Figure Technology: Smoke And Mirrors From A Fast-And-Loose Lender Masquerading As A Blockchain Darling

Summary

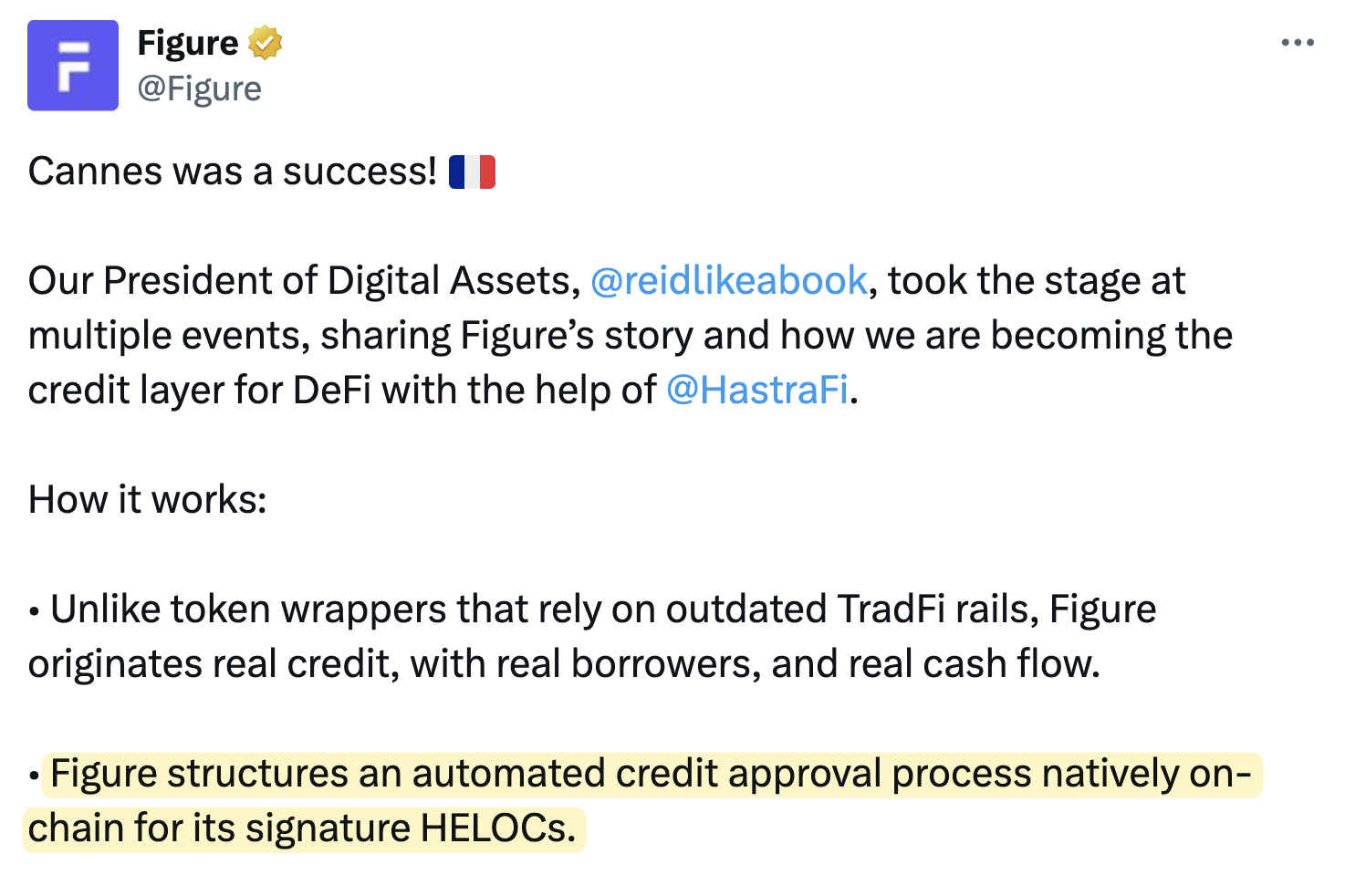

- Figure Technology Solutions, Inc. (NASDAQ: FIGR) is a $7.7 billion fintech company that claims to use blockchain to improve the speed, security, and cost of originating and securitizing home equity lines of credit (“HELOCs”). Beyond this initial market, Figure has developed a suite of blockchain tech that, according to the grandiose claims of co-founder Mike Cagney, will secure Figure’s place in the “Mag 7” of “Web 3.0.”

- Our 4-month investigation reveals that Figure is little more than a risky home equity lender masquerading as a blockchain innovator. Its blockchain initiatives, including Figure Connect, Democratized Prime, YLDS, OPEN, and Figure Markets appear to have stalled or are propped up by Figure itself. The company’s closely affiliated “Provenance Blockchain” bears hallmarks of centralization antithetical to the DeFi movement.

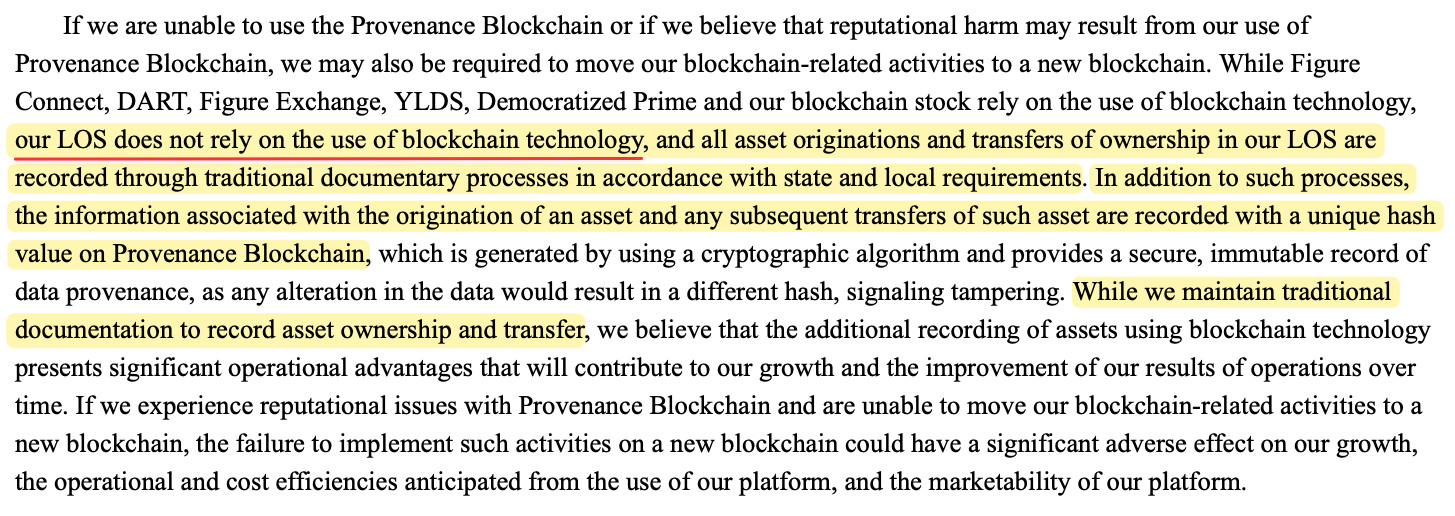

- Figure does not originate loans on the blockchain, per its own SEC disclosures and our interviews with former employees. Instead, its HELOC business largely boils down to an undifferentiated origination model built on widely available 3rd-party tools used by many competing lenders. Its growth has been fueled by aggressive underwriting that appears to prioritize volume and speed over quality, leaving Figure susceptible to fraud, severe valuation discrepancies and adverse borrower characteristics, harkening back to the disastrous practices that preceded the 2008 Financial Crisis.

- Figure’s misrepresentations seem to be an open secret among its own employees, with one former employee telling us: “They love that moniker of being a sort of blockchain-based entity” and another saying: “Prior to joining Figure, I was convinced that everything was happening on-chain, like beginning to end. And that's not the reality, right?” A third told us that the “Mike Cagney playbook” is selling investors a “vision of a Porsche when all we have is like a bicycle.”

- Cagney has a controversial history of misleading stakeholders, “grandiose claims,” hyperbole, and an appetite for using “opaque structures” reminiscent of the worst practices that led to the 2008 Financial Crisis, according to multiple media reports on his tenure at SoFi, a company he co-founded. Moreover, Figure’s CFO was allegedly “instrumental in orchestrating” a billion-dollar Ponzi-like scheme built on a “foundation of lies,” a position omitted from her bio.

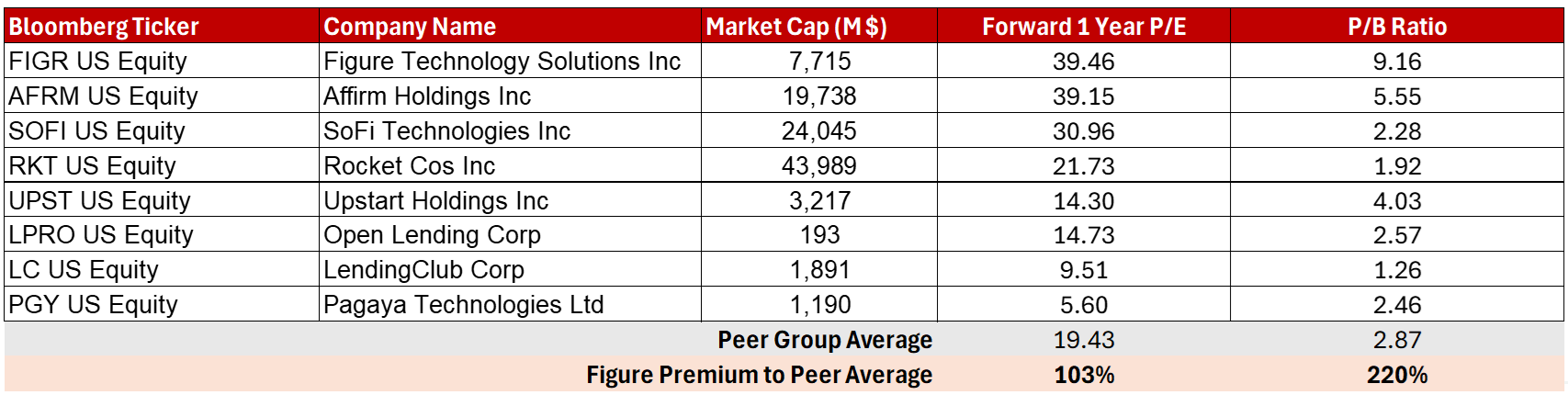

- Despite claiming that $30 is a “goofy” price and indicating that he may single-handedly “push up the bid price” of Figure’s shares, Cagney has dumped $64 million worth of stock since IPO at an average price of $28.50 without a single purchase. This is in addition to significant sales from other insiders, all while Figure trades at a 103% “blockchain premium” to fintech peers. Cagney also appears to have an undisclosed pledge of 2 million shares, per an active UCC filing.

From Loan Origination To Securitization: We Believe Figure Exaggerates Or Outright Fabricates Its “Significant Blockchain-Enabled” Advantages

- Figure has repeatedly claimed that it originates all of its loans on the blockchain, which allegedly drives significant cost savings, while reducing the time it takes to fund a loan. Yet, Figure does not originate its loans on the blockchain. Buried within its SEC filings, Figure admits that the company’s Loan Origination System (“LOS”) “does not rely on the use of blockchain technology” and that “all asset originations and transfers of ownership in our LOS are recorded through traditional documentary processes.”

- Rather than being powered by blockchain tech, Figure’s supposedly “proprietary” LOS is a patchwork of off-the-shelf tools that are used by numerous other digital HELOC lenders. These include vendors such as CoreLogic for digital property valuations and lien checks, Plaid for automated income verification, and other service providers that are ubiquitous across home equity lending.

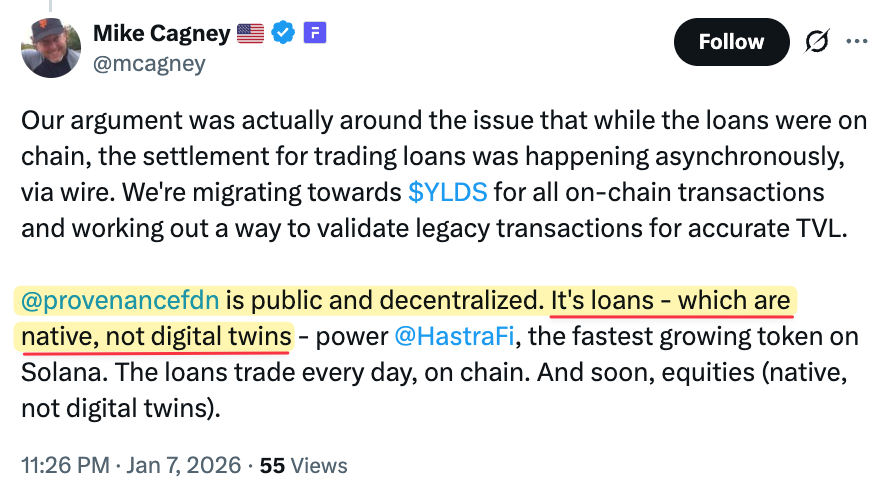

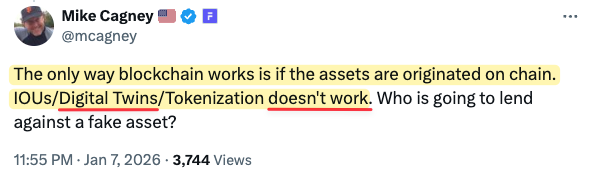

- Despite clear disclosures that Figure’s LOS does not rely on blockchain, Cagney continues to tell investors that its loans are “native” to the blockchain and that they are not “digital twins,” which are blockchain tokens that represent real world assets. He has publicly ridiculed the use of tokens and digital twins. For example, Cagney posted on X in January that the “only way blockchain works” is if assets are “originated on chain” and that “digital twins/tokenization doesn’t work,” implying that tokens are “fake assets.”

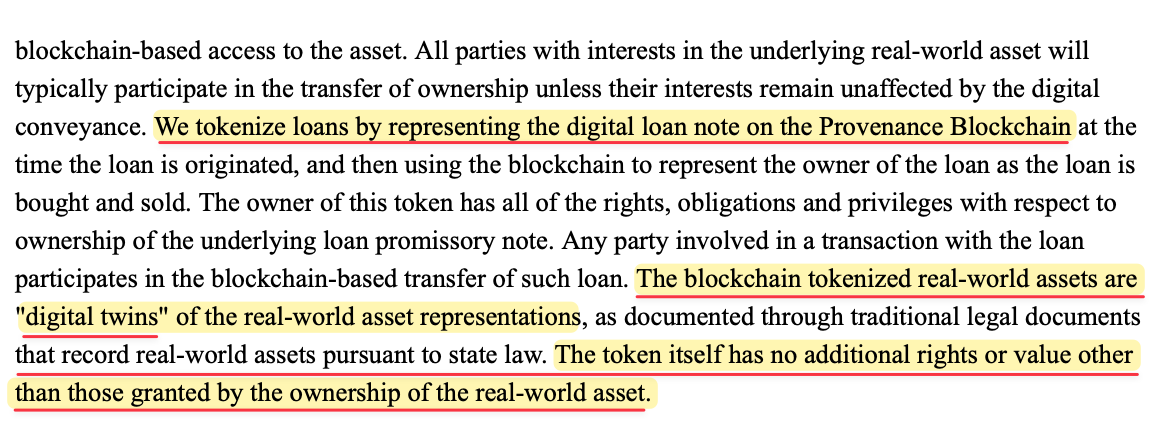

- Contradicting Cagney’s statements, Figure’s SEC filings explicitly state that its loans are “digital twins,” or “tokenized” representations of real-world assets “as documented through traditional legal documents.” In other words, Figure originates its loans through conventional means and then uploads the loan data to the blockchain only after-the-fact.

- In September 2025, Mike Cagney engaged in a Twitter feud with a crypto data aggregator DefiLlama, which has been described as “one of the few honest actors” in the crypto space. DefiLlama refused to list Figure’s loan assets in its reporting after conducting due diligence on Figure claims and citing the unanswered question of whether Figure was just “mirroring their own internal [database] into the chain,” while accusing Figure of wanting to “pump their metrics for their IPO.”

- One of Figure’s repeatedly claimed efficiencies of the blockchain is related to the practice of emailing spreadsheets with loan data back-and-forth between capital markets counterparties – a practice Figure executives have characterized as “crazy,” archaic and susceptible to fraud. Instead, Figure claims that by storing loan data “immutably” on the blockchain, it makes a “Tricolor-style failure impossible,” referring to the recent collapse of the sub-prime lender that manipulated spreadsheets with loan data.

