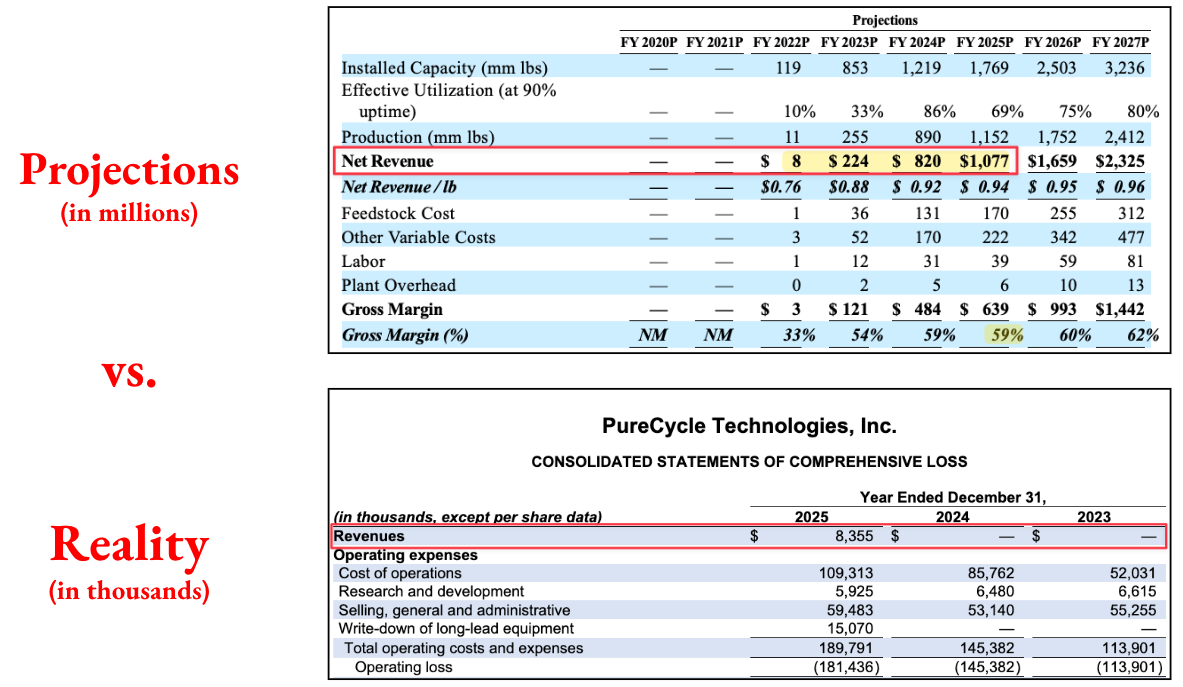

Despite Having Zero Revenue, PureCycle Went Public Through A 2021 SPAC Deal Based On Supposedly Revolutionary Recycling Tech, Massive Offtake Deals With Blue-Chip Partners, And Projections Of 7 Mega Factories And A Billion Dollars In Revenue By 2025

Reality Check: PureCycle Has Achieved Less Than 1% Of Its Projected Revenue At Deeply Negative Margins While Racking Up An Accumulated Deficit Of ~$850 Million Getting 1 Factory To ~⅓ Of Nameplate Capacity

3 years after the John Scott left PetroAlgae he partnered with Mike Otworth and founded Innventure based on the same strategy that led to the collapse of XL Vision, XL Techgroup, and their numerous portfolio companies.

Innventure's first portfolio company, Purecycle Technologies, was incorporated in 2015 to commercialize recycling technology IP licensed from Procter & Gamble.

Armed with zero revenues and a supposedly revolutionary process to recycle polypropylene, PureCycle merged with a SPAC during the SPAC craze of 2021. The company had a grandiose plan to build 7 factories and scale into one of the largest plastic recyclers globally. [Pg. 27]

Like previous blowups, Purecycle claimed “blue chip” partnerships and offtake deals with the likes of Procter & Gamble, Total Energy, and L’Oreal. PureCycle management claimed that they would generate over a billion dollars in 2025 revenue at software-like margins, according to its SEC filings.

Fast forward to 2026, and rather than the 7 operational factories outlined in its SPAC deck, it has commenced production at a single plant, which is currently operating at less than 1/3 of its nameplate capacity.

More concerning, since 2021, the company has generated less than 0.5% of its projected revenue for 2022 to 2025. Due to its sustained losses, the company has an accumulated deficit of $849 million.[1]

PureCycle shares have declined by more than 60% after reaching an all-time high in its first few days of trading on Nasdaq. Since then, investors have been aggressively diluted with the company increasing its share count by 54%.[1]

PureCycle had 117,349,281 common shares outstanding as of Q1 2021, which grew by 54% to 180,863,550 shares by May 2026. ↩︎

Despite PureCycle’s unequivocal failure to meet any of its stated goals, Innventure does victory laps around PureCycle by claiming its shareholders received $460 million in PureCycle’s shares.

Conclusion

Like past blowups, Accelsius claims to be a front-runner in an in-vogue investing space. Yet, despite unprecedented demand, it has failed to announce a single commercial-scale deal aside from DarkNX, which we see as obviously fake.

We see Innventure as the latest iteration of a decades-long grift that has successfully used the brand equity of large corporations like Nokia and P&G, assurances of imminent commercial success, and the allure of supposedly “groundbreaking” technologies to seduce unsuspecting investors. In reality, virtually all of these companies have failed spectacularly.

This playbook has generated hundreds of millions for Innventure’s insiders, while investors have lost what we estimate to be billions of dollars over the years.

We think Innventure will be yet another abject failure with shareholders left holding the bag.

Disclosure: We Are Short Shares of Innventure Inc (NASDAQ: INV)

Legal Disclaimer

Use of Morpheus Research LLC’s (“Morpheus Research”) research is at your own risk. In no event should Morpheus Research or any affiliated party be liable for any direct or indirect trading losses caused by any information in this report. You further agree to do your own research and due diligence, consult your own financial, legal, and tax advisors before making any investment decision with respect to transacting in any securities covered herein. You should assume that as of the publication date of any short-biased report or letter, Morpheus Research (possibly along with or through our members, partners, affiliates, employees, and/or consultants) may have a position in the stock, bonds, derivatives, or securities covered herein and, therefore, stands to realize significant gains if the price of the securities move. Following publication of any report or letter, Morpheus Research intends to continue transacting in the securities covered therein and may be long, short, or neutral at any time thereafter regardless of Morpheus Research’s initial position or views. Morpheus Research’s investments are subject to its risk management guidance, which may result in the de-risking of some or all its positions at any time following publication of any report or letter depending on security-specific, market or other relevant conditions. This is neither an offer to sell or a solicitation of an offer to buy any security, nor shall any security be offered or sold to any person, in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction. Morpheus Research is neither registered as an investment advisor in the United States, nor does it have similar registration in any other jurisdiction. To the best of Morpheus Research’s ability and belief, all information contained herein is accurate and reliable and has been obtained from public sources believed to be accurate and reliable, and who are not insiders or connected persons of the stock covered herein or who may otherwise owe any fiduciary duty or duty of confidentiality to the issuer. Conclusions expressed herein are based upon the information disclosed herein and represent the opinion of Morpheus Research. Such information is presented “as is,” without warranty of any kind – whether express or implied. This report was prepared independently, without coordination with any third party. Morpheus Research makes no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results to be obtained from its use. All expressions of opinion are subject to change without notice, and Morpheus Research does not undertake to update or supplement this report or any of the information contained herein.