Velo3D: How A Physical Therapist With A Bogus Resume Parlayed A Failed SPAC And A Sham Relationship With SpaceX Into A $390 Million Dollar Fortune

Summary

- Velo3D (NASDAQ: VELO) (“Velo”) is a California-based additive manufacturing company that went public during the 2021 SPAC boom with backing from tennis superstar Serena Williams and SpaceX. SpaceX also served as the anchor customer for Velo’s Sapphire brand of 3D printers. Velo severely missed its SPAC projections and generated consistent losses. By summer 2024, the company was delisted from NYSE and was on the brink of bankruptcy.

- In December 2024, little-known Indiana businessman, Dr. Arun Jeldi (“Jeldi”), became CEO of Velo after restructuring Velo’s debt and obtaining control of 95% of its equity. Jeldi claims to be a successful doctor-turned-entrepreneur who bootstrapped a $50 million healthcare company and four other “multi-million dollar” manufacturing companies that he runs alongside Velo.

- Under Jeldi’s leadership, Velo’s market capitalization has soared to $537 million based on a renewed focus on aerospace and defense, a supposedly strong relationship with SpaceX, and the launch of its Rapid Production Solutions (“RPS”) division which will purportedly capture higher-margin, recurring revenue from selling 3D printed parts.

- Our investigation, involving 16 interviews with industry experts, former Velo3D employees and customers, reveals that Velo’s turnaround is an illusion fueled by a litany of overhyped deals, the aggressive promotion of a SpaceX relationship that largely ended years ago, and the dressing up of Velo’s unreliable technology as market leading. At the top of all this is a “fake it till you make it” CEO who appears to have cooked up virtually every aspect of his past.

- The financial media has portrayed Velo as a “proxy trade” for SpaceX exposure, and CEO Jeldi has leaned into this narrative, claiming in December 2025 that SpaceX is increasing its fleet of 3D printers and acquiring parts through Velo’s RPS division. Former employees and Velo’s own disclosures indicate that SpaceX has not purchased a printer since 2022 and that the relationship is virtually non-existent today.

- An IP license agreement signed in 2024 allows SpaceX to manufacture its own printers in-house, according to multiple people familiar with the deal. A former senior leader from Velo told us: “I think that any revenue related to SpaceX has pretty much ceased to exist since 2024.”

- One former Velo employee told us: “SpaceX has the option now to just build their own machines with the same technology.” Another former Velo employee told us: “I would be pretty skeptical of [SpaceX] buying more printers from Velo, and the reason I say that is, in October of 2024, we licensed them all of our IP. 100% of it … I’d be very surprised if they ever bought another Velo system.”

- SpaceX appears to have found an alternative to Velo, according to a former Velo employee who told us: “The reality of that is that Velo is no longer in business with SpaceX … There has been minimal effort on both sides trying to continue that relationship. And the reason for that is that, number one, SpaceX have found an alternative.”

- In addition to SpaceX, Velo’s rally has been driven by a new focus on defense, space, and government customers for both its printer and RPS businesses. We believe, however, that this pipeline is stuffed with highly speculative deals that are unlikely to result in significant revenue, while some “prime” defense customers appear to have ended their relationship with Velo.

- Deal #1: In April 2025, Velo announced a $15 million RPS deal with Momentus, a company whose stock price has fallen over 97% since its 2021 SPAC deal, and whose management has issued a going concern warning. Almost a year after the deal was announced, Velo has booked zero revenue from the deal, according to its financial statements. A former Velo employee described the deal as a “distraction” and “an effort to create a press release for us, quite frankly.”

- Deal #2: In December 2025, Velo announced a $32.6 million deal with the Department of War (“DoW”), which the sell-side characterized as a “significant opportunity” and “evidence” of Velo’s penetration into the defense sector. As of this writing, however, the DoW has funded just ~9% of this program, which is scheduled to end in 3 months, per a government contracting database. In March, a Velo competitor called Nikon SLM won a new 12-month contract under the same program.

- Deal #3: In March 2026, Velo announced a $9.8 million contract with the Defense Logistics Agency. CEO Jeldi characterized the deal as “strategically important” and claimed it positioned Velo at the “forefront” of additive manufacturing for the military. In reality, the $9.8 million is a total amount for which 24 successful bidders including Velo must further compete. The contract comes with no guaranteed revenue, and to date, zero dollars have been allocated to Velo under the program, according to a government contracting database.

- CEO Jeldi has cited Velo’s relationship with Lockheed Martin as evidence of Velo’s footprint in defense. But two former Velo employees told us Lockheed “decided to not use our product” and that there was “such a high level of dissatisfaction from the Lockheed guys that they were just like, screw it.” Lockheed recently published a write-up on its additive manufacturing strategy and named four 3D printing partners – but Velo was not on the list. We believe this relationship is very likely completely dead.

- CEO Jeldi has claimed that Velo’s technology is virtually unmatched and that only Velo can deliver what space and defense companies want. Not only is this claim obviously false, but it appears that Velo is being aggressively outcompeted by firms such as Nikon SLM and EOS, which are viewed as “industry favorites,” per our interviews with a multitude of industry experts, including former Velo employees.

- For example, one former Velo employee described the company’s printer as a “science experiment” and told us that “the reliability of these machines is very, very questionable comparing to EOS or SLM.” Another former Velo employee also told us that “reliability is inherently kind of low” and explained that many Velo customers were only getting 20% utilization out of their printers, while uptime for EOS printers is “pretty reliably up in the 70s.”

- We interviewed an additive manufacturing expert who spent over a decade studying 3D printers on behalf of a prime defense contractor. They told us Velo’s printer “tends to break down a lot” and that its “uptime is notably a problem.” A former Velo employee corroborated this, saying the market is “worried” about investing in a Velo printer because of all the “reliability issues they’ve heard in the field.”

- Former Velo employees also cast doubts about the company’ pivot to a rapid printing solution operation, citing a lack of a competitive edge, reliability issues, and a lack of automation. One told us: “I still have strong reservations around … is that a business model that, at the end of the day, can really be profitable and how successful will it be … I question, long-term, the economics of that business in general, right?”

- Another former Velo employee told us: “My conclusion is that with the current technology that Velo has, they are not ready to do that [bring production in-house]. They will be losing money.” The former employee explained that Velo’s machines require “an army of people to operate” and that “there’s virtually minimal automation.”

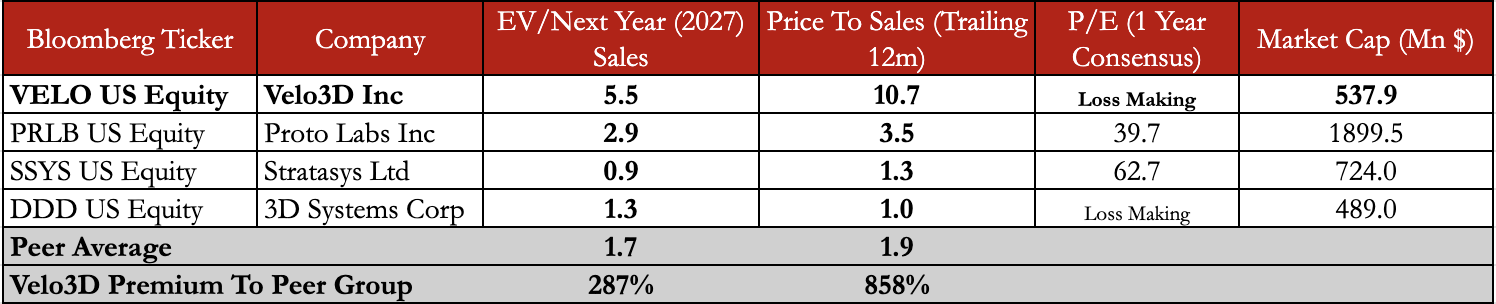

- Even ignoring our report, Velo3D has fundamental downside risk due to a nosebleed valuation of 10.7x price-to-sales, a premium of 858% to its peer average. Velo trades at this industry-leading premium despite the fact that revenue has been virtually flat over the last 6 quarters while the business has continued to generate consistent losses.

- Other red flags include: 1) high executive turnover (CTO, CFO, COO, & VP of Technology departed since Jeldi took control), 2) seven unremediated material weaknesses in accounting controls, and 3) rapid shareholder dilution driven by a 129% increase in the Velo share count under Jeldi’s leadership.

- Investors should also be concerned that Velo CEO Jeldi’s bio contains egregious exaggerations, outright fabrications, and omits a history of bad business deals and litigation. For example, despite calling himself a “doctor” who “practiced medicine,” his highest degree of education is a bachelor's in physical therapy. His “multi-million dollar” businesses appear to be shell companies with little to no discernible operations, and most are affiliated with the same vacant address where the landlord sued Jeldi for failing to make rent payments.

- CEO Jeldi appears to have gotten his start in manufacturing by working with his brother Bala Jeldi, who faced numerous civil and criminal cases in India and allegedly tried to flee the country after defrauding investors, per police reports. A former associate of Bala’s told us he “essentially defrauded investors,” causing them to “come after him.” Bala Jeldi’s Indian company bears a striking branding resemblance to Arun Jeldi’s magnesium venture in the U.S., which has no discernible operations but which has faced a litany of lawsuits from creditors.

- CEO Jeldi, a former physical therapist, has already effectively cashed out a substantial sum by pledging 3 million shares, worth ~$54 million, for a private loan, per Velo’s April proxy statement. We believe this could expose shareholders to downside pressure due to potential margin calls if Velo’s share price declines.

Initial Disclosure: After extensive research, we believe the evidence justifies a short position in shares of Velo3D, Inc. (NASDAQ: VELO). Morpheus Research holds short positions in VELO. This report represents our opinion, and we encourage all readers to do their own due diligence. Please see our full disclaimer at the bottom of the report.

Background: A Flailing 3D Printing SPAC Rallying On SpaceX Hype And A Defense Themed Turnaround

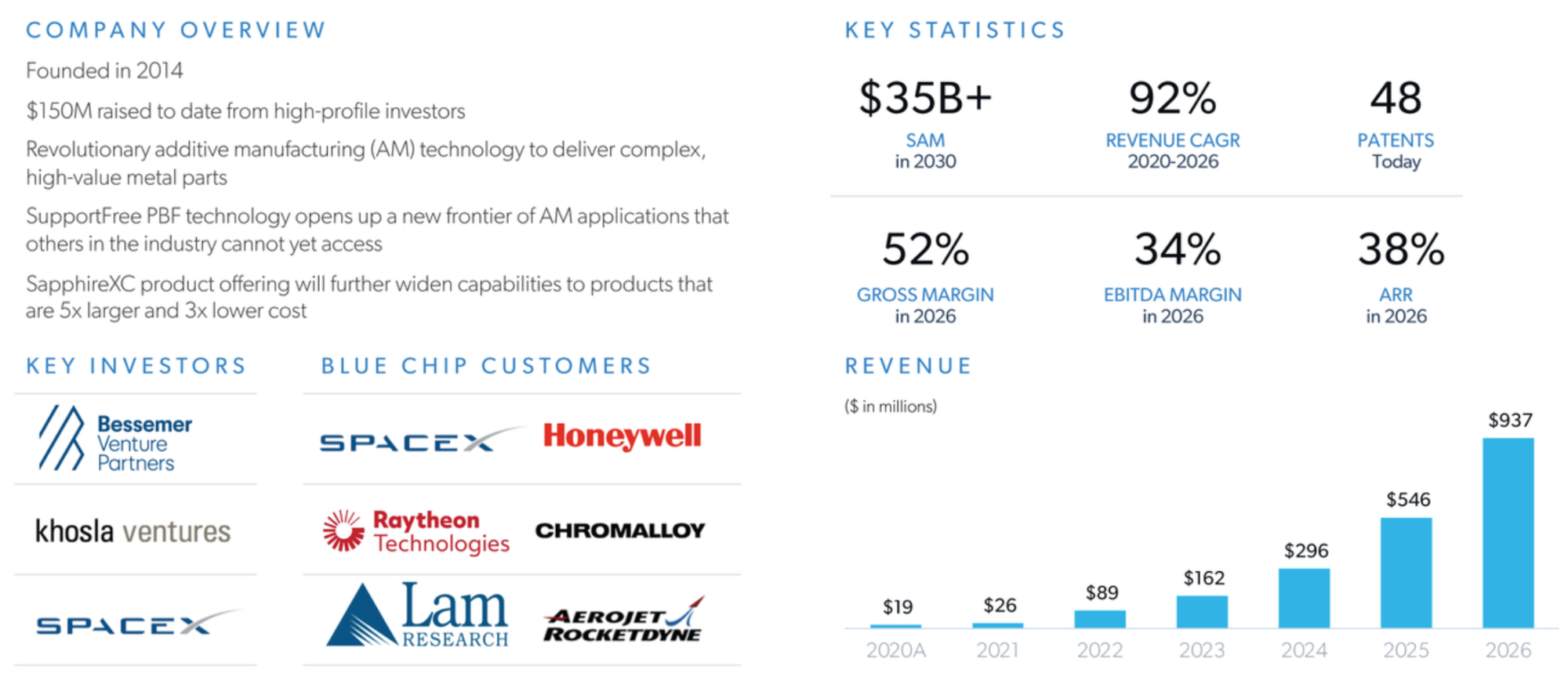

Velo3D (NASDAQ:VELO) is a California-based 3D printing company that was founded in 2014 and went public in 2021 via a SPAC deal backed by tennis superstar Serena Williams, billionaire Barry Sternlicht, and SpaceX. [Pg. 8]

With SpaceX also serving as its anchor customer, along with blue chip technology giants like Raytheon and Honeywell, Velo forecasted that annual revenue would skyrocket from ~$19 million at the time of the SPAC to nearly a billion dollars by 2026.