- Despite Figure management’s stance against the use of spreadsheets, Figure uses them to share loan data with counterparties. Figure sent audit-firm KPMG loan data spreadsheets with labels like “v5,” “v7,” “v3 (6)” and “External,” indicating manual compiling, editing and sharing, according to reports issued by the audit firm. Similarly, a former employee confirmed that the company sent most of its loan tapes via email and spreadsheet to loan buyers: “Yep. Again, maybe that’s changed, but I doubt … that’s how a lot of the funds and how the banks do things.”

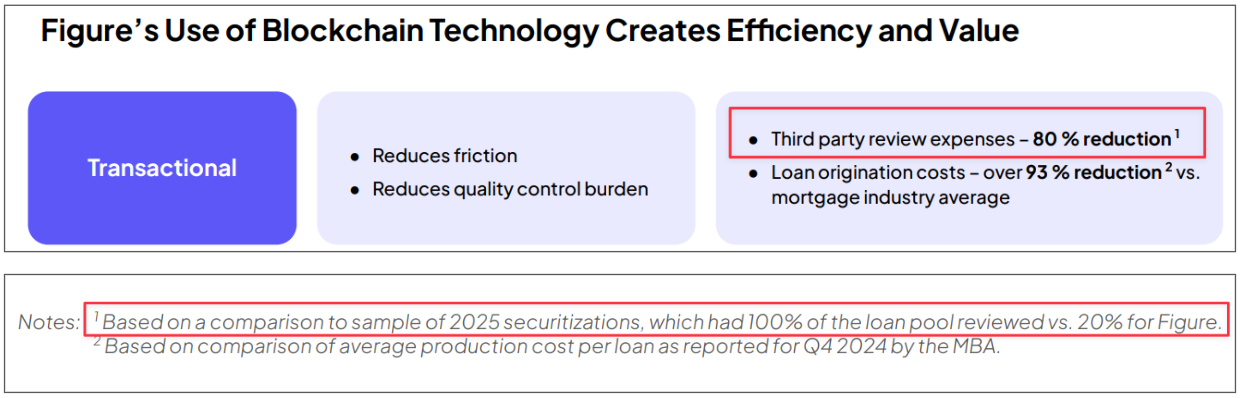

- Mike Cagney also claims that “because of the way we use blockchain,” auditors for its securitizations only need to review 20% of the loan pool, which Figure’s CEO has said is “one of the clearest examples of blockchain adding value.”

- This, too, is an egregious misrepresentation of Figure’s claimed blockchain-enabled advantages. In reality, post-2008 regulations require that a “statistically significant” percentage of a loan pool be audited, which in many cases could be ~20%. Other HELOC lenders, like Achieve, also report ~20% of loan pools being audited in securitization reports, despite not using “immutable” blockchain-hosted loan data.

- An employee from Achieve told us: “It is not the blockchain that’s allowing them [Figure] to do 20%, not 100% … it’s the requirements of the rating agencies as well as the underwriters … one of the underwriters that we work with, one of the same ones that they work with, requires 20%.”

Figure Is A Graveyard Of Failed, Flailing, And Internally Propped-Up Blockchain Projects Including Figure Markets, Figure Connect, And Democratized Prime

- Figure has a history of promoting supposedly breakthrough blockchain projects that either stalled entirely or failed to gain significant traction, like Figure Equity Solutions, Figure Pay and Figure Markets.

- Its latest initiative, Figure Connect, is a “capital-light marketplace” of whole loans that the company “does not even touch,” and that accounts for more than 50% of total origination volume. Contrary to these claims, our investigation reveals that Figure appears to be a significant buyer in the Figure Connect marketplace.

- For the first 9 months since Figure Connect was launched, only 53.5% of Figure Connect volume was transacted by 3rd-parties, according to the company’s first S-1 filed with the SEC. Figure does not disclose how much of the 2025 Figure Connect volume was supported by its own purchases.

- A footnote in Figure’s latest prospectus indicates that the volume transacted in its marketplace includes “loans contributed directly to securitizations.” This indicates that Figure buys the loans through Figure Connect as a principal and then acts as the seller “of all HELOCs” that make up the loan pools securitized, based on the pre-sale reports from DBRS Morningstar.

- Regarding Figure Connect, a former Figure employee told us, “The vision was to have this marketplace and make it very easy for institutional investors to buy loans. Back when I was there, Figure was funding a lot of it, like a lot of it.”

- Institutional investors seem to be walking away from the platform. For example, in February 2025, Figure announced a JV with investment firm Sixth Street to “bring over $2 billion of liquidity” to Figure Connect. Yet, fast forward to the end of 2025, and Sixth Street has contributed less than 25% of its commitment, and the JV appears to have not purchased a single loan, per SEC filings. The JV agreement had an initial term through February 2026, although Figure has not updated investors on its renewal or provided any update.

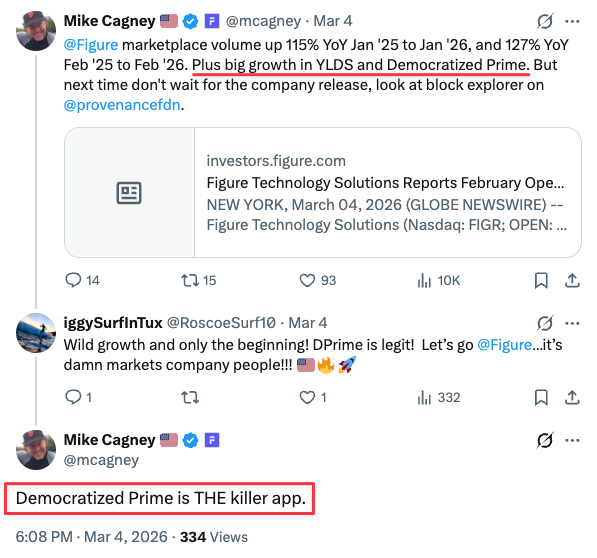

- In June 2025, Figure launched a DeFi initiative called “Democratized Prime,” described by Mike Cagney as “THE killer app” that would provide superior interest rates to both borrowers and lenders. Yet, Figure appears to be paying above market rates of ~8.7% to attract lenders to the platform, while its undrawn traditional warehouse lines cost just ~5.5%, according to its financial statements. After 10 months, Prime has little traction with other borrowers, with Figure’s own HELOC pools representing 94% of the demand for capital

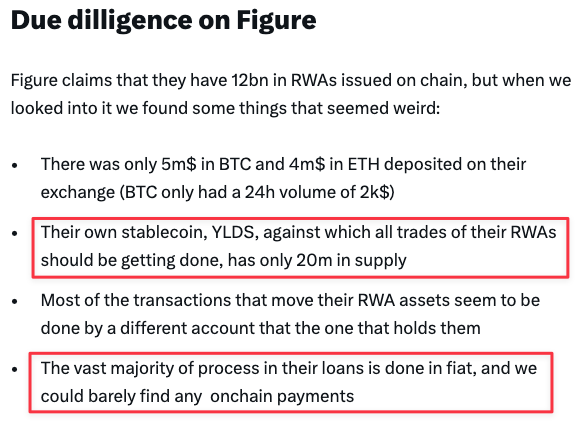

- Figure has launched a yield-bearing stablecoin called YLDS that Figure’s CEO has described as the “oil of our capital market,” which is used to settle loans traded on its marketplace. We struggle to understand how this could be possible when at the end of 2025, 99% of YLDS was owned by Figure and a single passive investor.

- In yet another promotional initiative, in early 2026, Figure introduced OPEN, an exchange for listing equity natively on the blockchain, and listed 4.375 million of its own shares. Mike Cagney said it was the “beginning of the true renaissance era of blockchain.” Yet, just 2 months after listing Figure shares on OPEN, 86% of shares have left the network, while trading volume has plummeted to less than $60,000 per day and no other listings have materialized.

Figure’s Real Growth Drivers: Questionable Interpretation Of Regulations & Fast And Loose Lending Practices That Are Driving Accelerating Delinquencies

- Figure’s HELOC lending practices are reminiscent of the fast and loose underwriting standards that preceded the 2008 Financial Crisis – most aptly characterized by the aggressive prioritization of speed and volume over quality. This includes lending against investment properties, the use of unreliable automated valuation models (“AVMs”), not ordering title reports or requiring title insurance, a lack of proper diligence on existing liens, the use of the more forgiving alternative credit scores, and more.

- A former employee described some of these as a “major flaw” in underwriting that creates “really high-risk exposure” and which opens a “wide door for fraud.” In a key example, the former employee explained that, in their view, Figure’s AVMs were not always accurate, “I can tell you, there were some major issues there. And it really gives you a true understanding of value and AVM, and even with a high confidence score, I saw many times where those were not appropriately positioned.”

- In another key example, the former employee explained that Figure’s lien checks are not always sufficient, “I liked being at Figure, but I have now gone to [redacted] because of some of my concerns. One of the other major flaws, in my opinion here, is that you do not ever have a title report before you make a $150,000 - $200,000 loan and you don’t have a title policy … presumably we’re buying a first-lien loan at max 85% LTV, well come to find out … we weren’t actually first position.”

- Cracks in Figure’s loan performance are already starting to show, with delinquent balances of loans held for sale increasing from 3.91% in 2024 to 5.46% in 2025, according to Figure’s financial statements. During the same period, BofA, the largest HELOC lender in the US, experienced a reduction in outstanding home equity loan delinquencies and non-performing from 1.92% to 1.78%.

- Our analysis of over a dozen 2024-vintage securitization deals reveals that 90+ day delinquencies in Figure’s loan pools are twice as high as delinquencies in similar loan pools including home equity loans from Rocket Mortgage and Spring EQ.

- Figure’s partners also appear to corroborate Figure’s loose underwriting. Namely, one of Figure’s highest-volume partners has publicly bragged publicly about how “easy” it is to sell a Figure HELOC, saying there is a “very high chance” of approval with “no appraisal needed, no actual income docs needed … it’s easy.”

- Figure classifies its loans as “Open-End” credit for the purposes of federal regulations, which requires a “contemplation” that borrowers will do repeated draws on their credit facility. A former Figure employee explained there was scrutiny on this due to Figure’s requirements that borrowers fully draw their HELOCs at close, “There’s a lot of scrutiny, I mean a lot of scrutiny around that … I know we’re calling it an open-end product, but at that point, until they pay it down, it’s closed, I mean that’s almost a closed-end product there.”

- Figure’s forced “full draw” at origination has also sparked consumer backlash, resulting in complaints with the Consumer Financial Protection Bureau (CPFB), according to a class action lawsuit and negative reviews accusing the company of false advertising.

Figure’s Closely Affiliated “Provenance Blockchain” Is Neither Independent Nor Decentralized

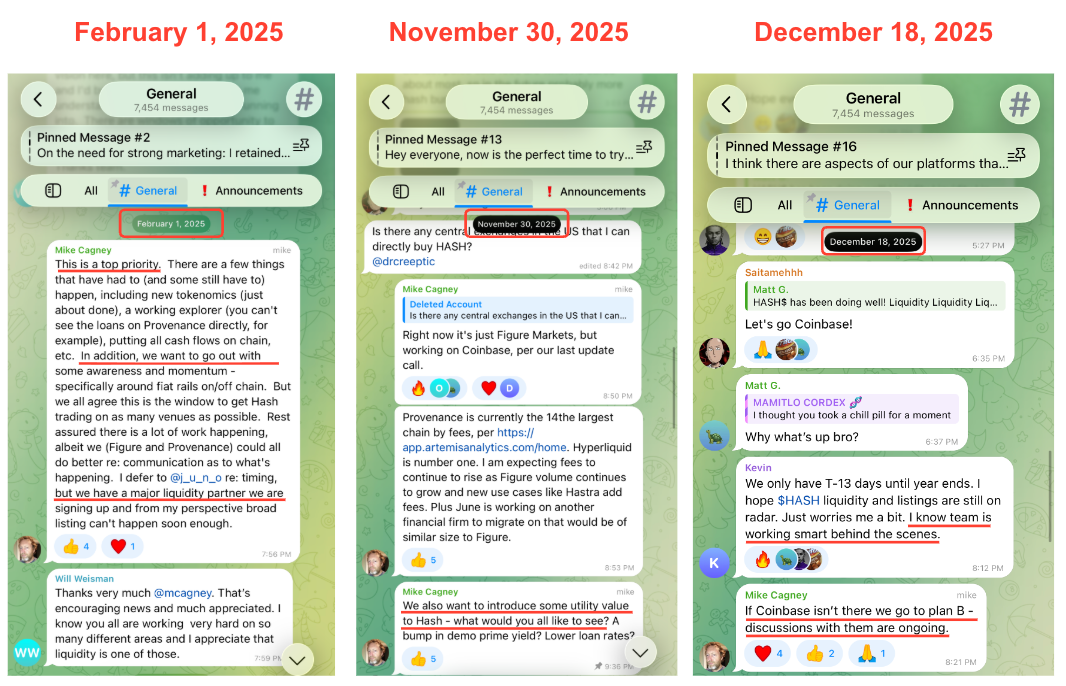

- In 2022, Cagney said in an interview, “If you don’t have the decentralization, and you have someone who de facto controls the network, then you don’t really need the blockchain.” Despite that statement, our investigations found that Provenance Blockchain has all the hallmarks of a centralized network.

- Figure describes Provenance Blockchain as an “independent Layer 1 blockchain” and claims that it does not “participate or expect to participate in the development and maintenance of Provenance Blockchain.” Yet, Provenance Foundation is led by Mike Cagney’s wife, who is a co-founder and director of Figure. A review of the Provenance’s public Telegram channel further indicates that Cagney is the de facto leader of the Provenance community. Meanwhile, multiple senior executives from Figure simultaneously hold roles with the Provenance Foundation.

- Despite Figure’s CEO saying that they "absolutely don’t control the network,” over 65% of Provenance blockchain’s native and governance token is owned by Figure, affiliates of Figure, and Cagney himself, according to Telegram messages from Cagney.

- Provenance Blockchain is a proof-of-stake blockchain, in which nodes are operated by validators. Validators stake Provenance’s native and governance currency, HASH, in order to produce blocks and validate transactions. Owners of HASH can delegate their tokens to validators and receive fees generated by transactions in the network.

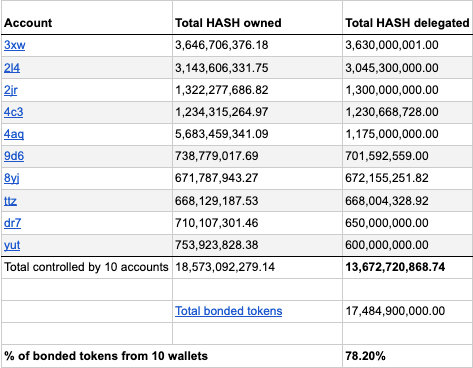

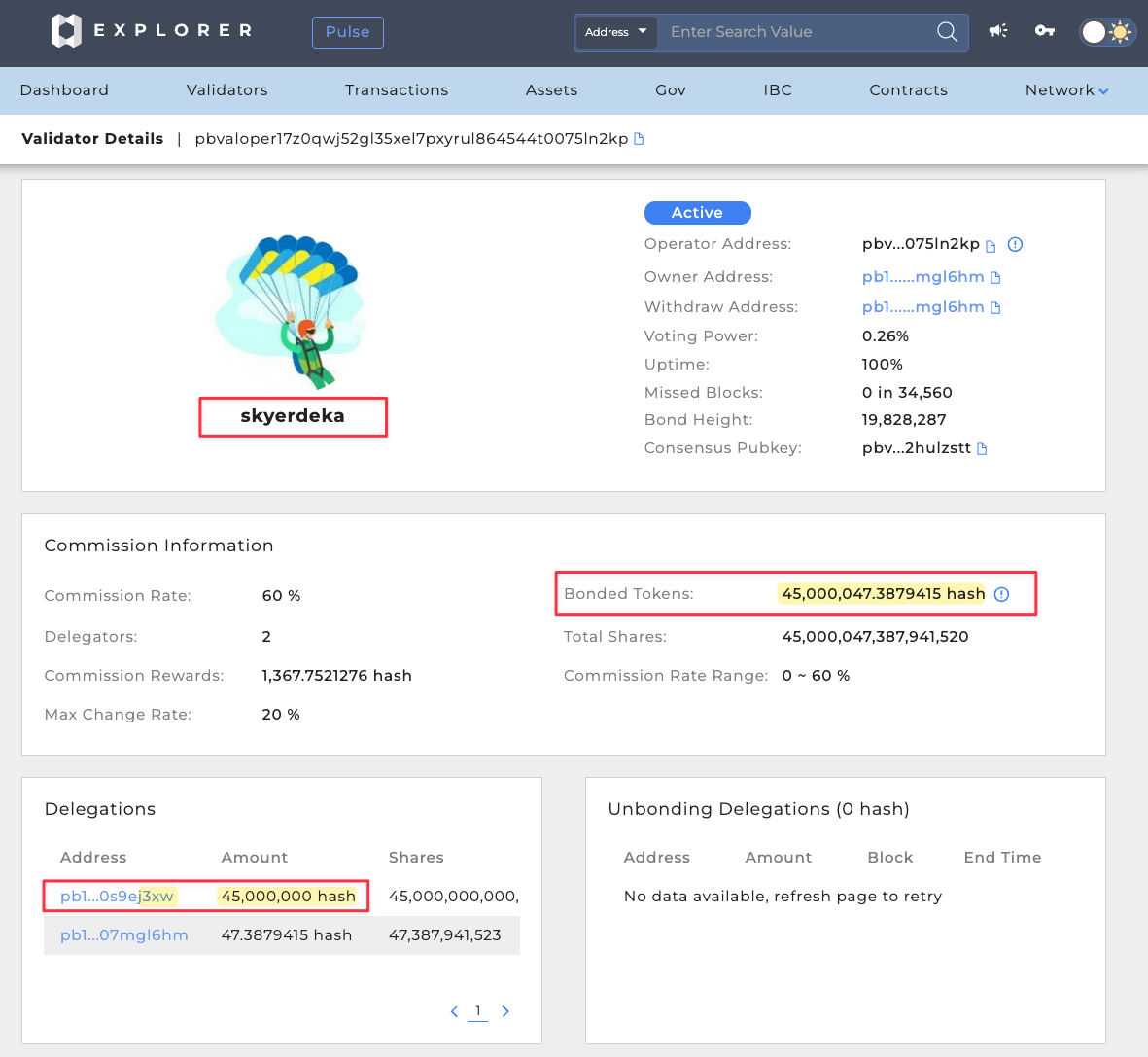

- According to our analysis of the Provenance Explorer, 10 accounts control 78% of all HASH tokens staked by all the validators. Based on that distribution, a mere 2 accounts could halt the entire network and only 7 accounts could collude to alter the registries of Provenance Blockchain, according to the documentation of the consensus mechanism used by Provenance.

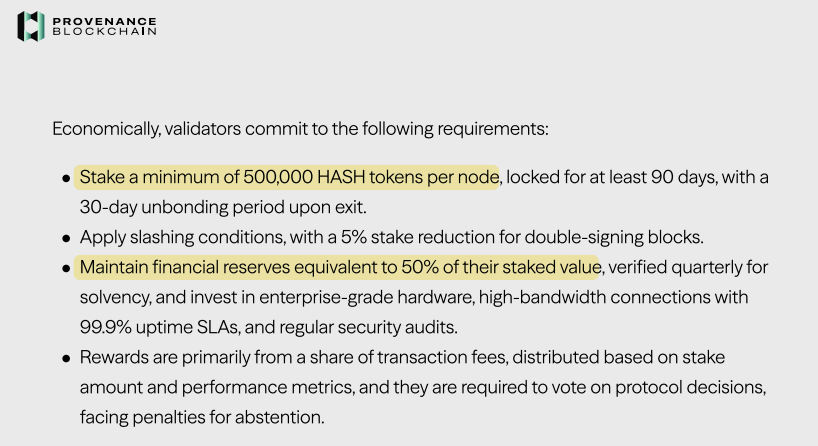

- Proof-of-stake networks typically require validators to have financial skin in the game to secure the network. We found that almost half of the validators active on Provenance received their staked tokens from the Provenance Foundation, rather than putting their own skin in the game— 40% of the active validators had, at best, an average of $23 in total assets at risk, according to our analysis of Provenance explorer.

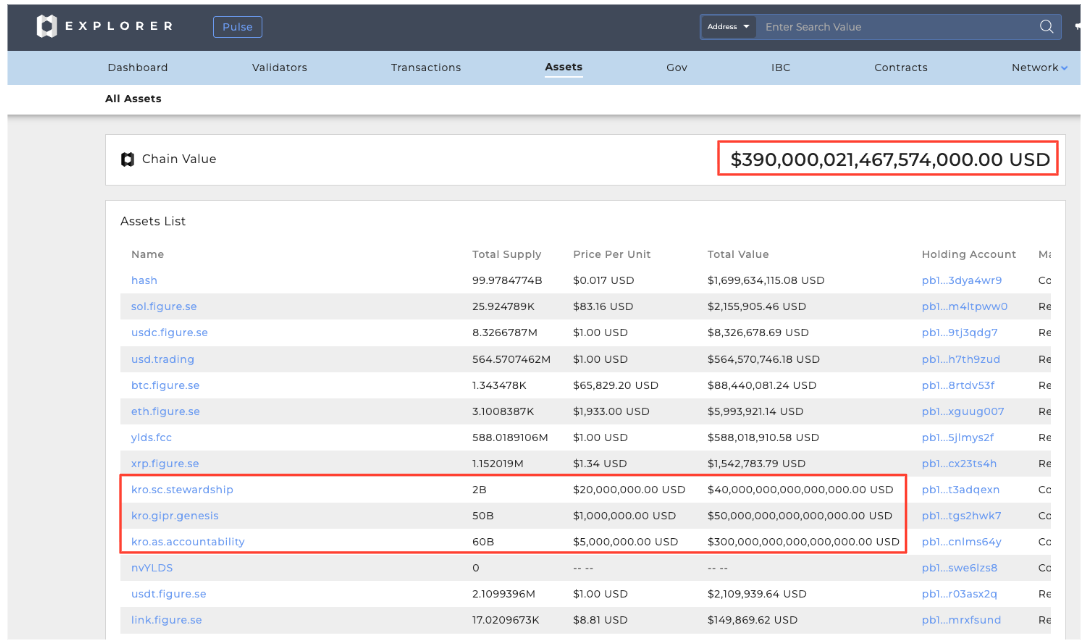

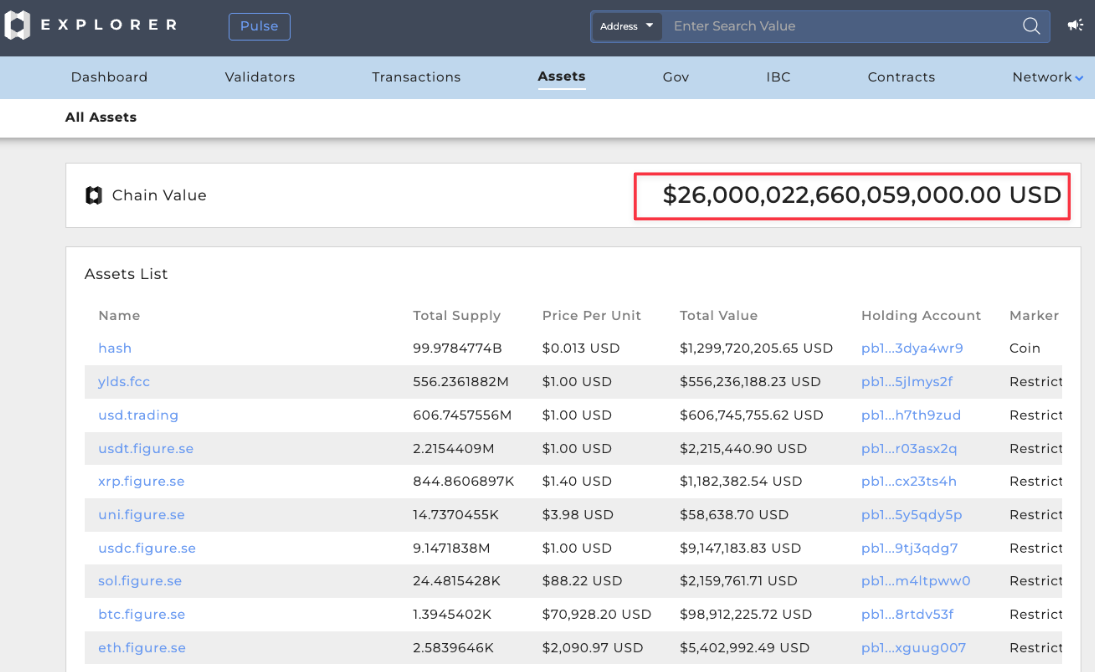

- We believe the problems with Provenance’s “independent” governance and the lack of security provided by its network of validators are exemplified by its printing of quadrillions of dollars of value out of thin air. In March 2025, Provenance displayed on-chain assets worth $390 quadrillion, per the Provenance explorer.

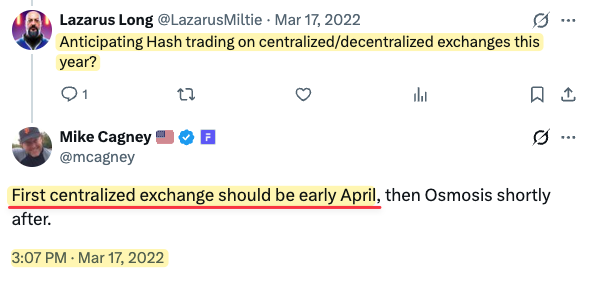

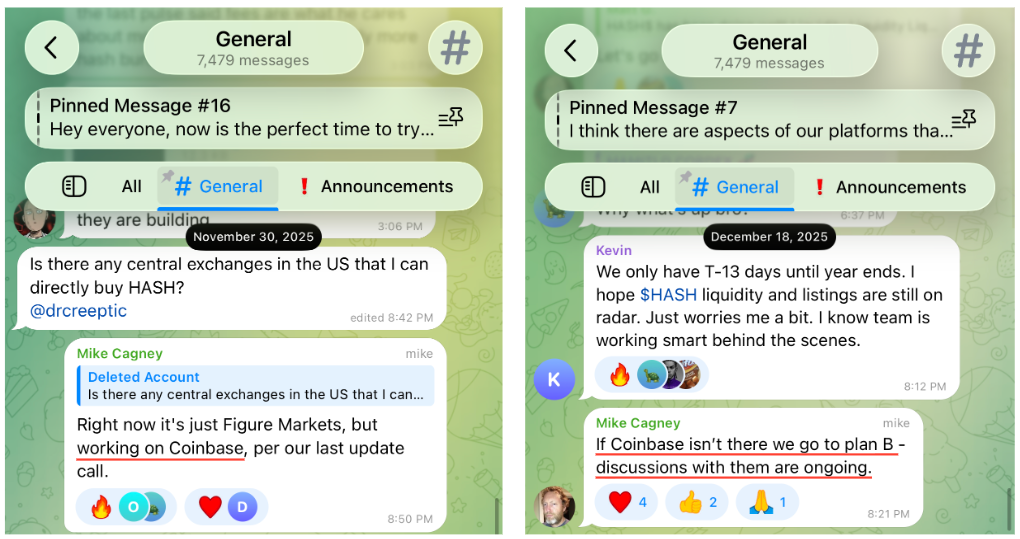

- Listing a crypto token on a recognized centralized exchange adds credibility to a crypto project. The bar to list a token, however, is not that high. For example, the “dumbest of all meme coins,” Fartcoin, is listed on Coinbase and Kraken. Despite years of assurances from Mike Cagney, HASH is still not listed on a major centralized exchange, and its price has plummeted by ~90% since launch.

Conclusion

- Like all great stock promotions, Figure’s claims fall apart under detailed scrutiny, which we believe is coming for its allegedly blockchain-themed “disruption.” We believe the market will soon re-rate Figure for what it is – an undifferentiated HELOC lender with aggressive underwriting facing hordes of competitors.

Initial Disclosure: After extensive research, we believe the evidence justifies a short position in shares of Figure Technologies Solutions Inc (NASDAQ: FIGR). Morpheus Research holds short positions in FIGR. This report represents our opinion, and we encourage all readers to do their own due diligence. Please see our full disclaimer at the bottom of the report.

Background: A $7.7 Billion FinTech Using Blockchain To Disrupt Capital Markets

Figure Technology Solutions, Inc., is a $7.7 billion financial technology company that claims to be “building the future of capital markets with blockchain.” It was founded in 2018 by current Chairman Mike Cagney who previously co-founded SoFi, where he served as CEO until 2017. Cagney’s wife, June Ou, also came from SoFi and is a co-founder and director of Figure.

Figure's purported use of blockchain technology relies on the affiliated and little-known Provenance Blockchain, which the company describes as an “independent layer 1 blockchain” that acts as the “database foundation” for Figure.[1]

Provenance Blockchain was built as part of Figure and was eventually spun off, according to a 2019 presentation from Mike Cagney. Provenance Blockchain, was built using Cosmos SDK, an open-source framework for building blockchains. Provenance Blockchain is currently overseen by the Provenance Foundation. Provenance’s native coin only trades on Figure’s own exchange and is not listed on any major exchange such as Coinbase or Kraken, per CoinGecko, indicating a lack of interest and demand in this blockchain. ↩︎

The initial target of Figure’s blockchain-powered disruption has been home equity lines of credit (HELOCs). Since its 2018 inception, Figure has grown into one of the largest providers of HELOCs in the country, originating billions of dollars of loans annually, both directly and through its 300+ member partner network.

Figure says blockchain reduces HELOC origination costs by 93%, securitization-related audit costs by 80%, and vastly improves speed and security as loans move from origination to capital markets.[1]

Bull Case: Continued HELOC Dominance While Poised To Disrupt Virtually All Capital Markets Through A Suite Of Proprietary Blockchain Tech As It Seeks To Join The Future “Mag 7” Of “Web 3.0”

With its use of blockchain technology, Figure has grown loan originations by ~74% since 2020, becoming the #1 non-bank HELOC lender in the country. With $34 trillion in outstanding home equity in the United States, bulls believe Figure has substantial room to continue growing in this core segment.[1]

With HELOCs, homeowners can tap into their home equity without affecting their existing low-rate first mortgages. ↩︎

Beyond HELOCs, Figure is developing a suite of blockchain-powered technology that ostensibly positions it to disrupt all capital markets.

- Figure Connect is a “first-of-its-kind blockchain-based” marketplace for private credit that Figure executives claim is “capital light,” reducing balance sheet risk while capturing high-margin ecosystem fees from loans transacted on the platform.

- Figure Markets is a blockchain-native exchange that Cagney has described as an “exchange of everything” that has the potential to facilitate trading of crypto, stocks, and alternative investments.

- Democratized Prime is a DeFi lending platform that Cagney has described as “THE killer app” that will compete directly with banks for capital, effectively cutting out the middleman and allowing lenders to earn more while borrowers access cheaper capital.

Through those supposedly groundbreaking initiatives, among others such as OPEN and Figure Forge, investors believe that Figure is positioned to capitalize on a “trillion dollar” opportunity and cement its position in what Mike Cagney describes as the “Mag 7” of “Web 3.0.”

Fundamentals: Up 42% From Its September 2025 IPO Price, Figure Now Trades At An Exorbitant 103% Premium To Peers As Competition In Its Core HELOC Market Rapidly Intensifies

Despite Figure’s array of seemingly impressive blockchain initiatives, today “substantially all” of Figure’s revenue still comes from its HELOC business, yet the company trades at an exorbitant valuation compared to fintech peers, most of which have diversified revenue sources.

With its shares trading 42% higher than its September 2025 IPO price, Figure trades at a 103% premium to peers based on forward earnings estimates and a 220% premium based on its trailing price-to-book ratio.[1]

Calculated based on consensus 1-year forward price to earnings multiple, per Bloomberg. ↩︎

Even ignoring our findings entirely, we believe Figure’s valuation and the intensifying competitive environment present fundamental downside risk.

Over the last two years, fintech giants such as SoFi and Rocket have aggressively expanded into home equity lending, growing origination volumes by 570% and 73.6% YoY, respectively. Meanwhile, a wave of smaller digital HELOC lenders such as Achieve and Homebridge are also reporting strong growth of 91% and 160% YoY, per a report from data aggregator Inside Mortgage Finance.

Part 1 - From Loan Origination To Securitization: We Believe Figure Exaggerates Or Outright Fabricates Its “Significant Blockchain-Enabled” Advantages

Figure claims a host of blockchain-enabled advantages spanning from origination to securitization. Many of Figure’s claims appear greatly exaggerated or outright fabricated, according to its own disclosures, our interviews with former employees, and our analysis of its securitization reports. Our research indicates that blockchain provides little to no real benefit to Figure’s core HELOC business.

Figure Claims That All Of Its Loans Are “Originated Through The Blockchain,” Which It Claims Drives Significant Cost Savings While Vastly Reducing The Time It Takes To Fund A Loan

Reality Check: Figure’s Loans Are Not Originated On The Blockchain, Per Figure’s Own SEC Filings, Which State That Its Loan Origination System “Does Not Rely On The Use Of Blockchain Technology” And That “All Asset Originations” Are Recorded Through “Traditional Documentary Processes”

“Prior To Joining Figure, I Was Convinced That Everything Was Happening On Chain, Like Beginning To End, And That’s Not The Reality” - Former Figure Employee

Cagney and other Figure executives have repeatedly asserted that the company’s loans are originated on the blockchain, and Figure’s website states that the company uses “blockchain to deliver a new standard in financial efficiency: faster approvals, lower costs, and transparent access.”