Instead, Velo’s revenue peaked in 2022 and then sharply declined while the business burned through hundreds of millions of dollars in cash from operating activities. By September 2024, Velo had been delisted from the NYSE, defaulted on its debt, and was on the brink of bankruptcy, according to industry reports.

In December 2024, little-known Indiana businessman Dr. Arun Jeldi appeared on the scene and acquired Velo3D’s distressed debt through his company Arrayed Additive. Subsequently, in a debt-for-equity exchange, he became Velo’s largest shareholder and CEO, controlling 95% of the company’s outstanding common stock.

“My decision to invest in Velo3D through Arrayed Additive stems from the immense potential I see in the combining our companies together. Together, we now offer unmatched metal additive manufacturing capabilities, leveraging the best technologies and expertise from both sides.

This powerful synergy positions us to capitalize on significant growth opportunities in key sectors, including aerospace, defense, automotive and engineering.” —CEO Arun Jeldi, Q4 2024 Earnings Call

Under Jeldi’s leadership, Velo appears on the surface to be experiencing a remarkable turnaround driven by a stabilized financial position and NASDAQ listing, a slew of contracts across the space and defense sectors, and a strategy to generate high-margin revenue from recurring parts sales manufactured in-house by Velo through its new Rapid Production Solutions (“RPS”) division. [1, 2]

A key catalyst for Velo is its supposed relationship with SpaceX, which financial media have leveraged to promote the Velo story to investors.

Over the last 12 months alone, Velo’s stock has rallied 140% and the company now has a market cap of $537 million.

Velo3D Has Fundamental Downside Risk Due To A Nosebleed Valuation Of 10.7x Price To Sales, The Highest Of Any 3D Printing Company And A 858% Premium To Its Peer Average

Velo Also Has Significantly Lower Profit Margins Than Peers, Remains Deeply Unprofitable, And CEO Jeldi Has Pledged Almost 25% Of His Stake In The Company Worth ~$54 Million To Obtain A Margin Loan

Even ignoring our findings entirely, Velo has fundamental downside risk due to its nosebleed valuation relative to virtually every peer on the market. On consensus EV/Sales it trades at a 287% premium to its peer average and 858% on a Price-To-Sales basis, per Bloomberg.

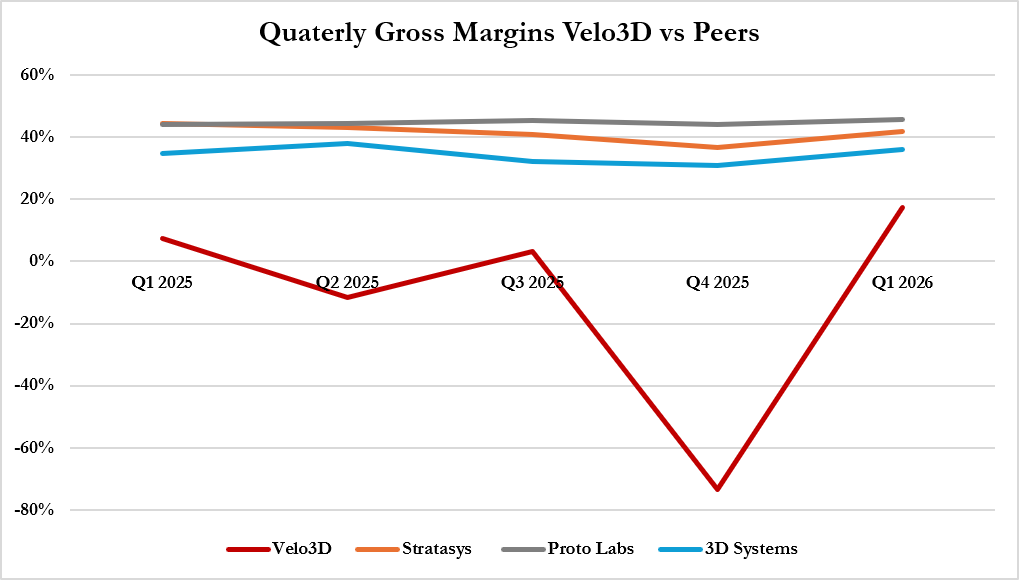

Despite this premium valuation, Velo has incurred losses from operations since inception, racking up an accumulated deficit of $505 million as of Q1 2026. Under Jeldi’s leadership, gross margins have continued to be highly erratic and significantly lower than peers.

Bulls see Velo’s reported 48% year-over-year revenue growth in Q1 as a positive sign, but this seemingly impressive headline figure was driven by an unusually weak quarter in Q1 2025. In reality, Velo’s revenue has been virtually flat since CEO Jeldi took control of the business in Q4 2024.[1]

Q1 2025 was an unusually weak quarter with just $9.3 million in revenue reported. In the previous quarter, Velo reported $12.6 million in revenue and in each of the two subsequent quarters (Q2 and Q3 2025), Velo reported ~$13.6 million in revenue. ↩︎

Velo exhibits other classic red flags, including a high volume of executive turnover, with its CTO, COO, CFO, and VP of Technology departing since Jeldi took control of the business.

Further, Velo has disclosed seven unremediated material weaknesses in controls over financial reporting, including weaknesses related to the “existence” and valuation of inventories, depreciation schedules, and the presentation of “contract assets.”

Under Jeldi’s leadership, Velo has continuously diluted shareholders, increasing its common shares outstanding by 129% from December 31, 2024 to May 12, 2026.[1]

CEO Jeldi has pledged 3 million shares, representing a 25% stake in the company worth an estimated $54 million, as collateral for a private loan, per Velo’s April 2026 proxy statement. Share pledges can be an unstable form of collateral, as falling stock prices can trigger margin calls and forced selling.

Part 1: How Velo3D Fueled Its Recent Run By Promoting A Sham Relationship With SpaceX That Effectively Ended 2 Years Ago

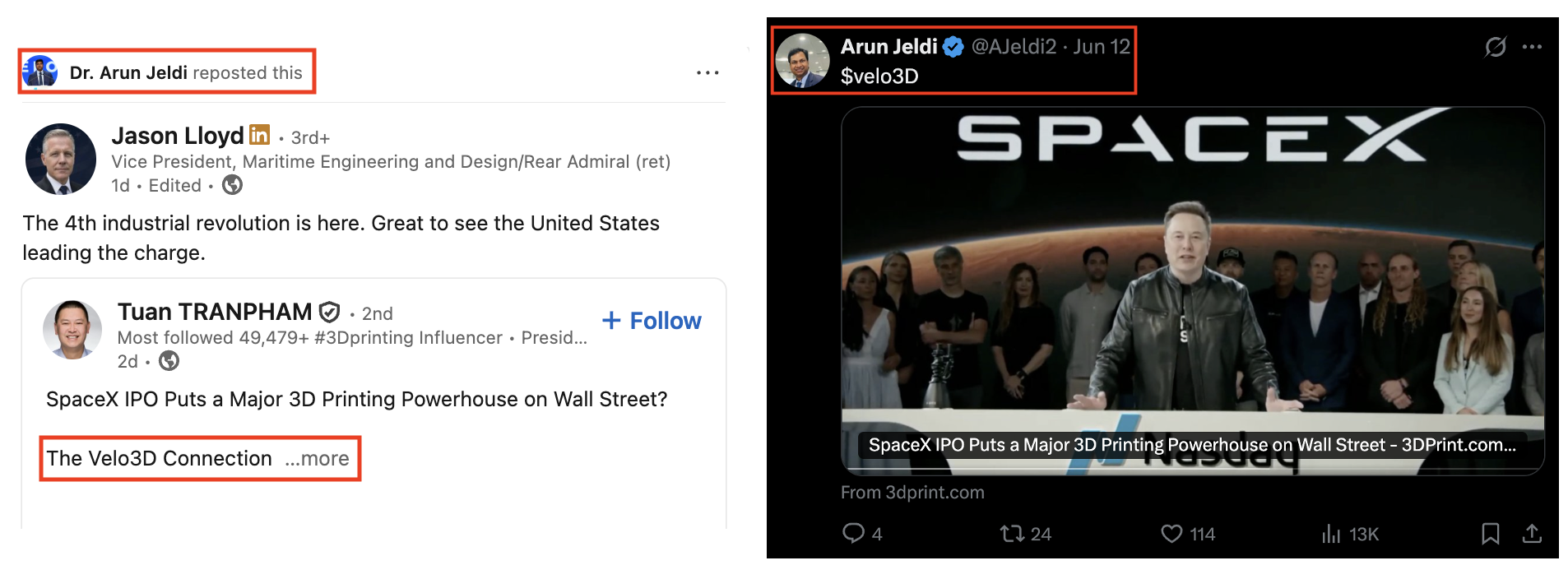

Bulls and the financial media have portrayed Velo3D as a “proxy trade” for SpaceX.

This narrative has also been promoted by CEO Jeldi, who has posted numerous times on his social media accounts about SpaceX.

Velo3D CEO: “SpaceX Is Actually Increasing Their Fleet”

Reality Check: SpaceX Stopped Ordering 3D Printers From Velo3D In 2022 And Signed An IP License Agreement In 2024 That Allows It To Manufacture Its Own Printers In House

Velo’s recent prospectus supplement, filed in August 2025, referred to SpaceX as a “notable customer.”

In December 2025 CEO Jeldi was asked at an investor conference if Velo would generate incremental revenue from SpaceX, and he confirmed that it would.

“Yes. We are still in contact with SpaceX and SpaceX is actually increasing their fleet and also sending us parts to print. So we are in good terms with SpaceX….We are in talks with SpaceX. I can't disclose the deal until it happens, but most likely they will [buy more machines].” —CEO Jeldi at the Winter iAccess Alpha Conference.

In June 2026, he again highlighted the relationship at another industry conference.

“As everyone knows, Velo is well-known for the initial mode of SpaceX machines… The recent Raptor engine and all other 3D, what Elon talks about is specifically, I mean, is a pure Velo platform.” — CEO Jeldi at The Future Tech Investor Conference

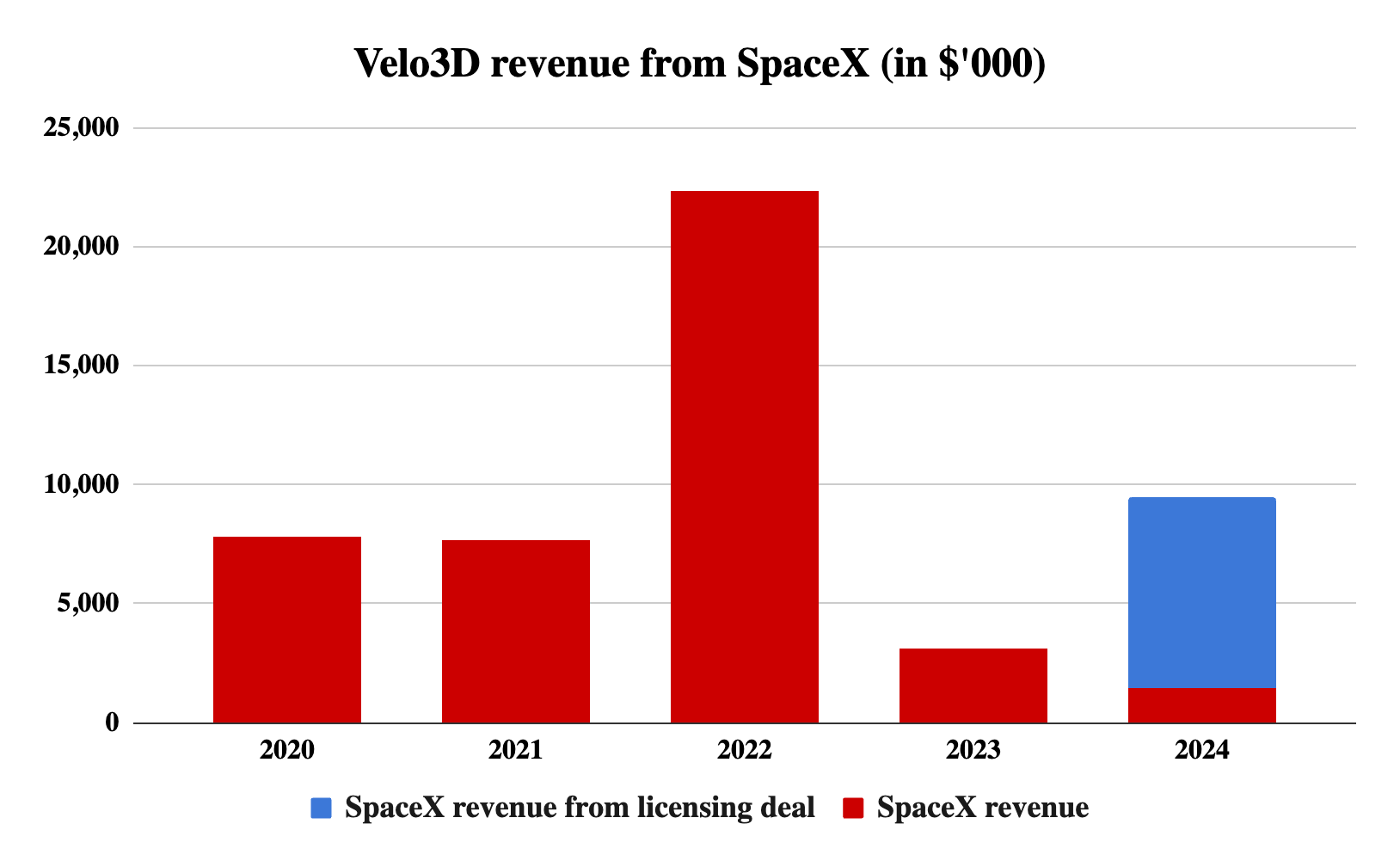

Velo began shipping Sapphire printers to SpaceX in 2018, and SpaceX was its largest customer when it went public in 2021, accounting for 27.8% of revenue, per the company’s 10-K.

By the end of 2022, SpaceX, still the largest customer, had grown its fleet to 26 Sapphire printers, and it represented 28.4% of Velo’s total revenue, per the company’s annual report.

In 2023 Velo stopped shipping Sapphire printers to SpaceX, causing revenue from SpaceX to collapse to 4% of total revenue, per Velo’s annual reports.[1]

As of 2023, Velo disclosed that it had shipped 26 Sapphire printers to its largest customer (i.e. SpaceX). By 2024, the amount of printers shipped to SpaceX had not changed and remained at 26, per the annual reporting. ↩︎

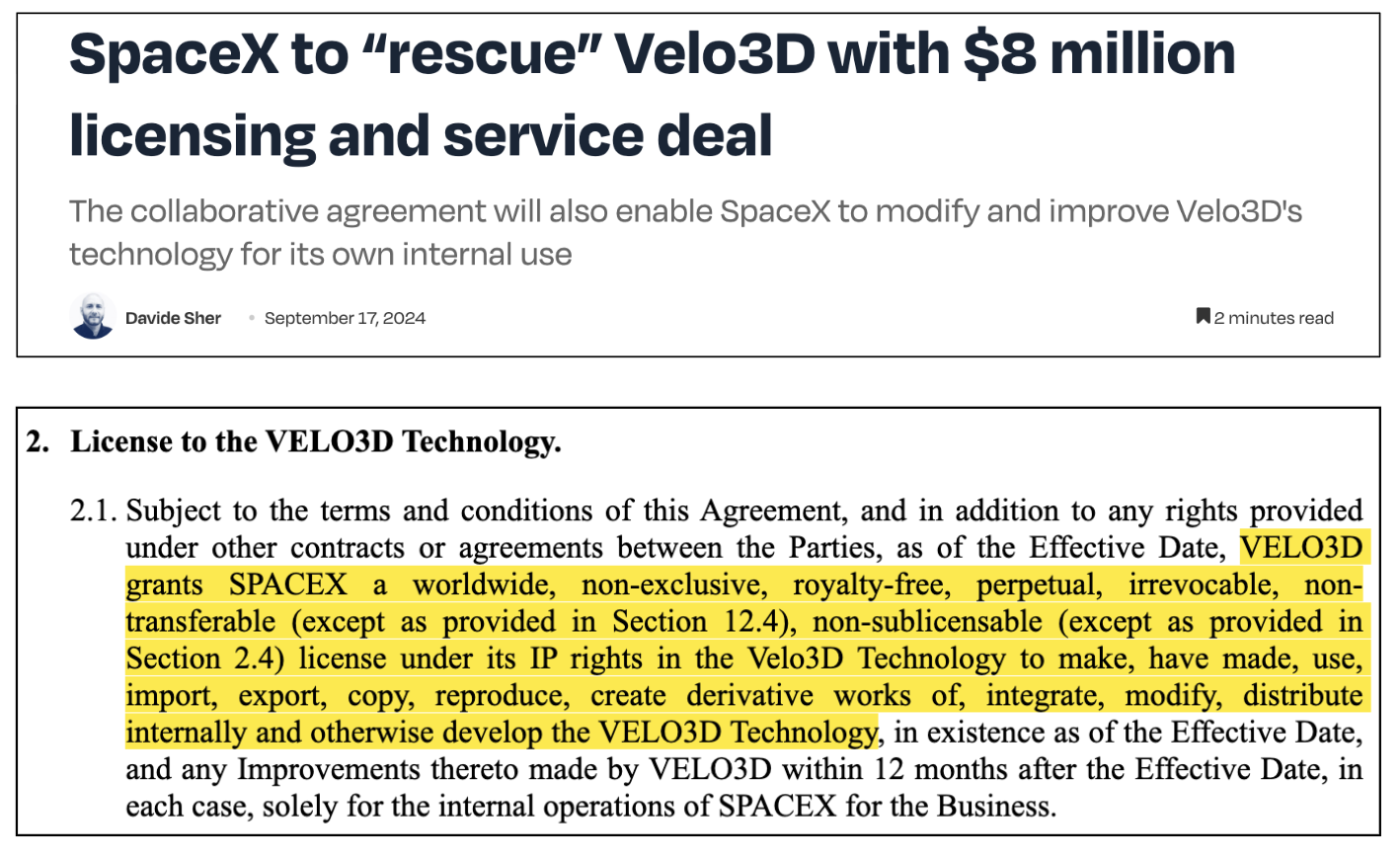

As mentioned, by September 2024, Velo was on the verge of bankruptcy, according to industry reports. This led the company to sell a perpetual, royalty-free, and irrevocable license to its technology to SpaceX for a one-time fee of $5 million in addition to a $3 million support services contract.

On the back of this one-time deal, SpaceX's contribution to Velo’s revenue increased to 23%. Without the $8-million licensing deal, we estimate that 2024 SpaceX revenue would have been ~$1.4 million or 3.4% of total revenue.[1]

The $5-million one-time fee was paid within 3 days after Velo delivered certain items described in the agreement and the $3-million service fee was to be paid during a target period of 3 months, per the licensing contract terms. Velo did not disclose if it had received all the proceeds from the licensing agreement, it only referred to the service revenue as being driven by the licensing agreement. We assumed all the fees associated with the licensing agreement were paid in 2024. ↩︎

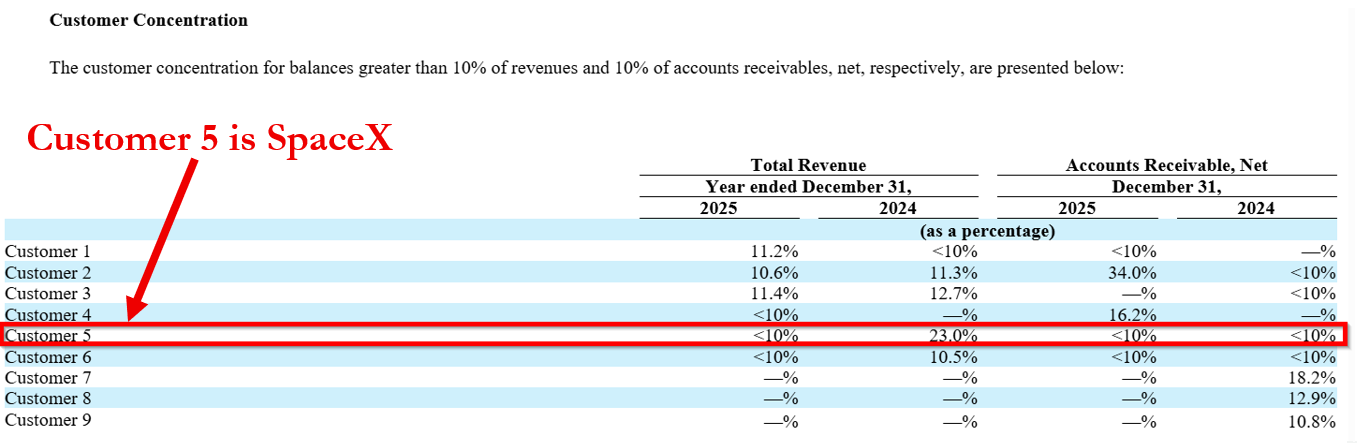

By 2025, SpaceX’s contribution to Velo revenue had fallen below the revenue concentration reporting threshold of 10%.[1]

A former Velo3D employee explained that while a relationship still exists, revenue from SpaceX largely wound down after 2024.

“I think that any revenue related to SpaceX has pretty much ceased to exist since 2024. Anything you're looking back at from now to 2025 has been independent of SpaceX.”

“I Would Be Pretty Skeptical Of [SpaceX] Buying More Printers … We Licensed Them All Of Our IP. 100% Of It … I’d Be Very Surprised If They Ever Bought Another Velo System” - Former Velo3D Senior Leader

The licensing deal effectively allowed SpaceX to manufacture its own machines in-house if necessary, meaning it would never need to return to Velo. We see the deal as the final nail in the coffin for a relationship that largely wound down at the end of 2022 when SpaceX stopped ordering new printers.

Three former Velo3D employees confirmed that SpaceX can now manufacture its own printers if it needs additional capacity.

Former Velo Employee #1: “SpaceX has the option now to just build their own machines with the same technology.”

Former Velo Employee #2: “That deal … gave them the ability to manufacture the printers themselves, right? So, they have a full manufacturing license…”

Former Employee #3: “I would be pretty skeptical of [SpaceX] buying more printers from Velo, and the reason I say that is, in October of 2024, we licensed them all of our IP. 100% of it … I’d be very surprised if they ever bought another Velo system.”

Two of the employees added that SpaceX is actively trying to move away from 3D printing due to how slow and expensive it is.

Former Velo Employee #3: “[SpaceX] also had the right and ability to make their own machines. And I can tell you for a fact, when Elon came and visited our facility on February 14th of 2020, it was clear that he hated 3D printing with a passion … he always thought the machines were way too expensive and way too slow… They did a ton of work to make even the machines that we sold them better. And so, I would think that whoever came to Elon with the ask to buy more Velo printers, would be fired immediately.”

Former Velo Employee #2: “What SpaceX told [redacted] very clearly is their internal objective at this stage is to eliminate 3D printing and only use it where they have to … Elon and SpaceX always viewed 3D printing as a bridge, with the idea that at higher volumes, casting and other manufacturing technologies would just be more cost effective.”

A former employee explained that there has been little effort from Velo or SpaceX to continue the relationship, and that SpaceX has found an alternative to Velo that can produce at least one of the parts previously made on the Sapphire.

“The reality of that is that Velo is no longer in business with SpaceX … There has been minimal effort on both sides trying to continue that relationship. And the reason for that is that, number one, SpaceX have found an alternative to the solution Velo can provide. From my understanding, it's a combination... of another OEM plus the internal software development that they were able to produce the part that previously only can be printed on the Velo machine.”

We believe Velo’s SpaceX relationship is virtually dead and has been since late 2024. Even if SpaceX wanted more Sapphire printers, it has the license to manufacture them in-house with zero additional fees paid to Velo.

Part 2: Velo3D’s “Defense And Aerospace” Pipeline Is Stuffed With Highly Speculative Deals That Are Unlikely To Result In Significant Revenue

In addition to its supposed SpaceX proximity, Velo’s rally has been driven by a new focus on defense, space, and government customers for both its printer and parts (RPS) businesses.

Since CEO Jeldi took control of the business in late 2024, Velo has announced a slew of deals that seem impressive on the surface, but which contain little to no substance, in our view.

In April 2025, Velo Signed A $15 Million RPS Deal With Space Startup Momentus, A SPAC That Paid The SEC $8 Million To Settle Charges Related To Misleading Investors, Followed By A 99% Decline In Its Share Price

As Of March 2026, Nearly One Year Later, Velo Had Booked Zero Revenue From Its Relationship With Momentus

A Former Senior Leader From Velo Told Us: “In My Mind, That Was A Bit Of A Distraction … That Seemed Like An Effort To Create A Press Release For Us, Quite Frankly”

In April 2025, Velo announced a $15 million RPS deal with Momentus, a satellite startup.[1]

This was a 5 year deal with $3 million per year target value. Under the agreement, Velo received Momentus shares as consideration for future services subject to a “refund provision.” ↩︎

Momentus went public during the 2021 SPAC boom. In July 2021, Momentus was charged by the SEC for misleading claims about its technology, as well as national security risks associated with its then CEO.