“The average consumer doesn't see blockchain when they get a Figure loan. What they are getting is a faster process, a cheaper rate because of all the efficiencies blockchain afford us on the back end.” - Figure Chairman Cagney to CNBC in September 2025

“Every loan originated across our now almost 250 partners is done electronically end-to-end on the blockchain without human involvement in the data.” - Figure CEO, Mike Tannenbaum on the first public earnings call in November 2025

"All of our loans are originated through the blockchain and then passed on to the capital markets at the end of the day”- Figure CFO Macrina Kgil to The Street in November 2025.

“Figure uses blockchain to reduce the cost to originate, finance and sell mortgages. It costs less than $1K to originate a first lien HELOC on the Figure platform. That alone is a significant blockchain-enabled benefit.” — Figure Chairman Mike Cagney in a February 2026 post.

Yet, Figure’s own disclosures to regulators directly contradict those claims.

Buried within Figure’s SEC filings, the company states clearly that Figure’s loan origination system (“LOS”) “does not rely on the use of blockchain technology” and that “all asset originations and transfers of ownership in our LOS are recorded through traditional documentary processes.”

Rather than a “proprietary” origination process powered by the blockchain, Figure’s LOS appears to be a patchwork of off-the-shelf 3rd-party tools that are ubiquitous across the home equity lending industry. This includes Cotality for valuations and lien searches and Plaid for income verification.[1]

Figure’s automated property valuations and lien searches are not “proprietary” or powered by blockchain, but provided by vendors such as Clear Capital and Cotality (fka CoreLogic), according to pre-sale reports from Figure securitizations. (Pg. 31) Cotality’s CLIP provides every record for a property, including ownership history, liens and taxes. Figure has worked with Cotality since its inception, specifically using CLIP, according to a success story published by Cotality. These providers are confirmed by Figure’s trust center resource, which lists them as subprocessors: Plaid for “income verification,” ClearCapital for property valuation, and CoreLogic (aka Cotality) for “valuations and lien matching.” ↩︎

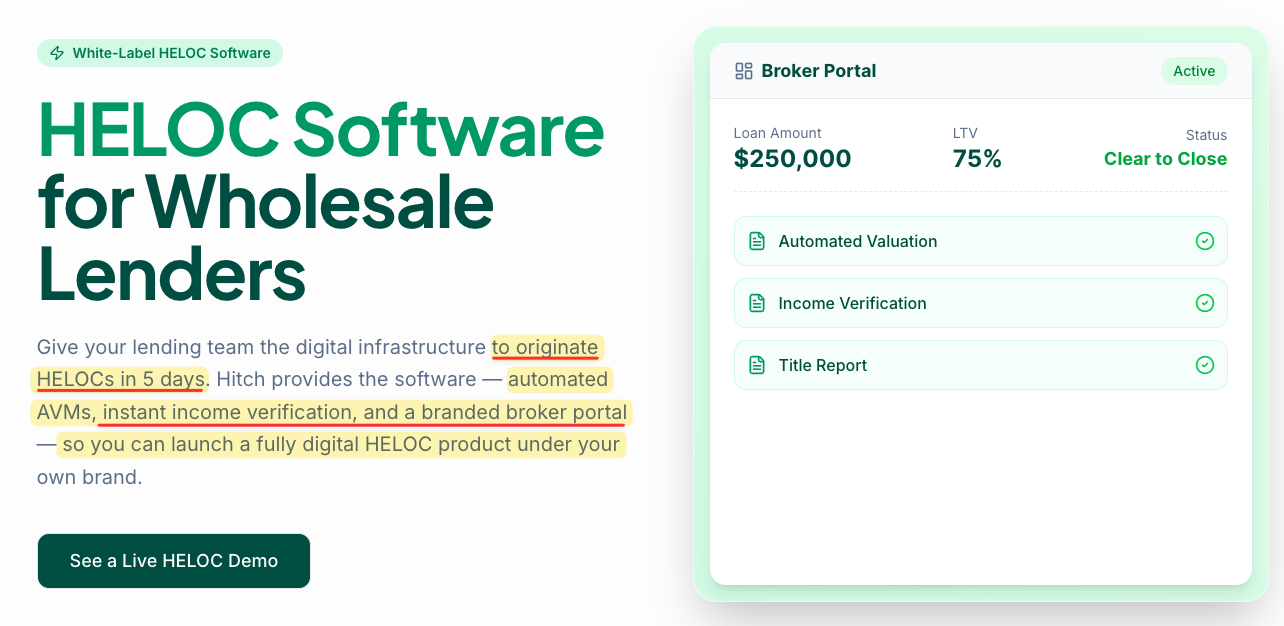

100% online applications, near-instant approvals, and access to funds in a matter of days are becoming commonplace in the home equity space. [1, 2] Further, emerging startups such as Hitch are now offering back-end platforms for lenders to white-label these services.

Further, it appears that Figure simply records the data from conventionally originated loans to its homegrown blockchain after-the-fact, according to its disclosures. A former employee corroborated this, telling us:

“Prior to joining Figure, I was convinced that everything was happening on chain, like beginning to end. And that's not the reality, right? … Like once the loan is actually funded, that transaction is recorded on the Provenance blockchain, not before.”

Despite management claims, we see the company disclosures as clear evidence that blockchain plays no role in the origination of Figure loans and its blockchain simply acts as a glorified database after-the-fact. We believe this not only undermines the company’s value proposition, but also its premium valuation.

Despite Clear Disclosures That Figure’s LOS Does Not Utilize Blockchain As Described, Mike Cagney Continues To Claim That Figure Originates “Native” Loans On The Blockchain While Ridiculing The Use Of Tokenized Assets Or Digital Twins

Reality Check: Figure’s Disclosures To Regulators Literally State That Its Loans Are “Digital Twins,” Or “Tokenized” Versions Of Real World Assets, “As Documented Through Traditional Legal Documents”

Figure’s leadership has repeatedly asserted that the company’s loans are “native” to the blockchain (i.e., assets that only exist within the digital realm like Bitcoin), rather than being “digital twins,” which are tokenized representations of real world assets.

For example, Cagney’s wife June Ou, a Figure co-founder and director of the company, stated in a 2025 interview:

“So if you put an asset and you tokenize it on the blockchain, but it’s just a digital twin, there is no point because you could sell that asset on paper.”

In December 2025, Cagney said that Figure’s partners “originate loans native on public chain.” On January 7, 2026, Cagney further confirmed in an X post that the loans on Provenance Blockchain (i.e., Figure’s HELOCs) “are native, not digital twins.”

Within 30 minutes, Cagney, through another X post, said that the blockchain did not work if assets were not originated on-chain and implied that digital twins are “fake assets.”

Yet, Figure’s filings with the SEC explicitly state that its loans are digital twins, or tokenized representations of real-world assets.

Beyond the contradiction between Figure’s co-founders’ statements and the company’s SEC filings, the founders have said there is “no point” and it “doesn’t work” using tokens to represent real-world assets— exactly what Figure is doing.

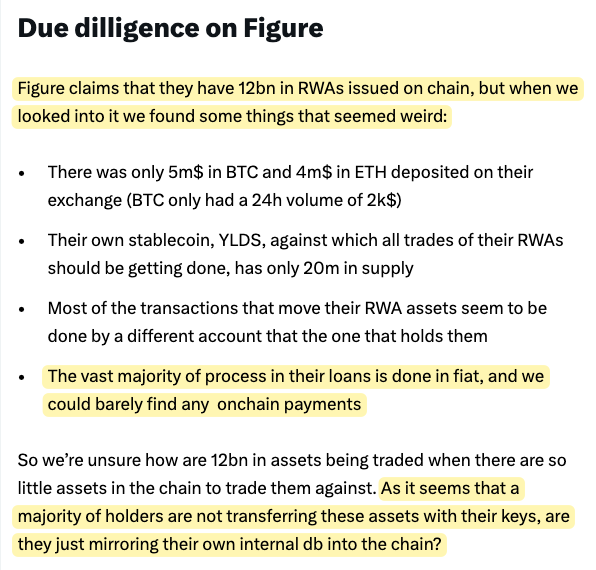

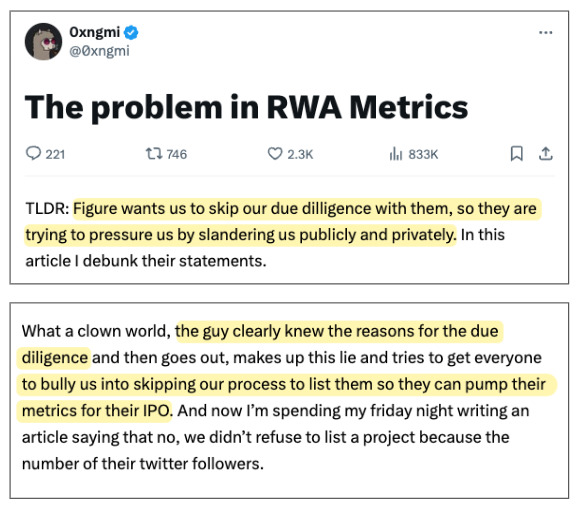

Last Summer, Cagney Engaged In A Twitter/X Feud With Crypto Data Aggregator DefiLlama After It Refused To Include Figure’s Claimed $11 Billion In “On-Chain” Assets In Its Reporting, Due To A Series Of Red Flags it Outlined In An X Post

DefiLlama’s Founder, Who Has Been Described As “One Of The Few Honest Actors” In The Crypto Space, Accused Figure Of Wanting To “Pump Their Metrics For Their IPO,” Asking If Figure Is “Just Mirroring Their Own Internal [Database] Into The Chain?”

As of August 1, 2025, Figure claimed that it had $11 billion in “real-world assets total value lock.” This total value locked (“TVL”) metric is defined as the amount of crypto assets that is deposited in a protocol (e.g., a blockchain). This TVL would put Figure HELOC among the top 20 largest crypto assets, per Cagney.

In September 2025, Cagney took to X to express his frustration at a popular crypto data aggregator called DefiLlama for not including Figure’s HELOC loans in its reporting for TVL on the Provenance Blockchain.

Cagney claimed that DefiLlama’s refusal to list Figure’s loans was due to Figure not having enough X followers.

DefiLlama’s founder, who has been called “one of the few honest actors left” in crypto, replied with a longform post explaining that its refusal to list Figure’s loans had nothing to do with its X followers, but a series of red flags that made Figure’s claimed on-chain assets unverifiable.

Critically, DefiLlama questioned whether Figure was just “mirroring their own internal [database]” to the blockchain.

DefiLlama’s founder also accused Cagney of making up the “lie” about Twitter followers to “bully” it into skipping its due diligence process so that Figure could “pump their metrics for their IPO.”

After the exchange, Cagney posted on X that “we’ve cleared it up and are working together to be able to report the assets.” Six months later, DefiLlama still does not include Figure’s loan data in its reporting for the Provenance Blockchain.

Figure’s CEO, Michael Tannenbaum, Has Called The Use Of Excel Spreadsheets To Share Loan Data “Crazy” And Susceptible To Fraud, Evangelizing About How The Blockchain Makes Failures Such As Subprime Lender Tri-Color “Impossible”

Reality Check: We Found That Figure Uses Excel Spreadsheets To Share Loan Data With Relevant Parties, Like Audit Firms And Whole Loan Buyers, Often With Version Numbers Like “v3 (6)” Indicating Manual Compiling, Editing, And Sharing

In June 2025, Figure co-founder and director, June Ou, said during an interview:

“The world right now, unless they’re on blockchain, is they still use spreadsheets, right? They use spreadsheets, they call loan tape— because it used to be a tape back in the day. And they email these spreadsheets back and forth.”

After the collapse of subprime Tricolor, which was reportedly manipulating Excel data to make car loans appear current, Figure’s CEO, Michael Tannenbaum, published an article claiming that “Tricolor couldn’t happen on Figure” due to the blockchain’s “truth over trust” model.

That same month, Figure’s CEO again criticized the use of spreadsheets to share loan data in the collateral management ecosystem:

“It sounds crazy, but this is how the world works. It's all about spreadsheets and wires and waiting for collateral and then checking things after the fact.”

Instead, Figure’s platform purportedly offers a tool called “Portfolio Manager,” which allows for easy “auditing and verification" of loan data stored on the blockchain, according to Figure’s CEO. [1, 2]

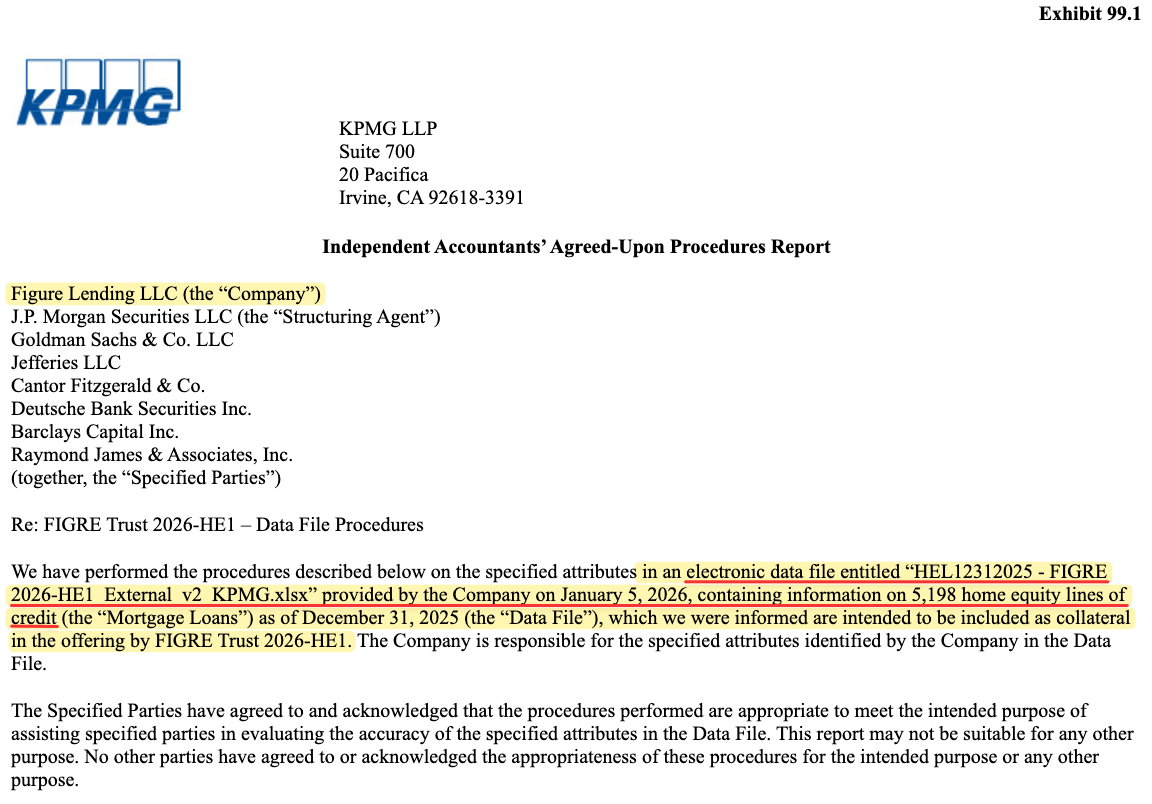

Despite characterizing them as archaic and supposedly having a superior process, Figure uses spreadsheets to share loan data with third-parties in its securitizations, according to an Agreed-Upon Procedures Report from KPMG.[1]

As part of the securitization process, after loans have been originated, Figure engages KPMG to select a random sample of its loan pool from an Excel spreadsheet and then compares the attributes in the Excel spreadsheet to the data in the agreements and other supporting documents, according to KPMG’s Agreed-Upon Procedures Report, prepared for Figure and several banks. The procedure described in the report states that KPMG compared the attributes in the Excel spreadsheet to “copies of the Mortgage Loan Agreement, Servicing Statement, Servicing Portal Screenshots, Notice of Servicing Transfer, Deed of Trust, and Credit Report Data.” ↩︎

We reviewed a total of 26 reports from KPMG related to Figure’s securitizations from March 2023 to March 2026 and found that spreadsheets were used in every case.

Alarmingly, these spreadsheets appeared to follow no labeling convention and included text such as “External_v5” and “v3 (6),” which indicates multiple copies and versions as well as manual compiling, editing, and sharing.

Figure’s use of Excel spreadsheets is not limited to its auditors. We asked a former Figure employee whether the company shared most of its loan/collateral tapes via email and in a spreadsheet with whole loan buyers.

“Yep. Again, maybe that’s changed, but I doubt … that’s how a lot of the funds and how the banks do things.”

If Figure relies on “immutable” data from the blockchain for its capital markets activities, we see no reason why it should be sending files that can be manipulated, such as spreadsheets, back and forth between involved parties – the very practice its executives have heavily criticized.