Momentus shares have cratered 99% since it went public and it reported less than $4 million in combined revenue during 2024 and 2025. Its most recent annual report included a going concern warning.

As of March 2026, almost a full year into the relationship, Velo appears to have booked zero revenue from the Momentus deal, according to its financial statements. [1, 2]

We asked a former senior leader from Velo about the deal, and they said that they viewed the announcement as a promotional effort.

“I think that, so [Momentus], in my mind that was a bit of a distraction… I don’t know that in my mind it was anything that seemed like an effort to create a press release for us, quite frankly.”

In December 2025, Velo3D Announced A Contract With A “Total Value Of $32.6 Million” To Support The Department Of War’s Defense Innovation Unit, Which Analysts Have Characterized As A “Significant Opportunity” And “Further Evidence” Of Velo’s Momentum In Defense

Reality Check: The DoW Has Only Funded ~9% Of The Program, Which Is Scheduled To End In ~3 Months, And Does Not Appear To Have Been Extended

In March 2026, Velo Competitor Nikon SLM Announced A New 12-Month Award Under The Exact Same Program

In December 2025, Velo announced a $32.6 million contract from the Department of War to support a “major weapon system” program known as Project FORGE.

CEO Jeldi described the deal as a “key” contract, while the sell side characterized it as a “significant opportunity” and “further evidence” of Velo’s penetration into the defense sector.

“We think the $32.6M win illustrates both the significant opportunity in the A&D sector and Velo’s continued momentum … We view this win as further evidence of the Company’s momentum in this market, which we believe will continue throughout 2026 and 2027.” — Lakestreet Capital, December 2025

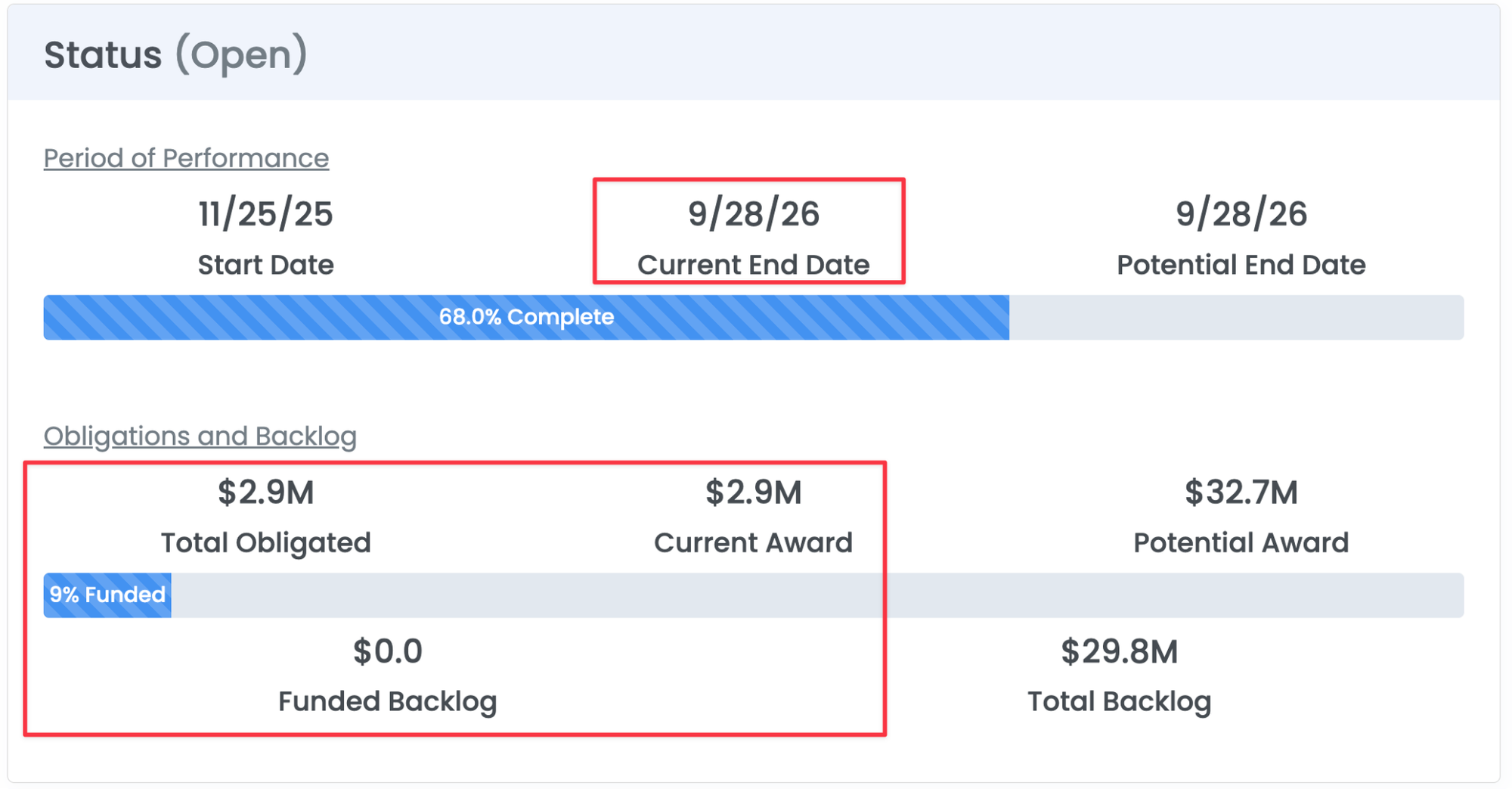

Despite the headline deal value, Velo is on track to earn substantially less. As of this writing, according to HigherGov, a government contracting database, the DoW has only funded 9% of the program, or approximately $2.9 million. The project is scheduled to end in ~3 months.

In March 2026, Velo competitor Nikon SLM announced a new contract with the DoW’s Defense Innovation Unit (DIU) through the Project FORGE program. The Nikon SLM press release quoted Derek McBride, the same DIU program manager who was originally quoted in the Velo announcement.

In December 2025, CEO Jeldi Stated That Velo Works Directly With Lockheed Martin, But Former Velo Employees Told Us That Lockheed Left Velo For Competitor Nikon SLM

“I Know Lockheed, They Used To Engage With Us, But They Have Decided Not To Use Our [Velo] Product.” - Former Velo3D Employee #1

“Obviously, There Was Like Such A High Level Of Dissatisfaction From The Lockheed Guys That They Were Like, Screw It” - Former Velo3D Employee #2

Beginning with Velo’s SPAC deal in 2021, it has named Lockheed Martin as a customer. More recently, under CEO Jeldi’s leadership, the Lockheed Martin relationship has been reaffirmed multiple times.

For example, at a December 2025 conference, CEO Jeldi told investors that Velo3D was working with Lockheed.

In April 2026, however, Lockheed published a write-up on its use of Laser Powder-Bed Fusion (LPBF) additive manufacturing – the same type of technology employed by Velo3D. Lockheed included a list of 3D printing partners such as EOS and Nikon SLM – direct competitors to Velo – while Velo3D itself was notably absent.

A former Velo employee explained that Velo has lost Lockheed’s business.

“They [Lockheed] used to engage with us, but they have decided to not use our product.”

Another former Velo employee attributed Lockheed’s decision to leave Velo due to a “high level of dissatisfaction” with Velo.

“Lockheed and Nikon have made public their relationship… I think was a direct result of the way that the relationship with Lockheed was mismanaged [by Velo] in those years with the old leadership.”

“Obviously there was like such a high level of dissatisfaction from the Lockheed guys that they were just like, screw it.”

Velo’s most recent annual report included new disclosure language that has not appeared in previous reports, which states that some of Velo’s listed blue-chip customers may now be “prior” customers.

We believe Velo has lost a material portion of its business with Lockheed, if not the entire relationship.

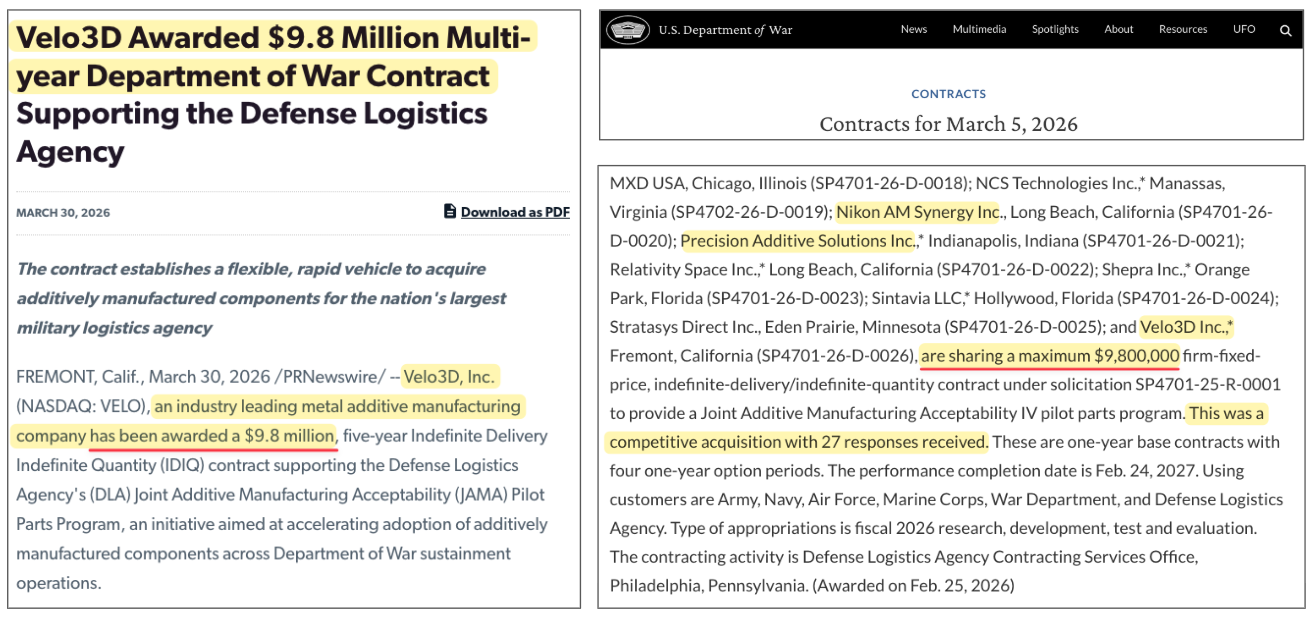

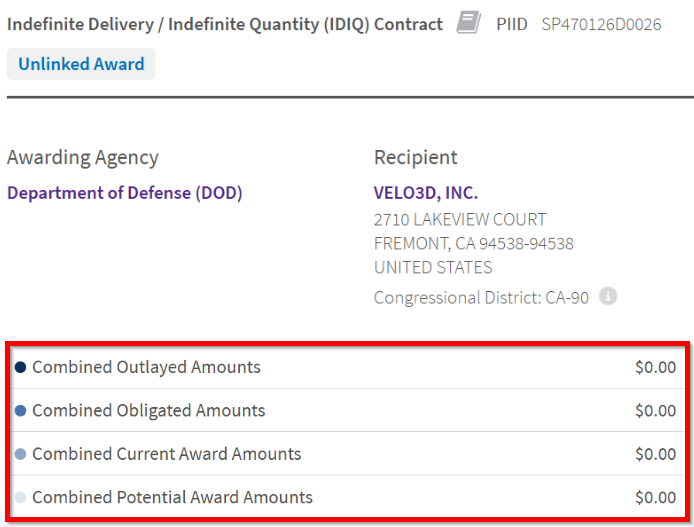

In March 2026, Velo Announced A $9.8 Million Multi-Year Award From The Department Of War To Support The Defense Logistics Agency’s “Pilot Parts Program”

CEO Jeldi Called The Award “Strategically Important” And Claimed That It Positions Velo At The “Forefront” Of The Military’s Adoption Of Additive Manufacturing

Reality Check: Velo Was 1 Of 24 Awardees That Will Share The $9.8 Million Award, If There Is Any Funding To Share At All – The Program Was Unfunded By The Government With Zero Dollars Obligated To Velo As Of June 2026

In March 2026, Velo announced a $9.8 million award from the Department of War (“DoW”) to support a pilot parts program for the Defense Logistics Agency (“DLA”).

At face value, the award appears to represent further evidence of Velo’s penetration into the defense sector, especially considering the commentary from Velo CEO Jeldi during Velo’s Q1 2026 earnings call.

“In March, we also announced that Velo3D was awarded a $9.8 million 5-year IDIQ contract with the Defense Logistics Agency … This award is strategically important, and the reliability of our technology for mission-critical applications. And third, it positions us at the forefront of the Department of Defense's adoption of additive manufacturing solutions designed to improve readiness, resilience and supply chain flexibility.”

Yet, Velo failed to communicate that the contract was awarded to 24 out of 27 bidders, who will “share” the total of $9.8 million available under the deal, per the DoW‘s own website.

As of June 23, 2026, zero dollars have been obligated towards Velo under the program, according to government contracting database USASpending.

In other words, this opportunity guarantees no material revenue for Velo, remains unfunded by the government, and Velo will have to compete with 23 other firms for just a piece of the $9.8 million total.

Part 3: Outdated Technology, Unreliable Machines, And An RPS Pivot That Velo’s Former Employees Do Not Believe In

In a September 2025 interview, CEO Jeldi explained how Velo’s technology is unmatched because no other printer OEMs can deliver what defense and space companies want.

We believe that Velo3D had a niche competitive advantage for especially large components and unique geometries when it first launched, but that this edge has largely eroded with the launch of larger, state-of-the-art 3D printers from competitors like EOS and Nikon SLM.

Further, we uncovered substantial reliability, service, and automation issues with Velo’s printers that we believe have driven reduced market demand. While the company is attempting to pivot to RPS – selling in-house printed parts – former employees expressed skepticism that this pivot will be successful.

Industry Experts Told Us Velo’s 3D Printers Have Major Reliability Issues, Are Prohibitively Expensive, And Are Rapidly Being Outcompeted By “Industry Favorites” Nikon SLM And EOS

A Former Velo Employee Told Us That “The Reliability Of These Machines Is Very, Very Questionable Comparing To EOS Or SLM” And Described Velo’s Printer As A “Science Experiment” And An “Unfinished Product”

Throughout our investigation, industry experts explained that Velo had a competitive advantage early on due to its ability to print especially large parts with unique geometries. A former senior leader from Velo told us:

“It became clear that Velo, the reason it was working at all, was Velo had capabilities that nobody else in the marketplace had… what that resulted in was customers that had a very high tolerance because they didn’t have any other choice.”

The former Velo senior leader explained, however, that competitors are “closing the gap” on Velo’s unique capabilities.

This sentiment was echoed by a former SpaceX employee who described technology advances from competitors like Nikon SLM and EOS, who they referred to as “industry favorites.”

“Players like [Nikon] SLM, they are advancing their technology to be able to develop and print higher complexity, greater geometry type parts, adding more and more lasers to improve speed … And from a reliability standpoint, like I said, EOS and SLM are what I would call industry favorites right now.”

Other industry experts, including former Velo employees, spoke of significant reliability issues with Velo’s Sapphire printers. For example, a former Velo employee explained that reliability is “questionable” on Velo’s printer, which he described as an “unfinished” product and a “science experiment.”

“The reliability of these machines is very, very questionable comparing to EOS or SLM. So, a target uptime for an EOS and SLM machine is between 60 to 80 [percent] machine. But on the customer base that I've talked to quite often, the expected uptime for Velo machine is between 20 to 40% … now you have to invest a lot of money to own the machine, but the machine is not producing the throughput that was expected.”

“The gap here is reliability. I’m talking about the ability to make things repeatedly over and over. And what leads to that is that the machine was never really designed for production … the term that has been used for the Velo machine is what they call a science experiment … it looked unfinished as a product.”

A second industry expert, a former senior leader from Velo, echoed these concerns about reliability.

“And when you looked at all of the other customers, what you found was they were getting on a good day, 20% utilization out of their equipment. Your best-in-class were up at 40 to 50% utilization… If you look at an EOS tool, for example, they're pretty reliably up in the 70s.”

“These are very complex systems to run. Reliability is inherently kind of low. Just the manufacturing from machine to machine, that reproducibility is relatively low. And I hate to say that, but one of the things that became very clear to me coming into the company was the documentation and standardization around building the machines was very limited.”

A third Velo employee explained that the reliability of Velo’s printers has created fear in the marketplace.

“The market still is worried about investing in buying a Velo3D printer because of all the reliability issues they've heard in the field.”

We interviewed an additive manufacturing expert who spent 10+ years comparing 3D printers on behalf of a leading defense contractor. They told us that Velo’s printer “tends to break down a lot” and that “its uptime is notably a problem.” The expert also confirmed that the Nikon SLM “NXG” model now competes directly with Velo for “large scale components.”

A senior leader from Nikon SLM said that they had heard of significant issues with the original fleet of printers that Velo sold to SpaceX, per a leading expert network database.

"When Elon Musk bought 10 machines and put them at SpaceX… the SpaceX engineers basically spend a year reengineering them to make them work like they would perform as sold. So now I wasn't there. That's a rumor, that's gossip, but I heard it from three different companies"

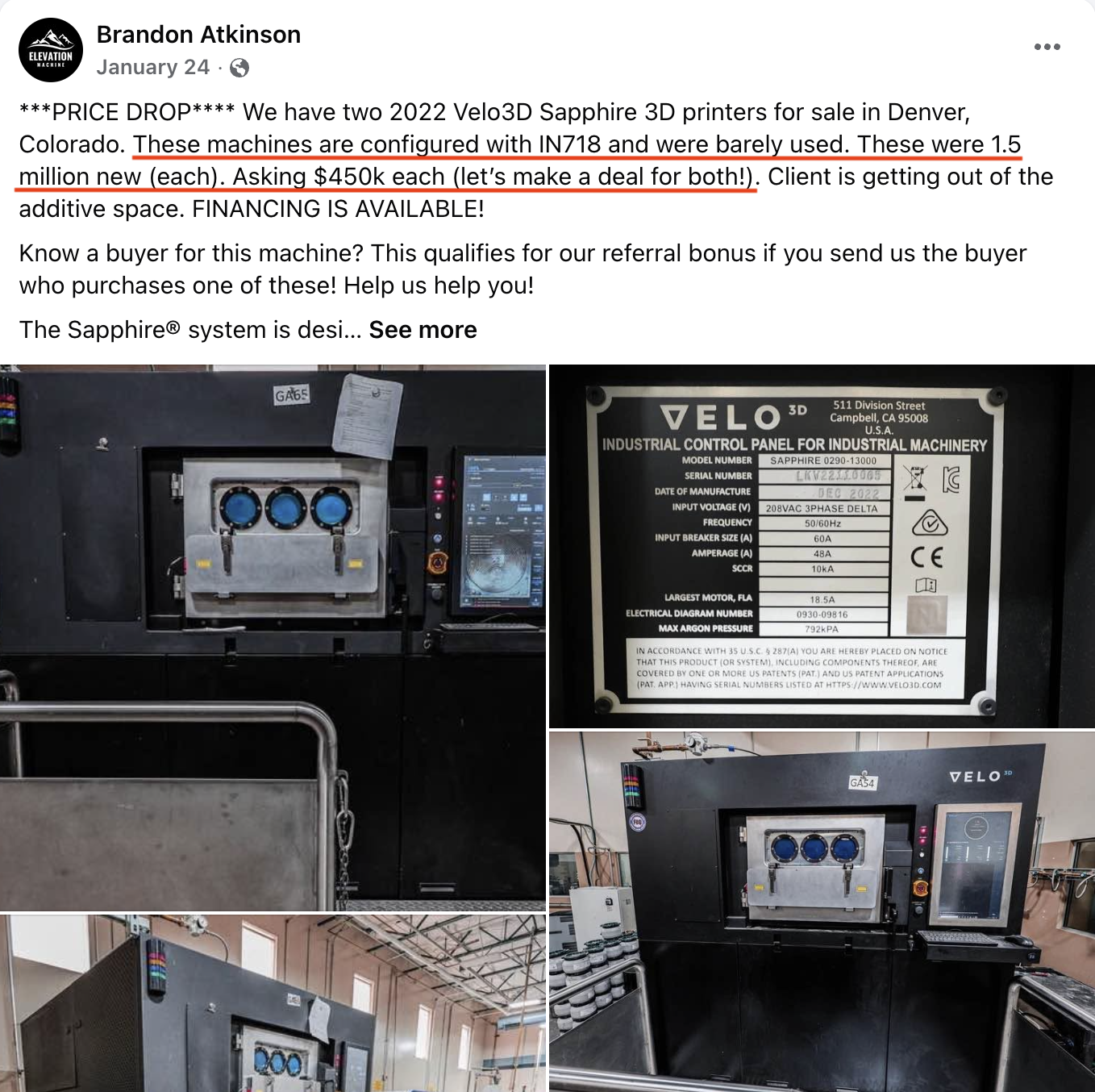

Overall, we believe there is little demand for Velo’s printers due to reliability issues and a rapidly eroding technological advantage. Supporting this, two “barely used” Velo3D printers were placed for sale on Facebook marketplace in January and February at a third of their original price, according to a Facebook post

Former Velo Employees Expressed Little Faith In The Company’s Ability To Pivot To Profitable RPS Operations

“My Conclusion Is That With The Current Technology That Velo Has, They Are Not Ready To Do That [Bring Production In-House]. They Will Be Losing Money” - Former Velo Employee #1

“I Still Have Strong Reservations … Is That A Business Model That, At The End Of The Day, Can Really Be Profitable And How Successful It Will Be” - Former Velo Employee #2

Bulls believe Velo’s RPS pivot positions it as the “go-to additive manufacturer” for aerospace and defense, and CEO Jeldi has stated that Velo will become the “AWS” of defense manufacturing.[1]

See Lake Street Capital research notes from April and May 2026. ↩︎

Former Velo employees, however, were skeptical that the business could effectively compete in parts production and achieve profitability. One former senior leader from the company told us:

“I still have strong reservations around … is that a business model that, at the end of the day, can really be profitable and how successful it will be … While there’s a lot of great things in Velo… I question long-term the economics of that business in general, right? …

I think competition is coming, I think as the technology gets more and more commoditized, I think so much of what Velo would have needed to have done early on has not happened, and I question their ability to remain competitive over a longer time horizon.”

Another former employee explained that, in their analysis, Velo could not run a profitable RPS business with its current technology, highlighting reliability issues and minimal automation.

“I ran my own model of if they should be bringing the production in-house … from that analysis, my conclusion is that with the current technology that Velo has, they are not ready to do that. They will be losing money.“

"Because there's so much technical debt in the machine, it requires an army of people to operate this machine, like day in, day out, run multiple shifts… there's virtually minimal automation."

A third former senior leader from Velo explained that by pivoting to RPS, the company is simply bringing reliability problems “in house,” and noted that part of Velo’s fleet is coming from customer buybacks from deals that “went south.”

“If we just abandon that and say we're going to be a production facility, then, like you say, all we're doing is bringing all those problems into our own hands and having to deal with them here in-house. To be quite frank with you, I didn't really see a lot of traction sticking to that concept of trying to fix our internal issues. It was like, boom, shift to production, that's going to solve all our problems.”

"Some of them [printers for the in-house fleet] were customer returns. Some of them were buybacks… from deals that went south for whatever reason. And then some are new builds.”

Part 4: CEO Jeldi’s Biography Contains Egregious Exaggerations, Outright Fabrications, And Omits A History Of Bad Business Deals & Litigation

CEO Jeldi claims to be a doctor who practiced medicine for several years before becoming an entrepreneur, supposedly building a $50 million medical company and bootstrapping several “multi-million dollar” manufacturing startups.

In this section, we reveal that much of Jeldi’s background appears to have been widely exaggerated. Rather than a successful business empire, we found a web of shell companies, defunct or dissolved businesses, and a trail of litigation against Jeldi from creditors, landlords, and other counterparties.

Finally, we found a concerning association between Arun Jeldi and his brother Bala Jeldi, who reportedly tried to flee the country of India after facing civil and criminal cases related to a failed Magnesium venture where he allegedly defrauded investors.