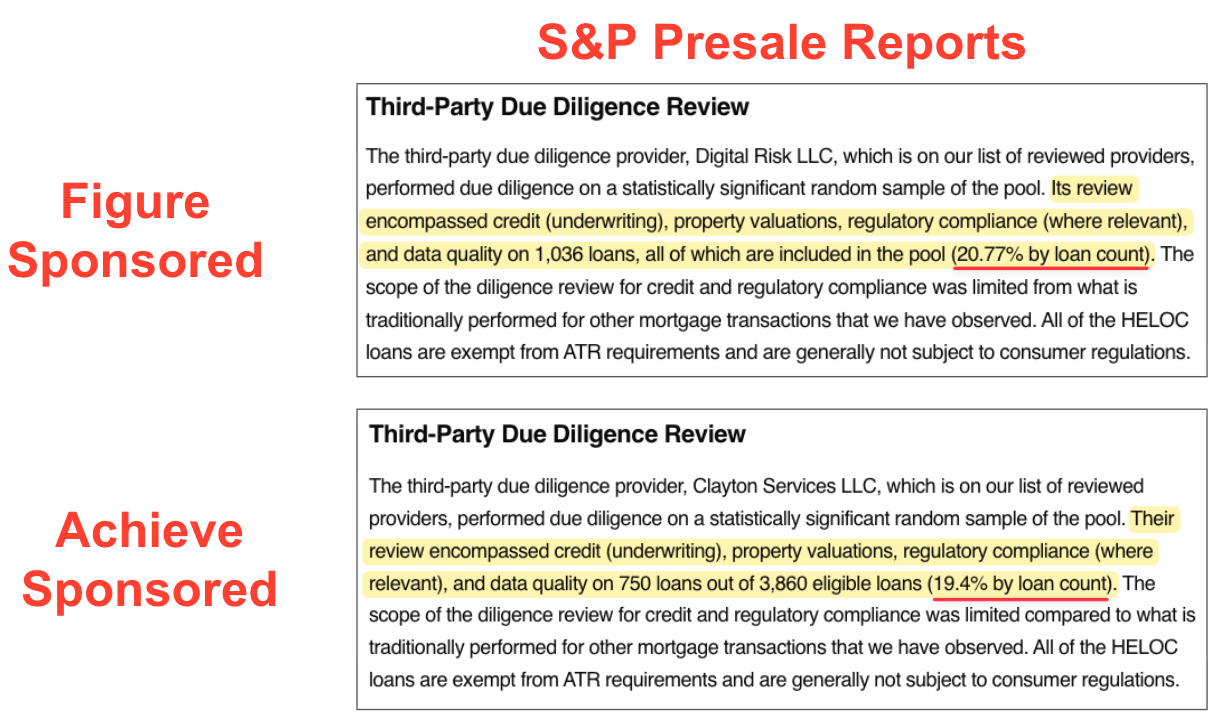

Mike Cagney Claims That “Because Of The Way We Use Blockchain,” Auditors For Its Securitizations Only Need To Review 20% Of The Loan Pool, Which Figure’s CEO Has Said Is “One Of The Clearest Examples Of Blockchain Adding Value”

This Is False, Per An Employee From HELOC Lender Achieve, Who Told Us: “It Is Not The Blockchain That’s Allowing Them [Figure] To Do 20% … It’s The Requirements Of The Rating Agencies As Well As The Underwriters”

Direct Competitor Achieve, Which Does Not Claim To Use Blockchain, Also Reviews 20% Of Loan Pools, According To Securitization Pre-Sale Reports

Another claimed efficiency of blockchain-hosted data is an 80% reduction in third-party review costs for securitizations, which CEO Michael Tannenbaum has described as “one of the clearest examples of blockchain adding value.”

Cagney explained this specific blockchain-enabled advantage in a March 2025 interview, saying that “because of the way we use blockchain, we get AAA rating with 20% of loans audited.” He later clarified in another interview that Figure ingests data “into blockchain, and the immutability of that,” rating agencies lowered Figure’s requirements to 20% to 30% of loans.

This, too, is an egregious misrepresentation of Figure's claimed blockchain-enabled advantages.

Ratings agencies require that a “statistically significant” percentage of a loan pool be audited, which in many cases could be ~20% depending on the requirements of the underwriters and ratings agencies.

This was corroborated by a senior employee from HELOC originator and close peer, Achieve.

“It is not the blockchain that’s allowing them [Figure] to do 20%, not 100% … It’s the requirement of the rating agencies as well as the underwriters. So, like, S&P could probably be comfortable with less than 20% … one of the underwriters that we [Achieve] work with, one of the same ones that they work with, requires 20%.”

Despite not using “immutable” blockchain-based data, Achieve’s December 2025 “AAA” securitization pre-sale report states that just 19.4% of its loans were reviewed for due diligence purposes.[1]

Achieve also securitizes the loans it originates. A search of Achieve’s website only generated 1 hit for the word “blockchain,” related to a job opening with part of the role description saying “Explore opportunities to innovate through the use of emerging technologies like AI, blockchain, and cloud solutions.” This Achieve sponsored securitization received a AAA rating from S&P, the same rating as a similar vintage from Figure. ↩︎

We see this as another misrepresentation from Figure’s leadership about the ostensible benefits of its blockchain technology that drive its premium valuation.

Part 2: Figure Is A Graveyard Of Failed, Flailing, And Internally Propped-Up Blockchain Projects Including Figure Markets, Figure Connect, And Democratized Prime

Over the last several years, Figure has announced a flurry of buzzword-laden blockchain initiatives, including Figure ATS, Figure Pay, Figure Equity Solutions, Figure Markets, Figure Connect, YLDS, HASH, Democratized Prime, Hastra, OPEN and most recently, Figure Forge.

Many of these projects have stalled or failed to gain significant traction in the markets they are ostensibly designed to disrupt – or, as in the case of Figure Connect and Democratized Prime, are largely propped up by Figure itself.

Background: Mike Cagney Has A History Of Promoting Supposedly Breakthrough Blockchain Projects That Either Stalled Entirely Or Failed To Gain Significant Traction

“They Love That Moniker Of Being A Sort Of Blockchain-Based Entity” — Former Figure Employee

Figure has launched various blockchain-themed projects over the years that, despite Mike Cagney’s grandiose claims, have either failed to gain significant traction or stalled entirely. Below, we highlight just 3 examples.

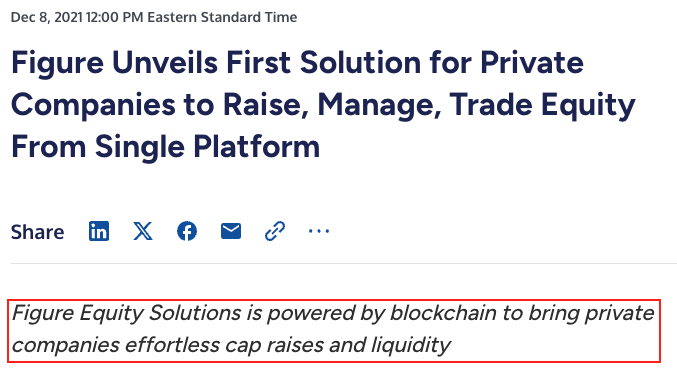

Failed Project #1: Figure Equity Solutions, also known as Adnales, was announced in December 2021, as a single platform for private companies to “raise, manage, and trade equity.” According to Figure, the platform would compete directly with market leader, Carta, a substantial market opportunity given Carta reportedly produces hundreds of millions in annual revenue.

We were unable to find any evidence, however, that Figure Equity/Adnales currently functions as a public-facing brand today. It appears to have been relegated to a back-end tool for other parts of Figure’s business. Critically, Figure Equity Solutions did not report any activity to the SEC until 2025. [1, 2, 3, 4]

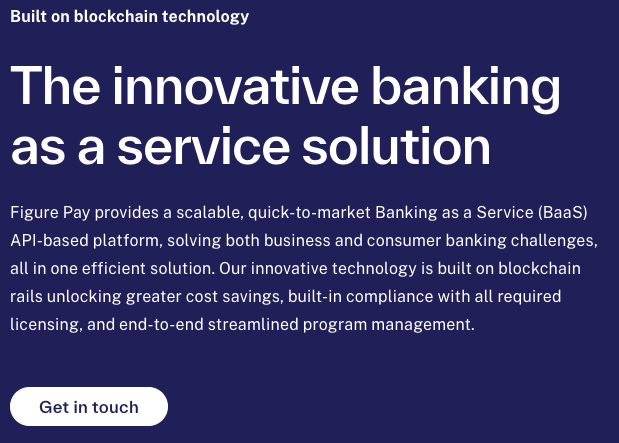

Failed Project #2: Figure Pay was announced in September 2022 as Figure’s Banking-as-a-Service (“BaaS”) platform that would use “blockchain rails” to “bring the financial services ecosystem into the modern world,” according to Mike Cagney.

While Figure Pay was initially positioned as a customer-facing brand, today the website leads to nowhere and the business appears to have been quietly wound down after reportedly failing to get a banking license.

Failed Project #3: Figure Markets was announced in March 2024 and described as an “exchange of everything” that Mike Cagney said would position Figure to compete directly with Coinbase and Binance, while allowing investors to “seamlessly” trade crypto, stocks, and alternative assets.

Two years later, Figure Markets has failed to gain a meaningful foothold in the hyper-competitive world of crypto exchanges. As of April 13, 2026, it is ranked #106 by CoinDesk. It does not generate any material revenue for the company, per its annual report.[1]

Even Figure’s $53 million in ADV appears to be greatly overstated by Figure’s HELOC token, which is not tradeable, according to our communications with Figure customer service staff. ↩︎

Based on our discussions with former employees, we believe that Figure’s endless stream of blockchain projects stems from its executives’ obsession with being viewed as a blockchain company rather than conventional home equity lender, as we will show in Part 5, and with one individual explaining:

“They love that moniker of being a sort of blockchain-based entity.”

Today, in our view, Figure is currently using even more “grandiose” claims to describe newer initiatives, which we believe are partially propped up by Figure itself, as detailed below.

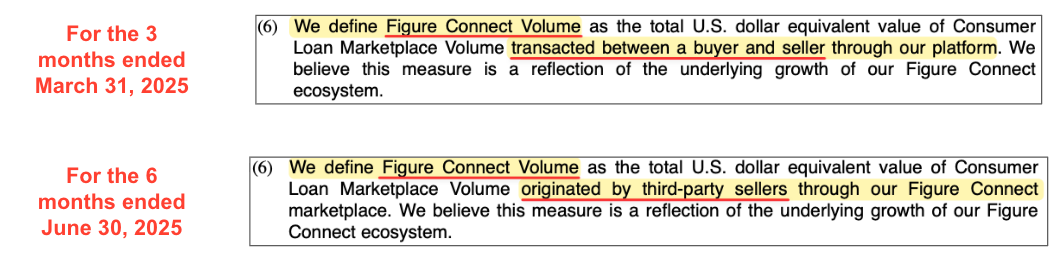

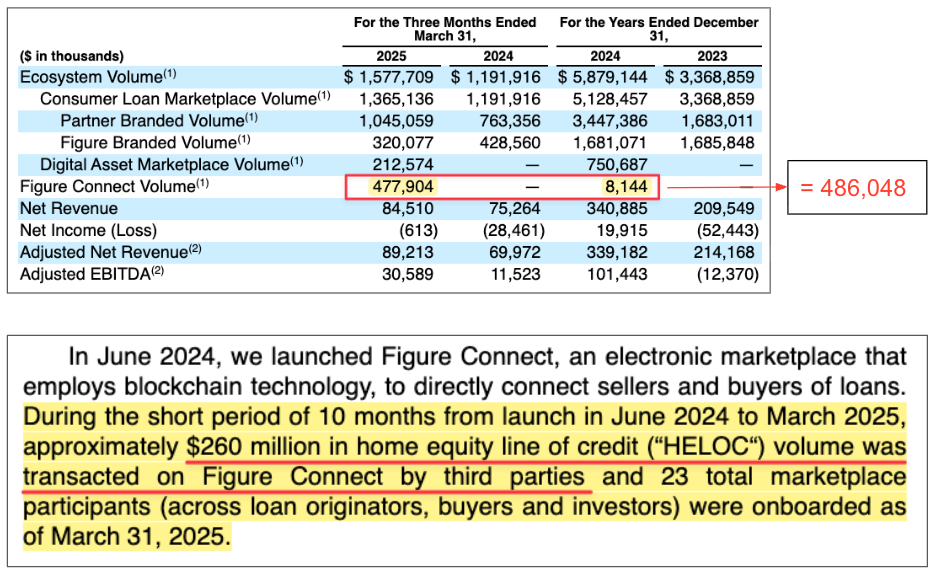

Figure Claims That Figure Connect, Its Loan Marketplace, Has Transacted $3.84 Billion Since It Was Created In June 2024— Experiencing A 320x Growth In Volume From $8 Million In 2H 2024 To $2.59 Billion In 2H 2025

Red Flag: In Q2 2025 Figure Made A Subtle Change To The Definition Of “Figure Connect Volume” From “Transacted Between A Buyer And Seller” To “Originated By Third Party Sellers” Through The Marketplace

Figure Connect, is an electronic marketplace that ostensibly uses blockchain technology to directly connect sellers and buyers of loans.[1]

Figure Connect seems to be a rehashing of a similar initiative called “Figure Loan Marketplace” that the company offered circa 2020, according to an archived version of Provenance’s website. ↩︎

Since its June 2024 launch, Figure Connect’s volumes have exploded from $8.1 million in the second half of 2024 to $2.59 billion in the second half of 2025. [1, 2, 3]

The seemingly impressive growth of the platform, however, coincided with a subtle change to how Figure defines volume on the platform. From Q1 2025 to Q2 2025 Figure changed the definition of the volume transacted through Figure Connect from “transacted between a buyer and seller” to “originated by third party sellers.”

We see this subtle change as an indication that Figure may actually act as a buyer in Figure Connect, as we will describe below.

Figure Management Claims That Figure Connect Is A “Capital-Light Marketplace” For Loans That It “[Does] Not Even Touch,” With The Company Collecting Fees For The Loans Traded On The Platform Between Third Parties

Reality Check: Figure Is Funding A Significant Portion Of Figure Connect Through Its Own Purchases, According To Credit Reports, SEC Filings, And Former Employees

“The Vision Was To Have This Marketplace And Make It Very Easy For Institutional Investors To Buy Loans. Back When I Was There, Figure Was Funding A Lot Of It, Like A Lot Of It” - Former Figure Employee

Figure Connect growth is especially impressive given the platform is allegedly “capital-light” since Figure claims it does not touch the loans transacted between third parties on the platform, according to an October 2025 interview with Figure CEO Michael Tannenbaum.[1]

As of September 30, 2025, Figure Connect represented 39% of total loan volume (i.e., ecosystem volume) during the first 9 months of the year, according to the company’s earnings release. ↩︎

“We built a pure marketplace, so 40% of total [Figure’s ecosystem] volume, we don’t even touch. It is not our license, it is not our money, it’s just the partner using our technology and then using our capital market … we launched Figure Connect, that pure marketplace, in June ‘2024 and then within a year it became 40% of volume— so pretty impressive.”

More recently, Tannenbaum has reiterated the “capital-light” nature of Figure Connect, while touting its rapid growth.

As of Q1 2025, Figure Connect volume since inception was $486 million. Only $260 million, however, was transacted on Figure Connect by third parties, according to Figure’s draft registration statement from August 2025. This indicates that Figure used its own balance sheet to support the remainder of the volume.

Figure's annual report also indicates that Figure likely uses its own balance sheet to acquire loans through Figure Connect.