CEO Arun Jeldi Claims To Be A “Doctor” Who Practiced Medicine For Years Before Entering The World Of Manufacturing

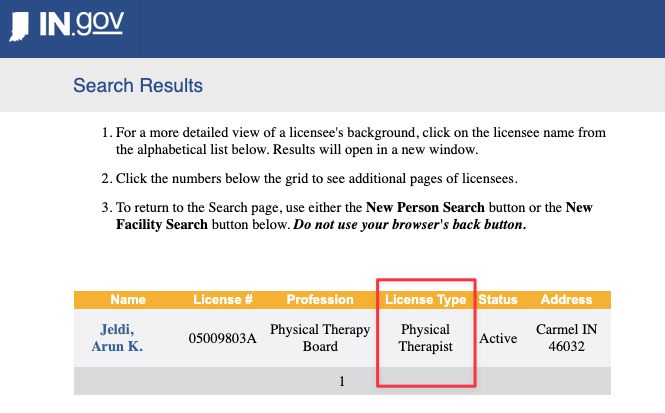

We Were Unable To Identify A Single Jurisdiction Where He Is Licensed As A Medical Doctor Or Any Evidence That He Ever Practiced Medicine

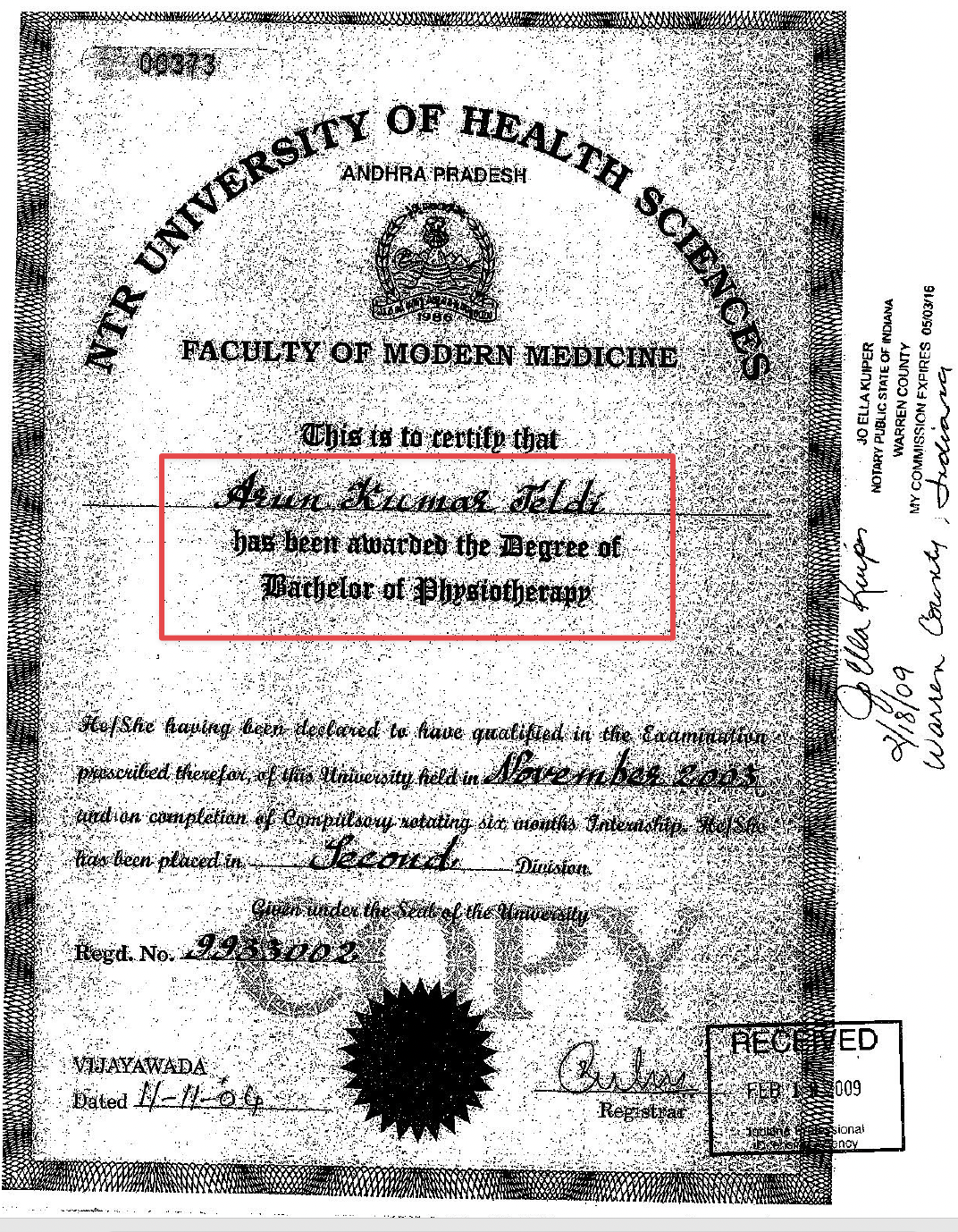

His Highest Level Of Education Appears To Be A Bachelor’s Degree In Physical Therapy

Velo’s CEO Arun Jeldi refers to himself as a doctor on both his LinkedIn profile and in the professional biography featured on Velo’s website.

In a September 2025 interview, he claimed that he “practiced medicine for 3 years” prior to entering the world of manufacturing. He does not clarify, however, where he received his medical degree.

Public records show that Jeldi has only resided in Indiana and California for the last 17 years. We checked Indiana and California state records for evidence that “Doctor” Arun Jeldi has ever had a license to practice medicine, but all we found was a physical therapy license.[1]

Indiana physical therapist license No. 05009803A. We also found a physical therapist license in Michigan (physical therapist license No. 5501014033). ↩︎

Jeldi’s application for a physical therapist license in Indiana disclosed that his highest level of education was a bachelor’s degree in physical therapy obtained in 2004. [Pgs. 1, 4]

While it would be a stretch for someone with a doctorate in physical therapy to say they “practiced medicine" and to refer to themselves as a doctor, Jeldi does not even appear to have a doctorate at all - having earned only a bachelor’s degree.[1]

Up to his 2018 license renewal, Jeldi stated that his “degree/credential” which qualified him for his first “U.S. physical therapist license” was a “Bachelors.” His 2020 and 2022 renewal applications, however, stated that the degree which qualified him for his first “U.S. physical therapist license” was a “Doctor of Physical Therapy.” ↩︎

Jeldi Claims That After “Practicing Medicine,” He Started A “Medical Company” That He Bootstrapped From A $10,000 Investment Into A $50 Million Business, Which We Believe Was His Staffing Business “INK Staffing”

Reality Check: By August 2025, Jeldi’s INK Staffing Had Defaulted On Millions In Loans, And When Its Lender Tried To Serve A Notice Of Default, It Found A Vacant Building With “No Business Activity”

We Only Found 4 Employee Reviews For This “$50 Million” Business, One Of Which Referred To The Owner As A “Habitual Liar” And Another That Accused The Owner Of Skimming Money From Paychecks

In a September 2025 interview, Arun Jeldi explained that he began his entrepreneurial journey by founding a medical company, which he says he grew into a $50 million business from an initial investment of just $10,000.

“My background is, I come from a medical background. I practiced medicine for 3 years and I felt like that’s not for me, and I quit that. And I started a, my first startup, a bootstrap, I started a medical company. And, um, I grew that company from investing about $10,000 dollars to $50 million dollars in 3 ½ years, expanded that to nationwide.”

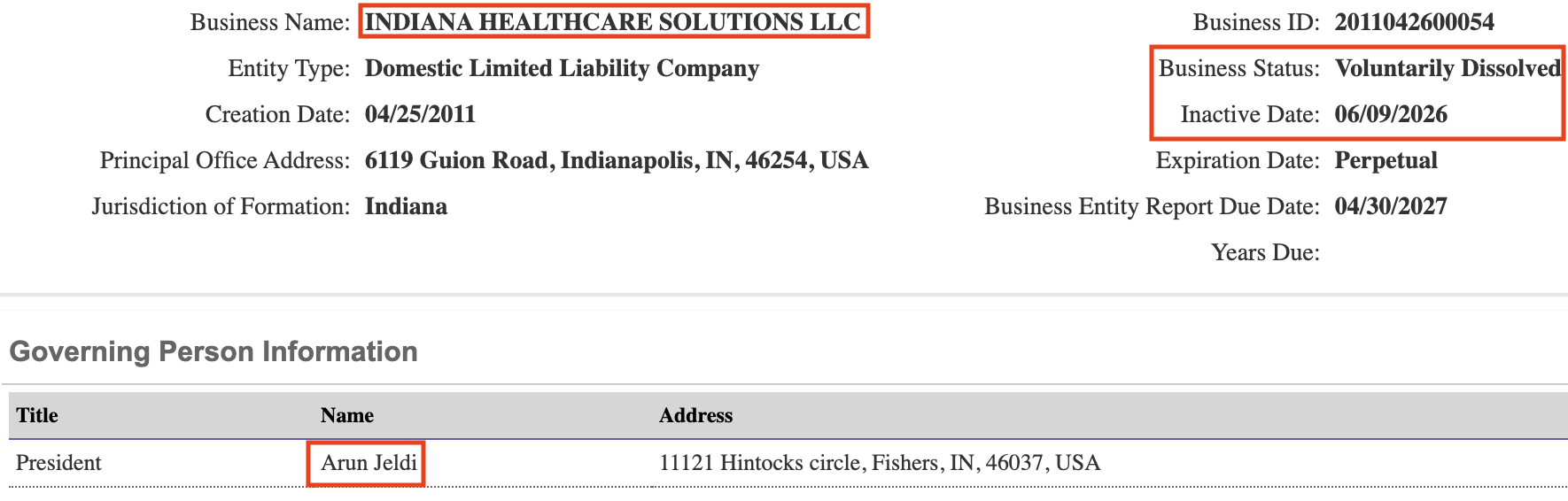

Jeldi’s LinkedIn profile states that he has acted as president of Ink Staffing since 2014. However, his official biography states that he has served as the CEO of Indiana Healthcare Solutions (DBA Ink Staffing) since 2019.

We find it hard to believe that this staffing company was a “$50 million” business, as Jeldi claims, especially since Jeldi renewed his physical therapy license in 2022 and stated that he was spending 21 - 24 hours per week in direct patient care.

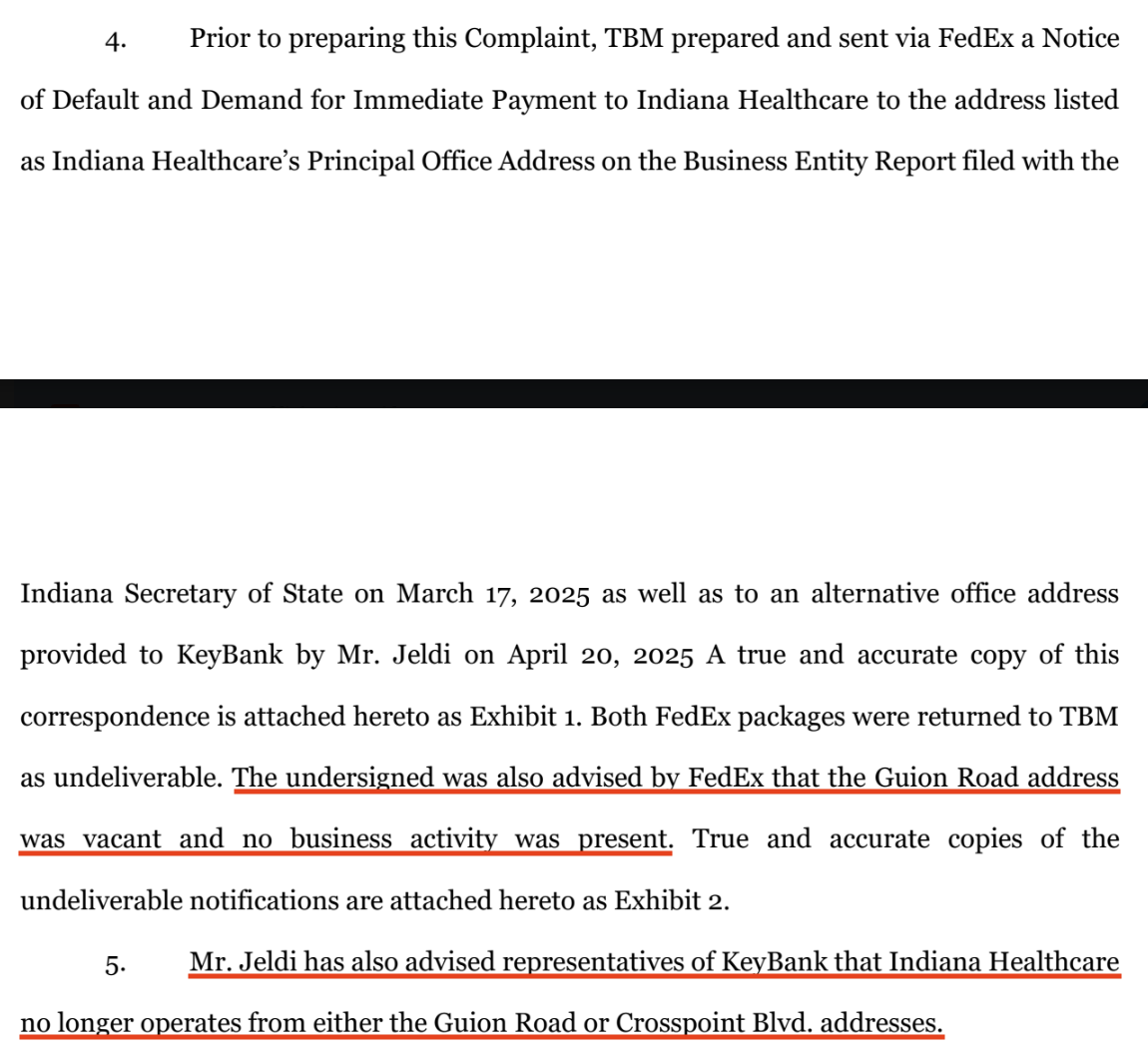

By August 2025, Jeldi’s staffing business had defaulted on $3.6 million of loans and was being sued by lender Keybank.[1]

In March 2026, Keybank terminated its charge against Jeldi, indicating the case was settled. ↩︎

When its lenders attempted to serve a Notice of Default to the company’s listed address, they found the building vacant with “no business activity.” Jeldi later admitted that the business no longer operated from that address.