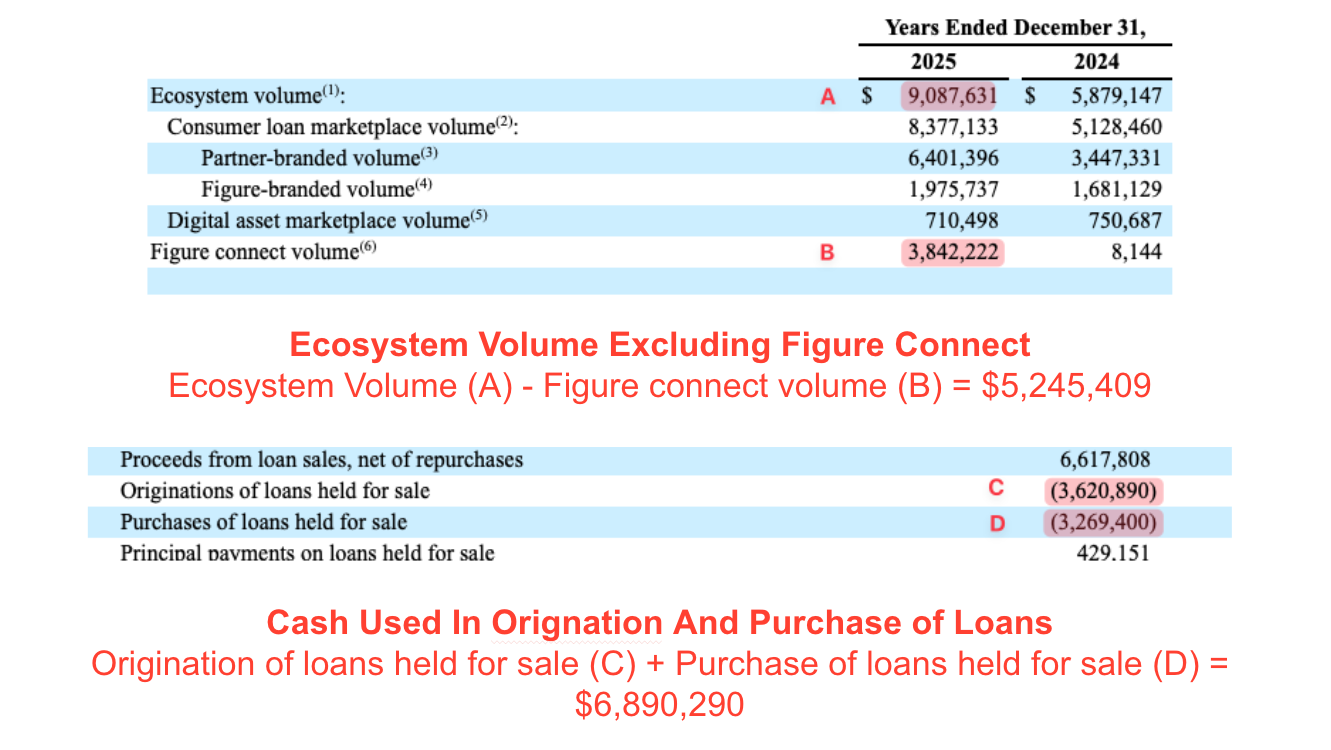

In 2025, Figure used $6.8 billion of cash to originate and purchase loans, according to its cash flow statement.

After subtracting Figure Connect volumes from the total ecosystem volumes, Figure and its partners appears to have originated $5.2 billion in loan volume in 2025 (i.e., total reported volume that does not include Figure Connect), indicating that the company likely used a substantial amount of cash to purchase consumer loans volume outside of its own originations, per its 10-K.[1]

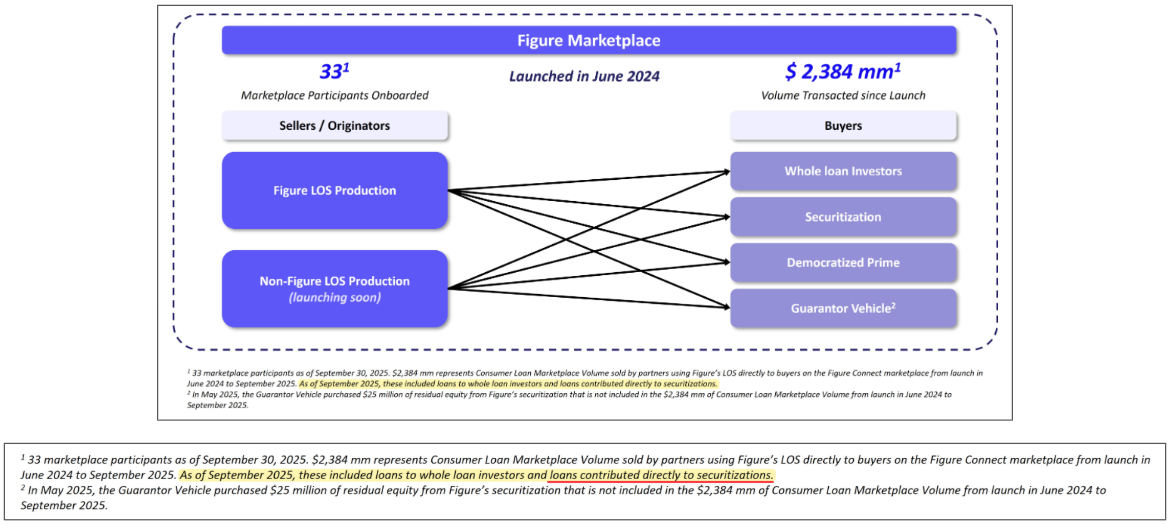

Moreover, Figure’s latest prospectus discloses that Figure Connect offers “access to rated securitizations” and that Figure Connect’s volume includes “loans contributed directly to securitizations,” according to a chart footnote in the same document prospectus.[1]

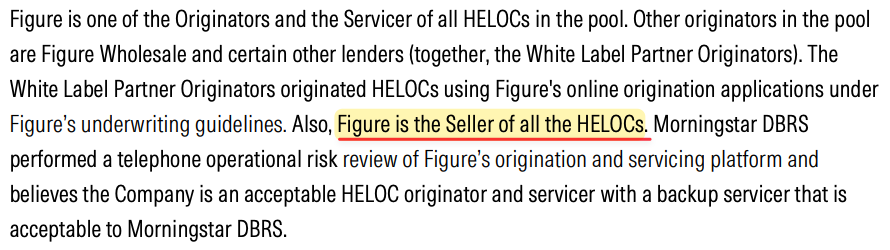

Figure acts as the seller of all HELOCs of its securitization, according to pre-sale reports from Morningstar DBRS. [1, 2]

As we see it, this implies that Figure acts as principal and uses its own capital to acquire loans that later are sold to securitization pools.[1]

Figure’s CFO said in the Q4 2025 earnings call that: “Our loans held for sale balance typically reflect the periodic timing of loan sale and securitization programs as we generally hold on to loans for a few weeks.” In our view, this indicates that Figure acts as principal of the loans that it contributes to securitization pools. ↩︎

We believe that the fact pattern supports Figure’s heavy involvement in Figure Connect as a substantial bidder, a view corroborated by a former Figure employee, who told us:

“[On figure connect] the vision was to have this marketplace and make it very easy for institutional investors to buy loans. Back when I was there, Figure was funding a lot of it, like a lot of it."

Since Figure is the sponsor of its securitizations, it is required to retain no less than 5% of the credit risk of the underlying assets, as established in the The Dodd-Frank Act Wall Street Reform and Consumer Protection Act of 2010, passed in the aftermath of the 2008 Financial Crisis.

This evidence suggests that Figure is playing a critical role supporting the bid within its own marketplace. As the company increases the amount of securitizations it issues, fed in part by the acquisitions of loans through Figure Connect, it will require more capital to satisfy the risk retention requirements. As we see it, this is anything but a capital-light model.

Example Of Lack Of Institutional Interest in Figure Connect: In February 2025, Figure Announced A JV With Investment Firm Sixth Street To “Bring Over $2 Billion Of Liquidity” To Figure Connect

Fast Forward To December 2025: Sixth Street Has Contributed Less Than 25% Of Its Commitment, And The JV Appears To Have Not Purchased A Single Loan, According To Figure’s SEC Filings

The JV Agreement Had An Initial Term Of 12 Months, Maturing In February 20256, But Figure Has Not Announced A Renewal Or Provided An Update

In February 2025, Figure formed a JV with investment firm Sixth Street to provide an “always on” bid to purchase HELOC loans originated through Figure’s LOS and sold through Figure Connect, according to Figure’s annual report.

Sixth Street committed to contribute $200 million for 95% of the JV, which was expected to be “recyclable equity” that would utilize leverage to provide “billions of dollars of committed financing,” according to a company’s prospectus.

As of September 2025, 7 months into the partnership, the JV had not purchased a single loan through Figure Connect but had instead spent $25 million to purchase residual tranches from Figure’s own securitizations, according to a company prospectus.

Meanwhile, as of December, the two parties have only funded the JV with $49.6 million, a fraction of the original $200 million, without providing any details if the capital was used to buy HELOCs or further securitization tranches, per Figure’s annual report.[1]

The JV had a return on equity target of 17%, and it is not obliged to buy Figure HELOCs if its “return on equity thresholds,” are not met, according to the company’s prospectus. This structure encourages the JV to buy Figure HELOCs, “when prices are more attractive, typically in time of less liquidity or demand for assets.” ↩︎

With an initial term of 12 months, the JV would have ended ~2 months ago, but Figure has not disclosed a renewed agreement or an update of any kind. We believe the partnership is likely dead in the water.

In June 2025, Figure Launched A DeFi Initiative Called “Democratized Prime,” Described By Mike Cagney As “THE Killer App” That Would “Disintermediate” Legacy Financial Middlemen, Providing Superior Interest Rates To Both Borrowers And Lenders

Reality Check: Figure Appears To Be Paying Above-Market Interest Rates Of ~8.7% To Attract Lenders To The Platform, While Its Conventional Warehouse Lines Cost Just ~5.5% But Remain Largely Unused, According To Figure Financials

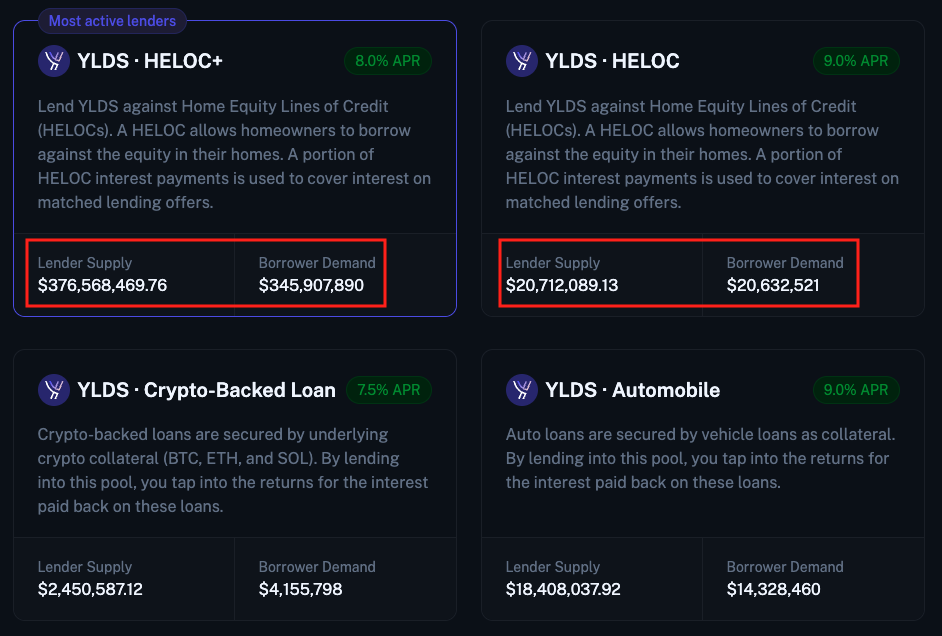

Despite Launching 10 Months Ago, Prime Has Little Traction Among Borrowers With Figure’s Own HELOC Pools Representing ~94% Of Demand For Capital

Democratized Prime is Figure’s DeFi marketplace “connecting sources and uses of capital, where common borrowers face off against common lenders,” per Figure filings.

Last month, Mike Cagney posted on X, citing the “big growth” in Democratized Prime, which he described as “THE killer app.”

Despite his claims of “big growth,” Democratized Prime has just 8 lending pools, and Figure’s two HELOC lending pools represent 94% of borrower demand on the platform.[1]

As of April 9, 2026, there were 8 available lending pools available on Democratized Prime representing a total of $388 million in borrower demand, including two backed by HELOCs managed by Figure. Figure’s two HELOC pools represented 94% of all borrower demand on the platform. ↩︎

In an October 2025 interview, Mike Cagney said that Figure itself uses Democratized Prime to finance loans cheaper than it could “through the street,” ostensibly referencing conventional warehouse financing facilities.

“We started bringing loans over to Democratized Prime and financing them there. And you know, we brought $10 million over, and sure enough, we financed it cheaper than we could have through the street. Brought another $10 million over, did the same thing.”

This claim, however, is untrue.

A footnote in Figure’s 2025 annual report states that the company paid average interest rates of 8.7% to borrow ~$190 million from Democratized Prime — rates that seem to be relatively high in the DeFi space, according to a presentation from Figure.

Meanwhile, Figure has conventional warehouse lines that only charge ~5.5% and which have hundreds of millions of dollars in unutilized capacity, per its annual report.[1]

Between 2024 and 2025, warehouse facilities went from representing 65% of the company’s total debt in 2024, to just 3.86%, while Democratized Prime climbed to 34% of debt, per its annual report.

Beyond the higher expense associated with Democratized Prime, it comes with far less stability since lenders can withdraw their funds “within an hour,” according to Figure’s website. Figure’s conventional warehouse financing, on the other hand, has agreed-upon maturity dates far in the future.

In other words, it appears as if Figure is not only operating as the primary borrower in its “DeFi” platform, but also offering uneconomic above-market rates to attract lenders to the platform. We see this as a waste of cash potentially aimed at engineering traction for what looks to us like yet another of its flailing DeFi projects.

Figure’s CEO Claimed In A CNBC Interview That The Company’s Stablecoin, YLDS, Is “The Oil Of [Figure’s] Capital Markets, And So, Loans Are Settled And Serviced In YLDS”

We Struggle To Understand How This Could Be Possible When 99% Of The YLDS Supply Was Controlled By Figure And A Single Passive Investor At The End Of 2025, And While Figure Only Accepts ACH And Wire Payments For Loan Payoffs

In February 2025, Figure launched “the first interest-bearing transferable stablecoin,” YLDS, which is native to the Provenance Blockchain and registered with the SEC. Figure’s CEO has described YLDS as the “oil of our capital market,” claiming that loans are “settled and serviced in YLDS.” [3:55]

We do not see how YLDS could be the “oil” of Figure’s capital markets, when Figure itself and a single passive investor controlled 99% of the YLDS supply at the end of 2025.[1]

As of December 31, 2025, there were $328.21 million YLDS in circulation, per Figure’s 10-K. Figure Certificate Company discloses on its balance sheet that it owes third parties $76.11 million, including accrued interest, this is the same amount reflected in Figure’s financials as liabilities from Figure Certificate Company. Figure Certificate Company’s annual report also showsthat $252 million of certificates are controlled by Figure and affiliates. Moreover, Figure also records an FCC liability of $2.05 million to related parties. This implies, by intercompany elimination, that out of the $328.1 million outstanding, $250 million worth of YLDS are owned by Figure. By the end of 2025 and through January 2026, Ondo Short-Term US Treasuries Fund, a fund that offers exposure to US Treasuries, held ~$75 million of YLDS, per internet archives of the fund portfolio holdings. (1, 2) ↩︎

Notably, in its due diligence on Figure, crypto data aggregator DefiLlama highlighted a lack of evidence that YLDS is widely used for transactions on the Provenance Blockchain.

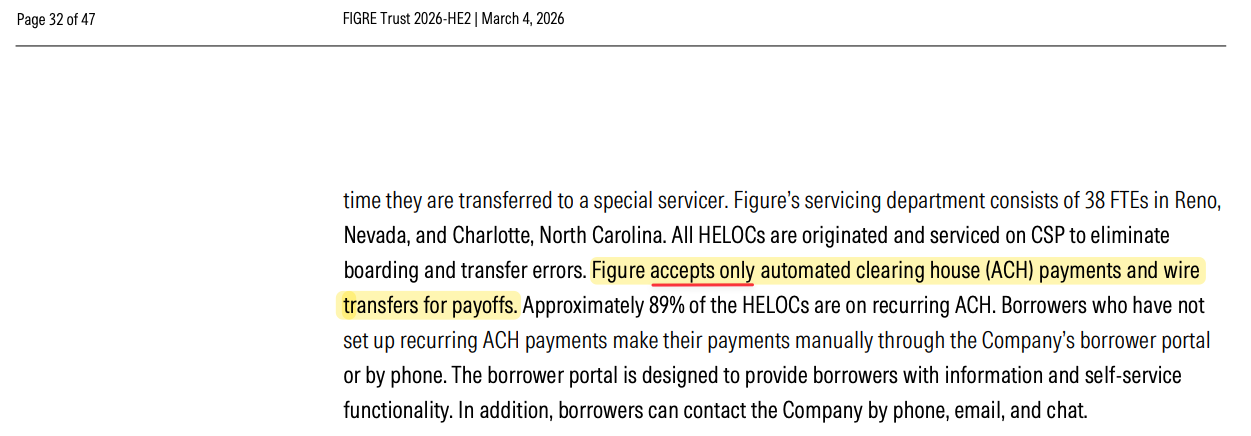

Further, it is unclear why Figure’s CEO would say claim its loans are “serviced” in YLDS, since Figure “accepts only automated clearing house (ACH) payments and wire transfers for payoffs,” according to its latest HELOC pre-sale securitization report from DBRS Morningstar.

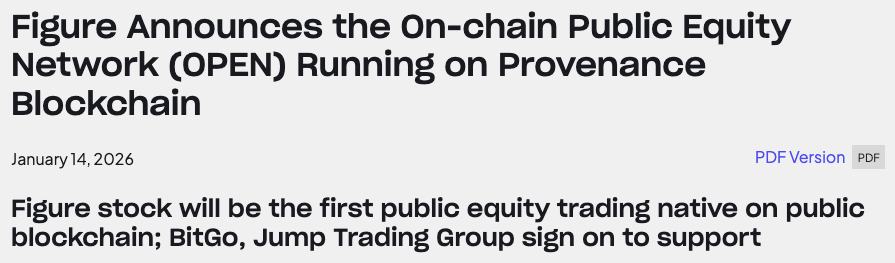

In Early 2026, Figure Introduced OPEN, An Exchange For Listing Equity Natively On The Blockchain, And Listed 4.375 Million Of Its Own Shares

Mike Cagney Said That “We Expect Many FIGR Shareholders To Move Their Stock To OPEN” And That It Was The “Beginning Of The True Renaissance Era Of Blockchain”

Yet Just 2 Months After Listing Figure Shares In OPEN, ~86% Of Shares Have Left The Network While Trading Volume Has Plummeted To Less Than $55k Per Day And No Other Listings Have Materialized

In January 2026, Figure announced the On-chain Public Equity Network (“OPEN”), a platform for companies to list their equity natively on the Provenance Blockchain.

Figure claimed that OPEN represents a “massive” $600 billion revenue opportunity, with a corresponding claim by Mike Cagney who said OPEN is an example of the “true renaissance era of blockchain.”

Shortly thereafter, Figure announced that it had completed an offer of 4.375 million of its own shares on OPEN, with Cagney saying, “we expect many FIGR shareholders to move their stock to OPEN.”

Instead, the opposite has happened.

As of this writing, only 690,295 Figure blockchain shares remain in OPEN, with 87% concentrated in just 3 accounts, according to Provenance Explorer. This implies that 86% of the all blockchain shares were converted off the blockchain to Nasdaq-traded shares.[1]

These blockchain shares can be converted to class A common shares that trade on Nasdaq, and Nasdaq-traded shares can be exchanged for blockchain shares, according to its prospectus. As of this writing, Provenance explorer shows a supply 690,195 shares for FGRD (i.e., Figure blockchain stock), same figure as in Provenance’s Pulse portal. (1, 2, 3) ↩︎

Cagney later disclosed that the listed shares were sold by insiders and that Figure itself acted as an initial buyer. Today, Figure’s blockchain-native shares appear to be of little interest to investors, with ~$54,000 in volume on Tuesday, April 14th.

To our knowledge, the company has not announced any further listings for OPEN.

Once again, we see OPEN and Figure’s native equity listing as a promotional initiative that has failed to meet the grandiose claims made by Figure management, most notably Chairman and co-founder Mike Cagney.

Part 3 – Figure’s Real Growth Drivers: Questionable Interpretation Of Regulations & Fast-And-Loose Lending Practices That Are Driving Accelerating Delinquencies

Rather than blockchain, Figure’s HELOC business appears to be fueled in part by misleading “bait-and-switch” advertising related to its characterization of its loans as “open-end” lines of credit versus closed-end loans.

Further, its lending practices are reminiscent of the fast and loose underwriting that preceded the 2008 Financial Crisis – most aptly characterized by the aggressive prioritization of speed and volume over quality.

Figure Is Able To Fund HELOCs In “As Few As 5 Days” Only Because It Characterizes Its Loans As “Open-End Credit” For Purposes Of Federal Regulations, Which Requires A Contemplation That Borrowers Will Do Repeated Draws

A Former Employee Told Us Repeated Draws Are Unlikely Due To Figure's Upfront "Full Draw" Requirement And That A Recharacterization To Closed-End Credit Would Come With A "Totally Different Set Of Regulatory Requirements"

“There’s A Lot Of Scrutiny, I Mean A Lot Of Scrutiny Around That … I Know We’re Calling It An Open-End Product, But At That Point, Until They Pay It Down, It’s Closed, I Mean That’s Almost A Closed-End Product There” - Former Figure Employee

One of Figure’s primary value propositions is the speed at which it can fund loans, per its own website. An employee from one of Figure’s white label partners explained that speed is a top priority in the HELOC space, and that Figure is “probably the fastest.”

“They [Figure] just have a very robust and good system when it comes to closing on HELOCs fairly quickly … We always want the loan to close as quick as possible. The faster, the better … I think [Figure] it’s probably the fastest.”

Speed translates into borrowers willing to pay a “pretty nice premium,” according to Figure’s Chief Capital Officer, Todd Stevens.

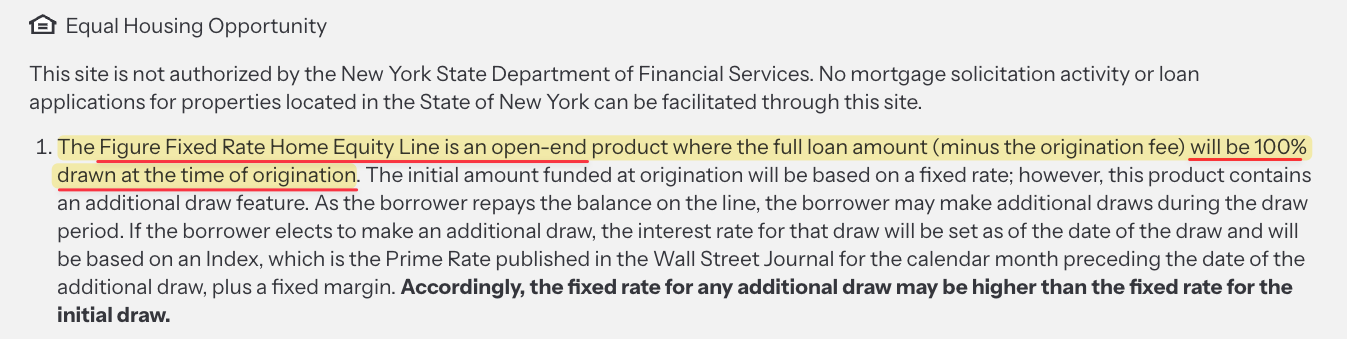

Figure’s competitive advantage of being “the fastest” could be at risk due to Figure’s requirement that borrowers draw their entire loan balances at close — contrary to the essence of a “line of credit”— which could result in its HELOC product being recategorized from “open-end” to“closed-end” credit under the Truth In Lending Act (“TILA”).[1]

TILA defines “open-end credit” as consumer credit that meets 3 criteria, including that “the creditor reasonably contemplates repeated transactions.” The guidelines from Consumer Financial Protection Bureau (“CPFB”) state that the creditor (i.e. Figure) must conduct and “objective analysis” to determine if they can “reasonably contemplate repeated transactions.” ↩︎

Open-end classification is only possible because Figure “contemplates” that borrowers will make “repeated draws,” which are unlikely due to Figure’s full-draw requirement and can only happen if borrowers pay down their balance, according to Figure filings. A former Figure employee told us:

“They make that max on the requirement for the draw amount, and I mean, that really changes the context of it being open-ended now even though it is, and you can redraw, it requires years of payment before you can do so. It’s not a typical line of credit.”

The former Figure employee told us there was a “lot of scrutiny” on this topic, and said a reclassification to “closed-end” would come with a different set of regulatory requirements.

“There’s a lot of scrutiny, I mean a lot of scrutiny around that … when you require a full draw like that, that’s almost to the point where you’re really looking at a totally different set of regulatory requirements … The Truth in Lending Act kinda has clearly delineated information about those types of almost, again, I know we’re calling it an open-end product, but at that point, until they pay it down, it’s closed, I mean, that’s almost a closed-end product there.”

Close-end credit is subject to more strict laws and rules, as disclosed by the company on its latest prospectus.

Instead of an open-end line of credit (i.e., HELOC), Figure’s product appears to be closer to a Home Equity Loan, also known as a Closed-end Second (“CES”).

Unlike HELOCs, CES must comply with TILA-RESPA Integrated Disclosure (“TRID”) rules, according to the National Credit Union Administration. These rules include a 7-day waiting period before closing for a borrower to review the loan terms. This would automatically limit Figure’s ability to close in 5 days.

TILA also mandates that a creditor must verify that a borrower has the ability to repay, through a much more stringent verification process than is used for open-end loans. More on this below.

As summarized by Figure in its latest prospectus, a recharacterization of Figure’s HELOCs as closed-end credit “would have a material adverse effect on our business, financial condition, and results of operation.”

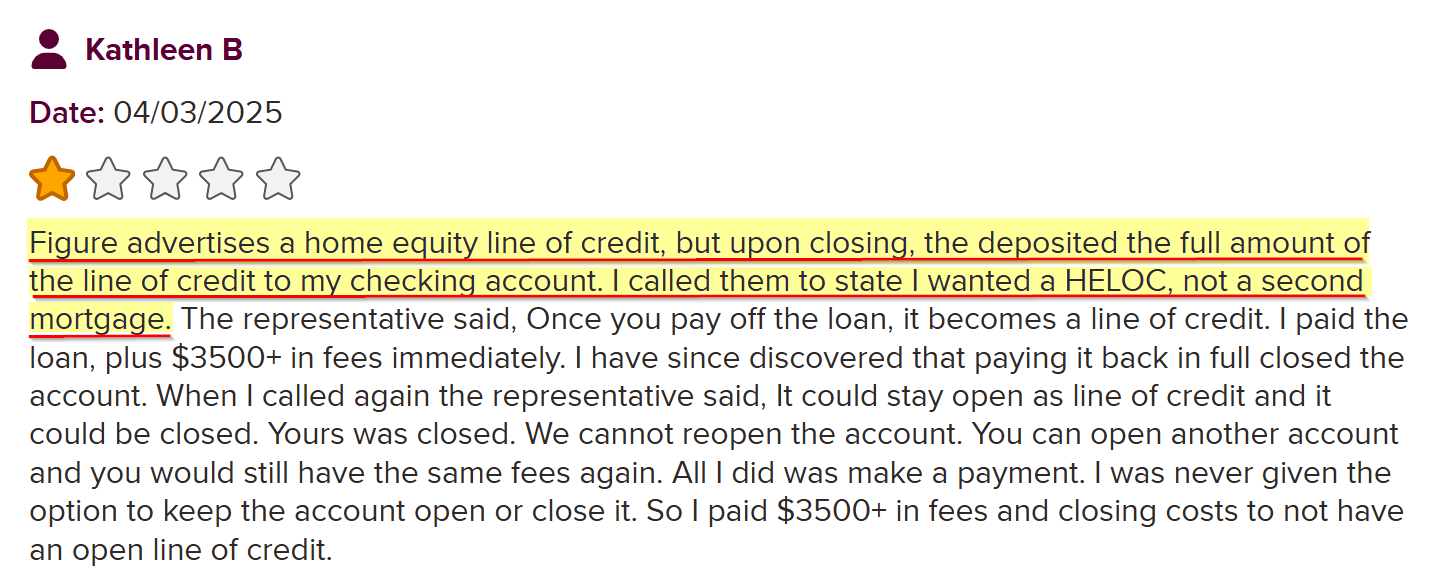

Figure’s Forced Draw At Origination Has Sparked Consumer Backlash, Resulting In Complaints With The Consumer Financial Protection Bureau (CPFB), A Class Action Lawsuit, And Negative Reviews Accusing The Company Of False Advertising

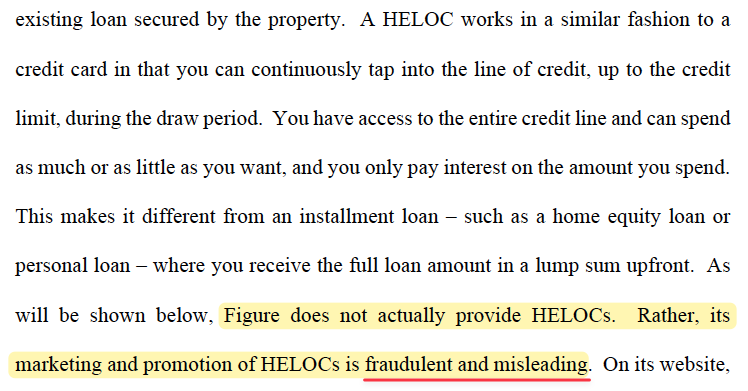

In 2024, a class action lawsuit was filed against Figure, alleging that the company “marketing and promotion of HELOCs is fraudulent and misleading.” The complaint cited dozens of customer complaints and alleged that “thousands of victims of Figure’s improper practices … resulted in damages far in excess of $5,000,000.” [Pgs. 5, 7-21]

The complaints have not stopped since the class action was filed. In February 14, 2025, a customer filed a complaint with the Consumer Financial Protection Bureau (CPFB) alleging that it was not until closing that he was informed that he had to take the full loan disbursement.

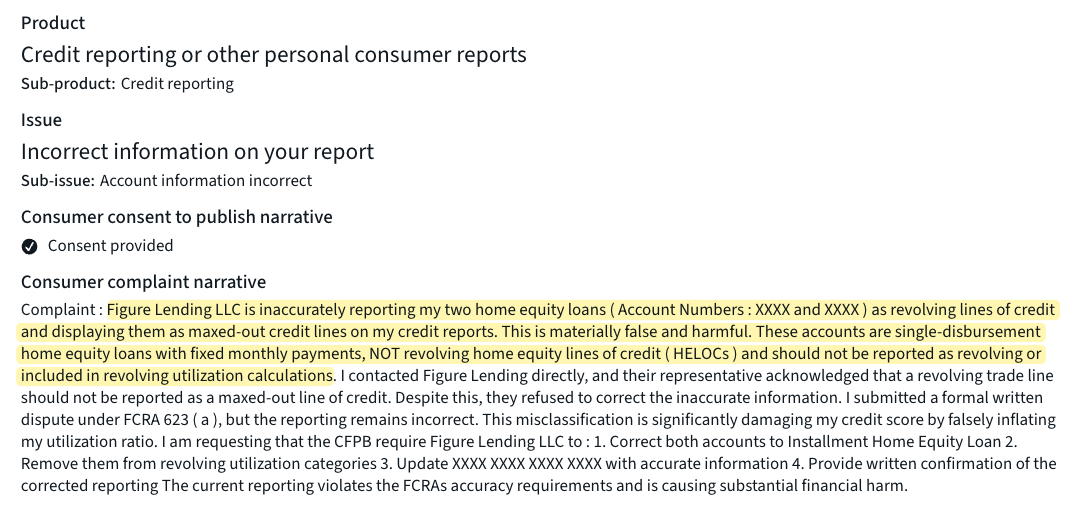

Again, on December 3, 2025, a customer filed a complaint with the CPFB alleging that Figure was reporting its loans as “as revolving lines of credit and displaying them as maxed-out credit lines on my credit reports. This is materially false and harmful. These accounts are single-disbursement home equity loans with fixed monthly payments, NOT revolving home equity lines of credit.”

Consumers have also complained about this practice on other forums, stating they were unaware that the full amount would be deposited in their accounts, per Better Business Bureau and Trustpilot reviews. [1 ,2, 3]

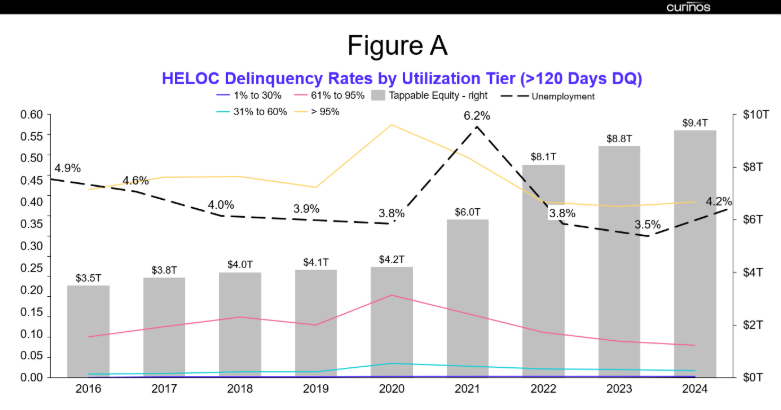

Borrowers That Utilize More Than 95% Of Their HELOCs Are Nearly 4x More Likely To Become Severely Delinquent Compared To Borrowers With Lower Utilization Rates, According To Advisory Firm Curinos

By Forcing A Full Draw At Close, Figure May Expose Itself To “Financial Stress” From “Mandatory Draw Requirements,” Effectively Trading Higher Upfront Origination Fees For Potential Tail-End Risk

Meanwhile, Some Of Figure’s Competitors Do Not Charge Origination Fees At All

Borrowers that utilize more than 95% of their HELOCs are nearly 4x more likely to become severely delinquent, according to research from Curinos, an advisory firm. A manager of Curinos warned about the “financial stress that is inferred from mandatory draw requirements.”

By forcing a complete draw at origination, Figure is able to charge an origination fee of up to 4.99% on the full balance of the loan. These fees represented 14% of revenue for 2025. Moreover, these fees are materially higher than those of its competitors.