Today, the job board on INK Staffing’s website leads nowhere, while the listed address is still the Crosspoint office – the same office that Jeldi has admitted he no longer operates out of in the aforementioned litigation.

We would expect to find a large volume of employee reviews for a $50 million staffing business. Instead, we found just 4 reviews, one of which referred to the owner, ostensibly Jeldi, as a “habitual liar” while another alleged the owner was “skimming” money from paychecks.

3 weeks ago, Jeldi dissolved the entity entirely.

In short, we do not think Indiana Healthcare Solutions (DBA INK Staffing) was ever a $50 million business, but instead a very small and financially distressed staffing firm that now appears defunct.

Jeldi Claims That After Successfully Building A Healthcare Company, He “Bootstrapped” 4 Manufacturing Startups, Which All Became Revenue-Generating “Multi Million Dollar” Businesses That He Continues To Lead As CEO

One Of These Companies Is Arrayed Additive, Which He Has Described As A “Leader In Magnesium And Aluminum 3D Printing” That Would Bring Substantial Synergies To Velo

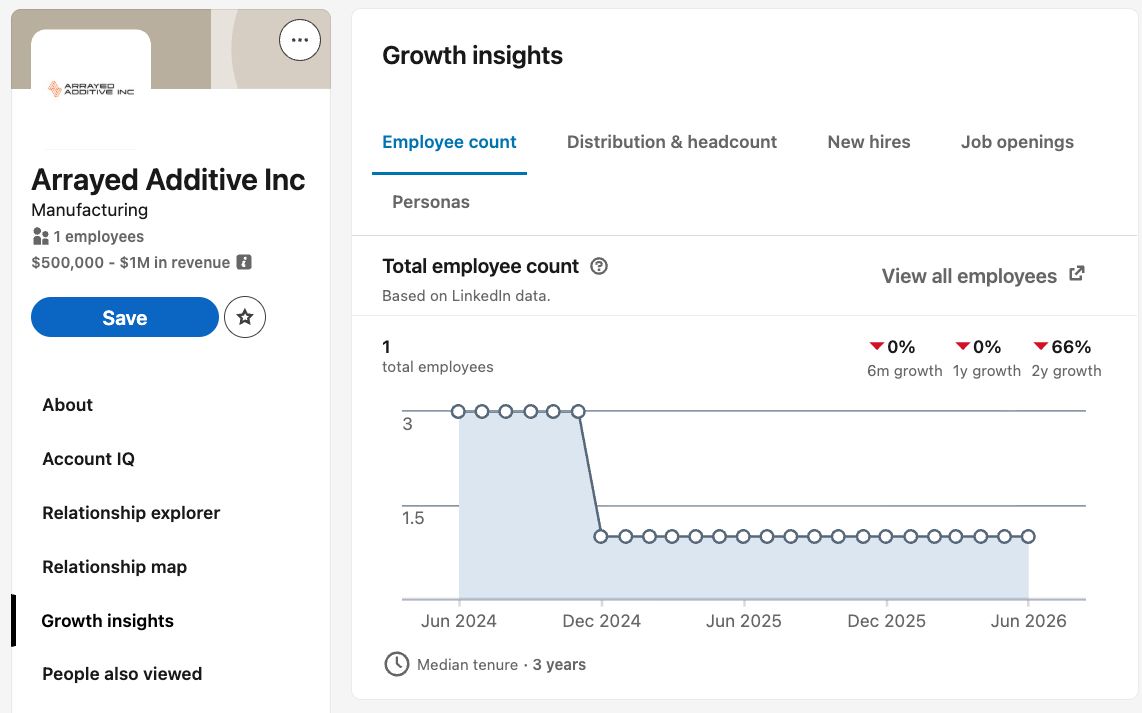

Reality Check: Arrayed Additive Has No Discernible Commercial Operations, Is Based Out Of The Same Abandoned Address As Jeldi’s Defunct Staffing Business, And Has A Single Employee On LinkedIn: Arun Jeldi

Jeldi claimed in a September 2025 interview that after his healthcare company became successful, he bootstrapped 4 companies in the manufacturing industry. In a more recent interview, he claimed that all 4 are multi-million dollar companies that he currently runs as CEO.

Based on Jeldi’s bio, we identified one of these companies as Arrayed Additive, the entity through which Jeldi acquired his Velo3D stake. Jeldi has described Arrayed Additive as a leader in “magnesium and 3D printing” and claimed that the combination of Velo and Arrayed would create substantial synergies.

We found no evidence of Arrayed Additive’s market leadership — or any commercial operations at all.

Arrayed Additive’s website lists the same address as Jeldi’s defunct staffing business – an address he has admitted he vacated and which is currently available for lease. Further, Arrayed Additive has no employees on LinkedIn except for Jeldi himself.

When we interviewed former Velo employees about the synergies from the combination with Arrayed, they said there were no synergies and referred to the company as a “shell.”

“Arrayed was, I don’t know, from all I could tell, a shell … Arrayed didn’t have any products. Like, Arrayed didn’t sell anything. They didn’t make revenue … There was never any customer synergy or market synergy.”

Jeldi Claims To Be The CEO Of “Lite Magnesium,” Which Allegedly “Designs And Manufactures” Magnesium Components For The Aerospace Industry

Reality Check: Lite Magnesium Is A Serial Defaulter Of Lease Payments, Has A Single U.S. Employee, And Its Headquarters Is Vacant

Jeldi’s biography states that he is the CEO and President of Lite Magnesium Products, which “designs and manufactures” magnesium components for the aerospace industry.

Lite Magnesium has just one U.S. based employee on LinkedIn and its website is full of stock photos.[1]

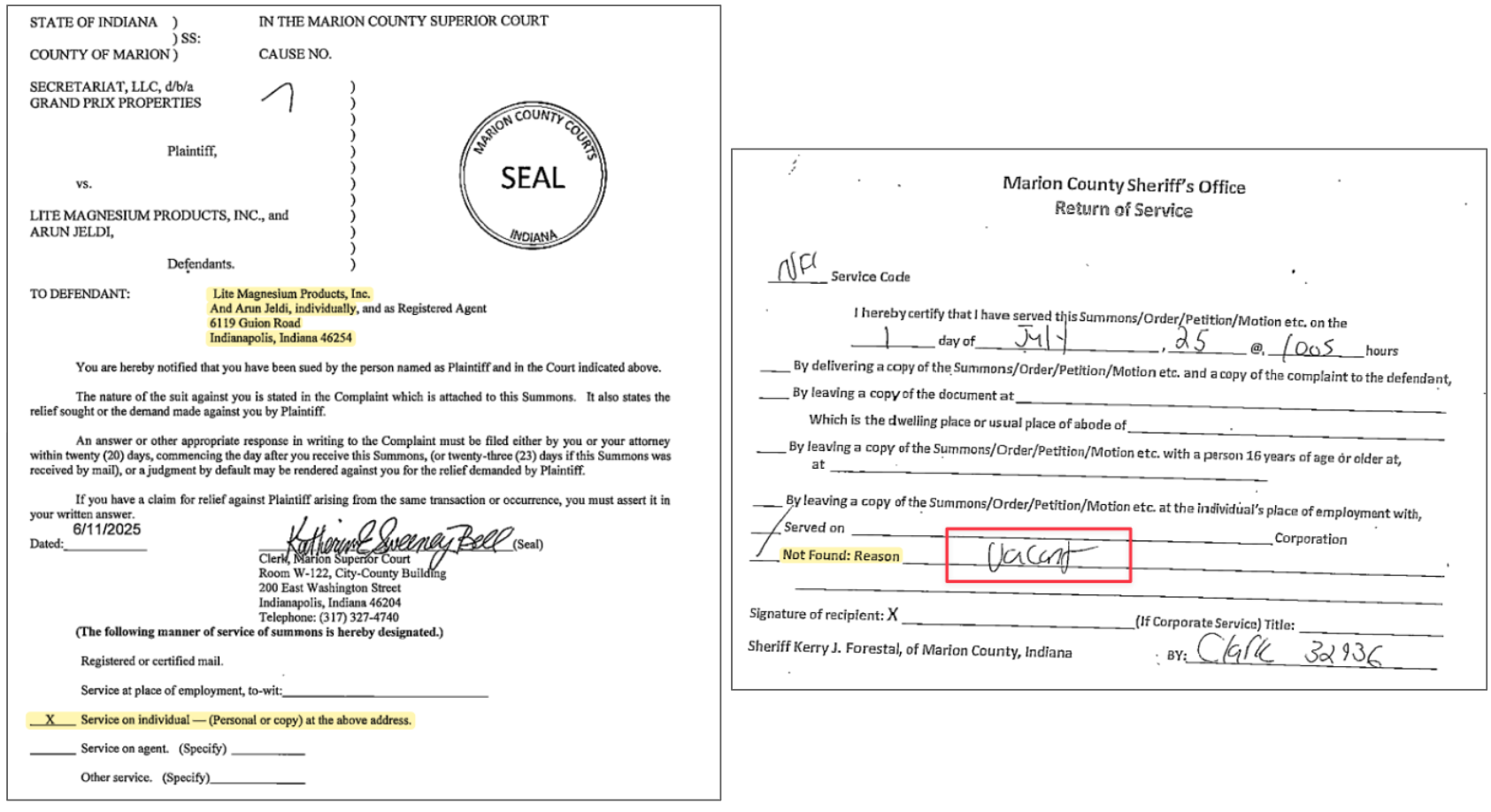

Further, its listed address is 6119 Guion Road, the very same address where Jeldi’s healthcare business was allegedly based, but where creditors found an empty building with no business activity. As stated above, the space is currently available for lease.

In June 2025, Lite Magnesium Products and Jeldi were sued by a landlord for this facility for failing to make lease payments. When the landlord attempted to serve Jeldi at this location, they also found the building vacant, just like creditors of Jeldi’s healthcare business. The parties, including Arun Jeldi, entered into a mutual release and settlement agreement on July 31, 2025. [Pgs. 1-2][Pgs. 1-2]

Similarly, in July 2025, the owner of a property in Noblesville, Indiana, filed a complaint against Lite Magnesium Products seeking $500,000 of unpaid rent. [Pgs. 1, 4]

We find it unlikely that Lite Magnesium, which has a single U.S. employee, a website of stock photos, and which seemingly cannot afford its lease payments, is an established manufacturer for the aerospace industry.

In October 2024, Jeldi Acquired Certain Assets From An Ohio Foundry With Seller Financing, But Allegedly Stopped Making Payments To The Seller And The Foundry’s Landlord Shortly After The Deal Closed, And Both Parties Are Now Suing Him

Despite This Ongoing Litigation And His Failure To Pay For The Business, He Has Characterized The Acquisition As A Highly Successful Turnaround Story

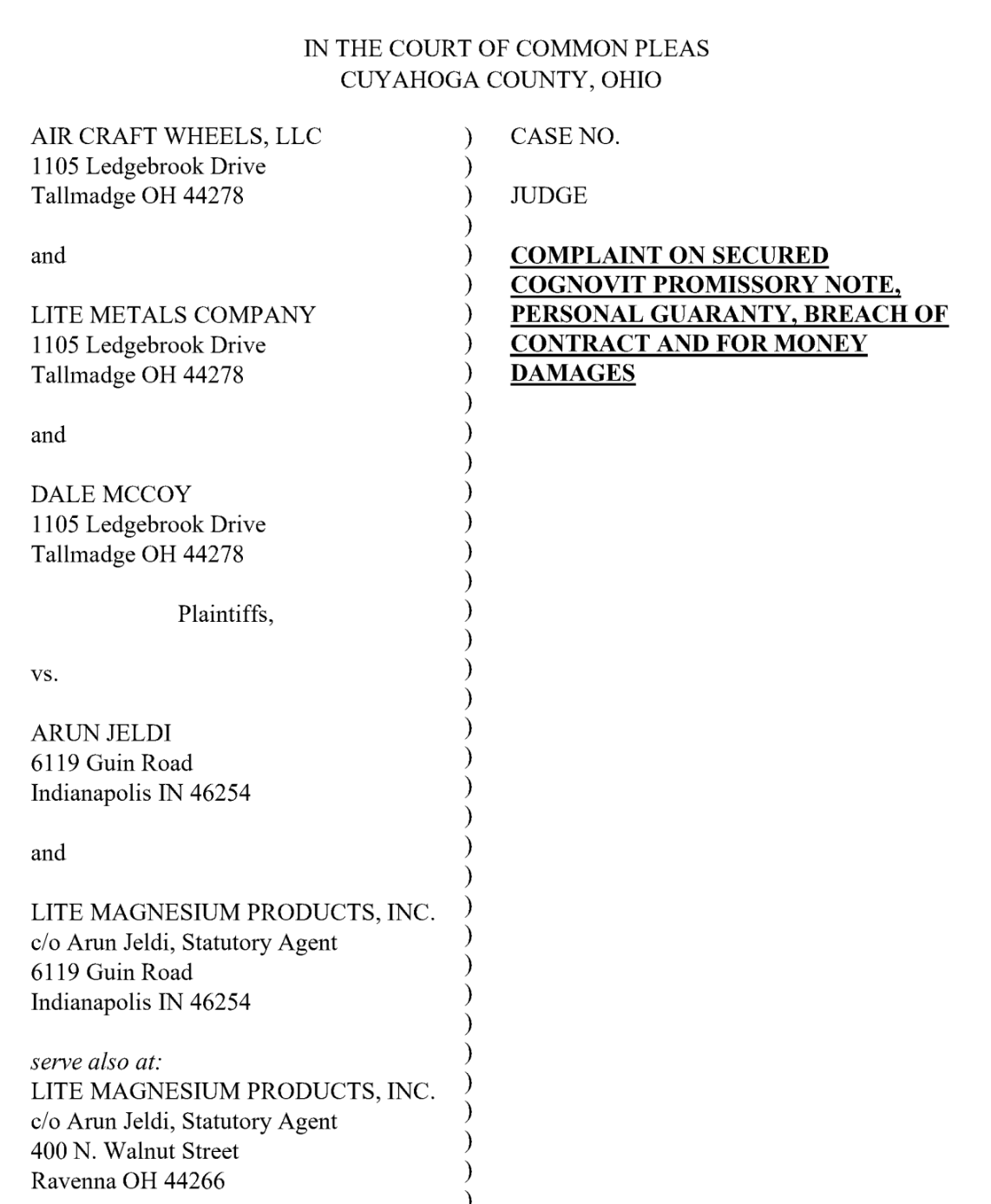

In October 2024, just two months before acquiring Velo3D, Arun Jeldi entered into an agreement to acquire certain assets of two Ohio-based manufacturing businesses, Lite Metals and Air Craft Wheels, through his entity Lite Magnesium Products. [Pg. 4]

In March 2026, the seller of the Ohio business filed a lawsuit against Jeldi in Ohio courts, alleging that Jeldi failed to make payments under the seller financing agreement. [Pgs. 5-6]

The deal also required that Jeldi enter into 2-year lease agreements with the landlords of the facilities where the acquired businesses operated.[1]

The first lease-to-purchase agreement was for a property located in Ravenna, Ohio, with a monthly rent base of $13,000 and a purchase price of $800,000 after one year. Lite Magnesium Products did not make “any rent payment,” according to the complaint. (Pgs. 6-7) The second lease-to-purchase agreement was for a property located in Avon, Ohio, with a monthly rent base of $7,000 and a purchase price of $800,000 after one year. Lite Magnesium Products did not make “any rent payment,” according to the complaint. (Pgs. 7-8) ↩︎

According to the complaint, however, he also breached those lease agreements. [Pgs. 4-8]

Despite failing to pay for the acquisitions and breaching the leases for both facilities, Arun Jeldi has framed this acquisition as a major success. In a September 2025 interview, when he was already nearly ~8 months delinquent on payments, he claimed that he acquired and successfully turned around an Ohio-based manufacturing business.

Jeldi’s Manufacturing “Experience” Appears To Have Its Origins In His Association With His Brother, Bala Jeldi, Who Has Faced 8 Civil And Criminal Cases In India And Reportedly Tried To Flee The Country After Defrauding Investors

A Former Associate Of Bala’s Told Us He “Essentially Defrauded Investors”

In 2019, Velo CEO Arun Jeldi incorporated at least two entities alongside an individual named Bala Jeldi whose LinkedIn profile shows an Indiana residence and an affiliation with magnesium manufacturing companies and 3D printing.[1]

In January 2019, Arun Jeldi incorporated Lite Auto Inc with “Bala Jeldi” serving as Chairman. In August 2019, arun Jeldi incorporated Lite Magnesium Products Inc with Bala Jeldi serving as its Chairman. ↩︎

In 2023, Arun and Bala Jeldi were photographed at a conference together.

While conducting our investigation into Arun Jeldi’s background, we asked a former Velo3D employee about the relationship between Arun and Bala, who confirmed that the two are brothers and that Bala had a magnesium foundry in India.[1]

Arun Jeldi’s address used in his 2006 certification of physical therapy educational requirements with the Michigan Board of Physical Therapy was: Plot #160, Road #4, Dhanalaxmi Coloni, Mahindra Hills. (Pg. 2) This is the same address used by Bala A Jeldi when he incorporated an entity in India in 2011. (Pg. 13) We see this as further confirmation of their affiliation. ↩︎

“I can understand your difficulty in finding information. When we first started talking to [Arun], I was honestly kind of sketched out by the whole conversation. And so, spent a lot of time digging and trying to figure out, like, where this guy came from, who he was, what was going on. So, I can tell you what I found out. When he was in India, he worked with his brother, [Bala], who also lives in Indianapolis currently. And they worked at a magnesium foundry in India. And they, it, wasn't working out and he became a physical therapist.”

We believe that magnesium foundry was Hindustan Magnesium, per Bala’s LinkedIn profile. In April 2022, Hindustan Magnesium entered an insolvency liquidation. After the insolvency proceeding, creditors received less than 5% of admitted claims, according to the insolvency resolution plan. [Pg. 8]

Both Bala and Hindustan have faced numerous civil and criminal cases in India since 2010, several of which remain open. See Appendix A at the bottom of this report for further details on these cases.

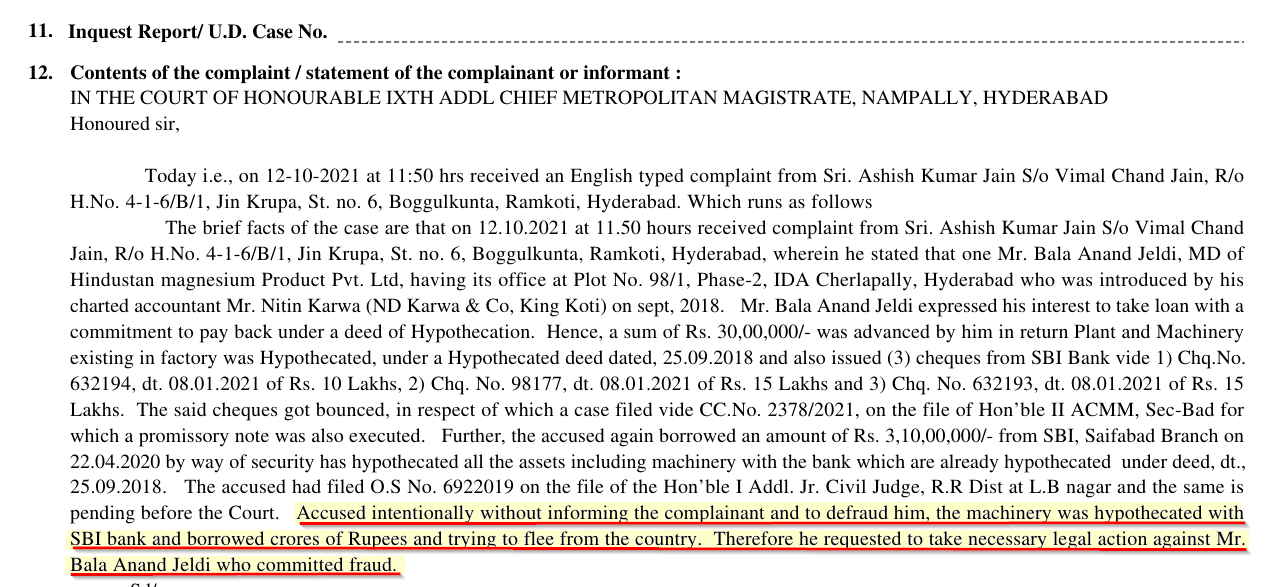

For example, we found a police report stating a complaint against Bala Jeldi for fraud. The complaint alleges that Bala Jeldi double pledged machinery, which meant the creditor was unable to collect their dues, and that he tried to “flee from the country.”

We spoke with a former associate of Bala Jeldi’s, who told us that Bala “essentially defrauded investors,” of multiple of his businesses, causing investors to “come after him.”

“And so, what is public is, if you look up in India, and it's related to, I think it's Hindustan Magnesium, out of India … that particular one, there is a note in, from the judge in one of those that specifically stated that Bala had fled the country prior to being criminally prosecuted… if you search through India, what you will find is that Bala has had a number of cases against him.”

While Bala does not appear to have any role at Velo3D, we find his and Arun Jeldi’s respective track records and his association in the industry are concerning and believe that Arun’s history warrants additional scrutiny from shareholders.

Conclusion

We believe it’s only a matter of time before investors see Velo3D for what it is: an obvious promotional grift orchestrated by a CEO with a wildly exaggerated resume that appears to be almost completely fabricated, a track record of business blow-ups and litigation, and no experience running a public company.

We believe that Velo’s relationship with SpaceX is virtually dead. Penetration into the aerospace and defense sector appears to be vastly overstated, consisting of little more than misleading promotion. Meanwhile, Velo’s own former employees have little faith that the RPS pivot will save the business, citing unreliable and inferior printers and intensifying competition.

Appendix A — Legal Cases Where Bala Jeldi Was Named As A Defendant In India

Since at least 2010, Bala Jeldi faced several criminal complaints in India, some of which remain open today:

- In March 2010, Fulletran India Credit Company Ltd. filed a criminal complaint against Bala Jeldi in Telangana. This case was disposed of in May 2012, though available records do not indicate its outcome.

- In January 2014, someone named Koinda Siva Reddy filed a criminal complaint against Bala Jeldi in Andhra Pradesh. This case was disposed of in October 2014, though available records do not indicate its outcome.

- In February 2020, Ps Kushaiguda filed a criminal complaint against Bala Jeldi in Telangana. These charges were disposed of by the end of 2020 pursuant to an agreement between Bala Jeldi and the complainant, Amit Tangri.

- In May 2021, a creditor named Ashish Jain filed a criminal complaint against Hindustan Magnesium Products, represented by Bala Jeldi. This case remains open in Telangana today.

- In July 2021, another creditor named Kondula Venkata Ratna Prasad filed a criminal complaint against Hindustan Magnesium Products and Bala Jeldi. This case remains open in Andhra Pradesh today.

- In January 2022, a criminal complaint was filed against Bala Jeldi in Telangana, and this case remains open today.

Some of the cases were categorized as “Indian Penal Code - 420” which implies “cheating and dishonestly inducing delivery of property,” per the Indian Penal Code. [1, 2]

Disclosure: We Are Short Shares of Velo3D, Inc. (NASDAQ: VELO)

Legal Disclaimer

Use of Morpheus Research LLC’s (“Morpheus Research”) research is at your own risk. In no event should Morpheus Research or any affiliated party be liable for any direct or indirect trading losses caused by any information in this report. You further agree to do your own research and due diligence, consult your own financial, legal, and tax advisors before making any investment decision with respect to transacting in any securities covered herein. You should assume that as of the publication date of any short-biased report or letter, Morpheus Research (possibly along with or through our members, partners, affiliates, employees, and/or consultants) will have a position in the stock, bonds, derivatives, or securities covered herein and, therefore, stands to realize significant gains if the price of the securities move. Morpheus Research also frequently enters into arrangement with capital providers pursuant to which those capital providers establish positions in a target company. Morpheus does not make any recommendations to, or control or otherwise influence trading by, such capital providers. Following publication of any report or letter, Morpheus Research intends to continue transacting in the securities covered therein and may be long, short, or neutral at any time thereafter regardless of Morpheus Research’s initial position or views. Morpheus Research’s investments are subject to its risk management guidance, which may result in the de-risking of some or all its positions at any time following publication of any report or letter depending on security-specific, market or other relevant conditions. You should assume that as of the time you read this report, Morpheus Research has covered or closed some or all of its initial positions at the time of publication. This is neither an offer to sell or a solicitation of an offer to buy any security, nor shall any security be offered or sold to any person, in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction. Morpheus Research is neither registered as an investment advisor in the United States, nor does it have similar registration in any other jurisdiction. To the best of Morpheus Research’s ability and belief, all information contained herein is accurate and reliable and has been obtained from public sources believed to be accurate and reliable, and who are not insiders or connected persons of the stock covered herein or who may otherwise owe any fiduciary duty or duty of confidentiality to the issuer. Conclusions expressed herein are based upon the information disclosed herein and represent the opinion of Morpheus Research. Such information is presented “as is,” without warranty of any kind – whether express or implied. This report was prepared independently, without coordination with any third party. Morpheus Research makes no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results to be obtained from its use. All expressions of opinion are subject to change without notice, and Morpheus Research does not undertake to update or supplement this report or any of the information contained herein.