For example, Bank of America (“BofA”), the largest HELOC lender in the US, does not require an initial full loan draw, does not charge application fees, closing costs, or annual fees on its HELOCs. Similarly, PNC, the third largest home equity lender in the US, charges a flat origination fee of up to $499, for its HELOC offering.

In our view, by giving borrowers more money than they may need with 100% loan utilization up-front, Figure may be trading higher short-term revenue for significant tail-end risk.

Beyond The Looser Regulatory Framework For “Open-End” Credit And The Requirement Of 100% Upfront Utilization, We See Other Red Flags In Figure’s Underwriting Criteria

Figure Uses More Forgiving FICO 9 Scores, Lends Against Second Homes & Investment Properties, And Uses “Less Rigorous” Documentation Standards, According To Morningstar DBRS

Open-end credit bears a lower underwriting bar than closed-end credit for originators. The latter is required only to check a borrowers’ ability to make minimum periodic payments, while the former must verify and document the borrower’s ability to repay the whole loan, not just meet the minimum payments.[1]

By treating its HELOCs as open-end credit, Figure only requires a check of a borrower's ability to make the minimum periodic payments (i.e., their ability to pay), according to the CFPB. On the other hand, closed-end credit is held to a higher underwriting standard, lenders must verify and document the borrower’s ability to repay a loan, not just meet the minimum payments, according to federal regulations. ↩︎

Beyond the lower bar for underwriting “open-end” credit and the risks of full-draw requirements, Figure’s lending business bears other hallmarks of aggressive underwriting.

- Rather than the industry standard FICO 8 score, Figure uses an alternative known as FICO 9, which is generally known to be more “forgiving” due to putting less weight on things like medical debt and third-party collections “that have been paid off and don’t have a negative impact.”

- Figure also lends against second homes and investment properties, which are typically perceived as higher risk. In Figure’s first securitization of 2026, these types of properties made up 7.65% of the loan pool, according to an S&P pre-sale report.

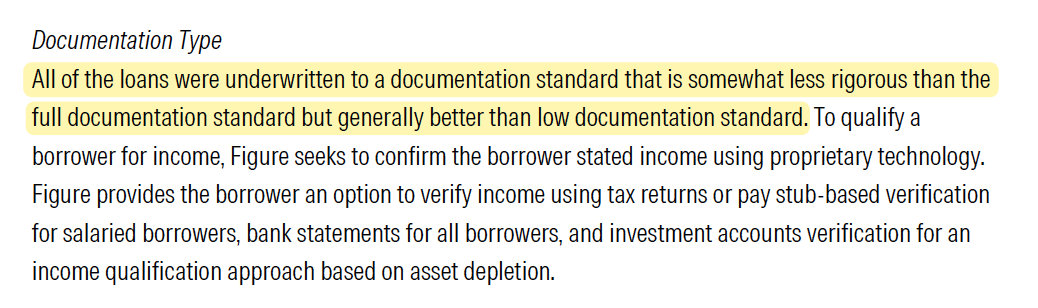

- Additionally, Figure underwrites loans “to a documentation standard that is somewhat less rigorous than the full documentation standard,” including “the income, employment, and asset verification methods used,” according to Morningstar DBRS. [Pgs. 4, 16]

While investors may think these practices are industry-standard, HELOC peer and close competitor Achieve does not use FICO 9, does not lend against investment properties, and uses “traditional documentation” to verify income, according to a presale report from its December 2025 securitization.[1]

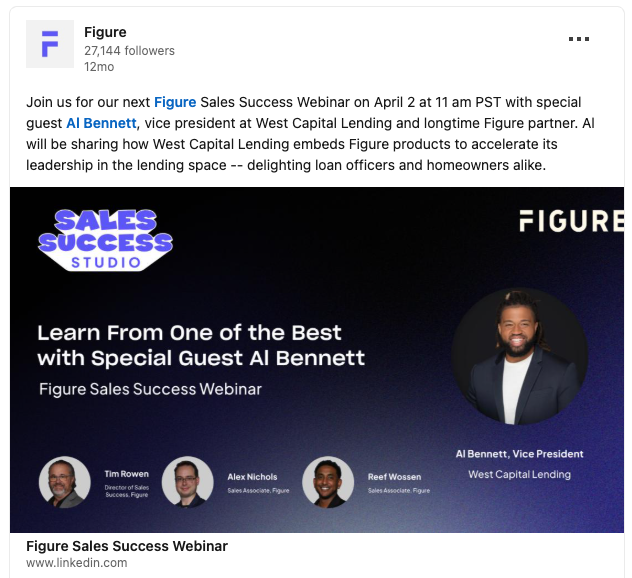

One Of Figure’s Highest Volume Partners Has Bragged Publicly About How “Easy” It Is To Sell A Figure HELOC, Saying There Is A “Very High Chance” Of Approval With “No Appraisal Needed, No Actual Income Docs Needed … It’s Easy”

One of Figure’s largest partners originating HELOCs is West Capital Lending. The #1 HELOC salesperson from West Capital, Al Bennett, has been described by Figure as a “longtime” partner and he was a special guest at a “Figure Sales Success Webinar.”[1]

West Capital Lending’s “number one Figure HELOC closer” is Al Bennet, according to a YouTube interview with Bennet. For the first 2 Figure HELOC securitizations of 2026, 18.8% and 27.4% of the loan pool were originated by West Capital Lending, according to DBRS Morningstar. (1, 2) ↩︎

In a recent interview Bennett bragged about how “easy” it is to qualify for a Figure loan.

“We have this HELOC, where they can literally take 30 seconds to 2 minutes, tops, to type in their information, and it will spit out basically a pre-approval, right? And as long as the income is verified, there is a very high chance that that loan will fund within 3 days, no appraisal needed, no actual income docs needed … It’s easy.”

Figure’s “easy” approvals, aggressive underwriting, and adverse selection associated with full-draw requirements may be the driving force behind the noticeable underperformance of Figure’s loans.

Cracks In Figure’s Loan Performance Are Already Starting To Show, With Delinquent Balances Of Loans Held For Sale Increasing From 3.91% In 2024 To 5.46% In 2025, According To Its Financial Statements

During The Same Period, Bank Of America, The Largest HELOC Lender In The US, Experienced A Reduction In Delinquencies Of Its Home Equity Loan Portfolio From 1.92% To 1.78% Of Outstanding Balance

We Also Compared Figure’s Loan Performance To Home Equity Loan Securitizations Including Loans From Peers Rocket Mortgage And Spring EQ, Revealing Double The Ratio Of 90+ Day Delinquencies Within Figure’s Loan Pools

From December 2024 to December 2025, Figure reported an increase in the unpaid principal balance of delinquent loans held for sale over total balance, from 3.91% to 5.46%, according to the company financial statements.[1]

Delinquent balance includes unpaid principal balance with 30-day delinquency and over, including balances in forbearance. To the best of our knowledge, Figure does not disclose the breakdown of these delinquent loans between HELOC loans or loans collateralized by digital assets. ↩︎

Over the same timeframe, HELOC market leader Bank of America reported a reduction in past due 30 days and non-performing loans from 1.92% to 1.79% of outstanding balances, according to the bank’s financial statements.[1]

Bank of America’s home equity loan portfolio includes HELOCs, home equity loans and reverse mortgages. BofA, however, currently only originates HELOCS. ↩︎

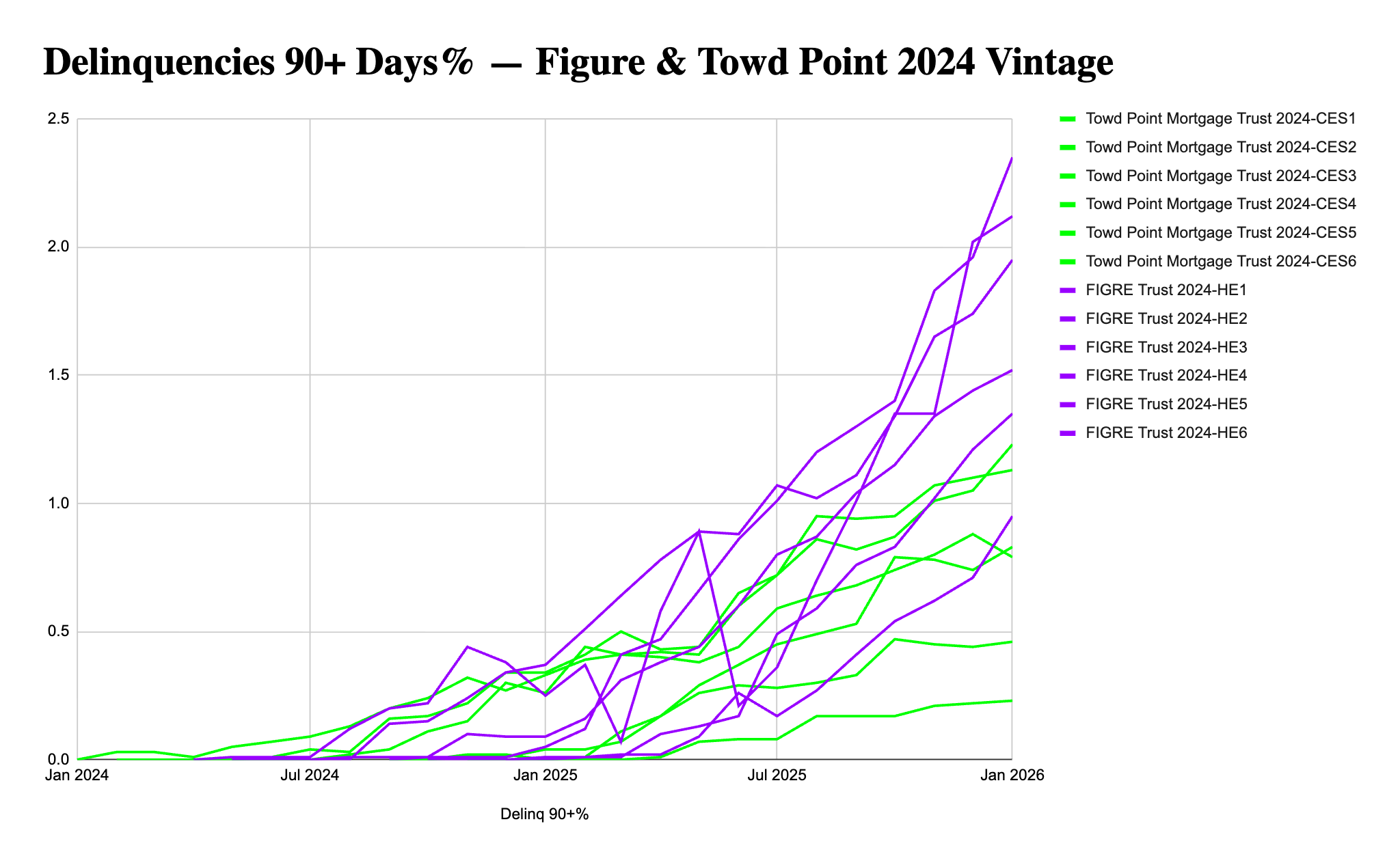

Meanwhile, 90+ days % delinquencies (as defined by Bloomberg) in Figure’s 2024 vintage securitizations are nearly twice as high as similar vintages from Rocket Mortgage and Spring EQ, whose loans underpin the “Towd Point Mortgage” securitizations referenced below.[1]

Peer sets include home equity loans (i.e., closed-end second mortgage). As previously explained, since Figure forces a full draw at origination, its loans resemble a home equity loan rather than a HELOC. Towd Point, an entity associated with Cerberus Capital, a private equity firm, is a serial issuer of home equity loans securitizations. These issuances mostly include loans originated by Spring EQ and Rocket Mortgage, according to presale reports we reviewed. (1, 2) In 2023 Figure only issued 3 securitizations, limiting the comp size. (1, 2, 3) While in 2024, Figure issued the same amount of securitizations as Towd Point did for CES securitizations. Bloomberg defines Delinquencies 90+% as the “percentage of loans which are 90 or more days delinquent, including loans in foreclosure, bankruptcy, and real estate owned (REO) buckets.” As of January 2025, the 90%+ delinquency average for Figure securitizations was 1.70% and 0.77% for Towd Point securitizations, according to Bloomberg. ↩︎

Mike Cagney claims that Figure credit performance is “solid and consistent” based on the “investment grade attach rate on our securitizations.” However, as the subprime crisis showed us, a AAA-rating attached to a securitization tranche does not directly reflect the credit quality of the underlying loan pool alone. Securitization credit ratings are also dependent on credit enhancement features such as subordination, over collateralization and excess spreads.

Overall, we believe that in addition to having no technological edge, Figure is underwriting worse loans than its peers.

Beyond These Early Signs Of Underperformance, We Believe Figure Exposes Itself To Tail-End Risk By Not Ordering Title Reports, Not Requiring Title Insurance, And Using Automated Valuation Models (“AVMs”) Instead Of Actual Appraisals

While Analysts Believe These Shortcuts Are Enabled By Figure’s “Technology,” A Former Employee Said These Practices Are A “Major Flaw” In Figure’s Underwriting, Creating “Really High- Risk Exposure” And Opening A “Wide Door For Fraud”

11% Of Loans In Figure 2026 Securitizations Show At Least A 10% Divergence Between Figure’s Valuations And Those Of A The Third Party Reviewer

Figure does not utilize title searches to check for preexisting liens or require title insurance from borrowers. Figure’s management has said that Figure’s “technology” obviates the need for title checks and title insurance.

A former employee, however, described this as a “major flaw” in Figure’s underwriting, explaining that Figure’s process does not thoroughly check for existing liens, potentially leading the company to believe it is in a first-lien or second-lien position when it is actually more subordinate.

“I liked being at Figure, but I have now gone to [redacted] because of some of my concerns. One of the other major flaws, in my opinion here, is that you do not ever have a title report before you make a $150,000 - $200,000 loan and you don’t have a title policy … presumably we’re buying a first-lien loan at max 85% LTV, well come to find out … we weren’t actually first position. We never had a buy-off of that first lien …”

Figure’s risk factors seem to corroborate this risk, describing the use of unspecified “lien data” rather than conventional title checks.

The former employee also criticized Figure’s use of Automated Valuation Models (“AVMs”) instead of actual appraisals, specifically citing potentially inaccurate “confidence scores” associated with types of these model-derived valuations.

“What they do is they utilize a confidence score that indicates accuracy … I know exactly what the consistency there is as far as day to day and what that looks like, and I can tell you, there were some major issues there. And it really gives you a true understanding of value and AVM, and even with a high confidence score, I saw many times where those were not appropriately positioned.”

Moreover, the third-party review reports of Figure’s securitization pools confirm issues with Figure’s AVMs.

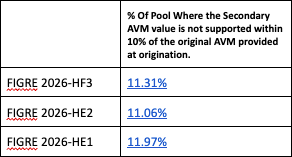

We found that for the last 3 Figure HELOC securitizations, 11% of the loan pool obtained a Valuation Event Grade of “C,” meaning that a secondary AVM ordered through another vendor did not support Figure’s AVM value within a 10% range, according to the third-party due diligence reports.[1]

Valuation Event Grade “C” definition: “The Secondary AVM value is not supported within 10% of the original AVM provided at origination. The valuation methodology did not meet the published guidelines and there were not sufficient compensating factors for exceeding published guidelines. The property is in below ‘average’ condition or the property is not complete or requires significant repairs.” ↩︎

Reinforcing the magnitude of the lack of title reports and the use of potentially unreliable AVMs, the former employee described these issues as a “top risk category” that creates “really high- risk exposure.”

“Those two pieces [AVMs and Lien Issues] really create, in my opinion, again, a really high- risk exposure.”

They added: “If I was going to risk score it … I would put this in a top risk category.”

Part 4: Figure’s Closely Affiliated “Provenance Blockchain” Is Neither Independent Nor Decentralized

Even if investors truly believe in Figure’s blockchain initiatives, we believe that red flags associated with the underlying ownership and governance structure of the Provenance Foundation and the clear signs of centralization within Provenance Blockchain could jeopardize Figure’s reputation in the market.

Figure Describes Provenance Blockchain As An “Independent Layer 1 Blockchain” And Claims That It Does Not “Participate Or Expect To Participate In The Development And Maintenance Of Provenance Blockchain”

Reality Check: Provenance Is Run By Figure Employees, Including Mike Cagney’s Wife, While Cagney Himself Appears To Be The De Facto Leader, According To Our Analysis Of The Provenance Telegram Channel

Despite Saying That It "Absolutely [Doesn’t] Control The Network,” More Than 65% Of Provenance Blockchain’s Native Token Appears To Be Owned By Figure, Affiliates Of Figure, And Cagney Himself, According To Cagney

Figure’s annual report describes Provenance as an “independent layer 1 blockchain” and the prospectus from a Figure subsidiary states that it, “nor any of its affiliates” (i.e., Figure) participate in the "development and maintenance of the Provenance Blockchain.”

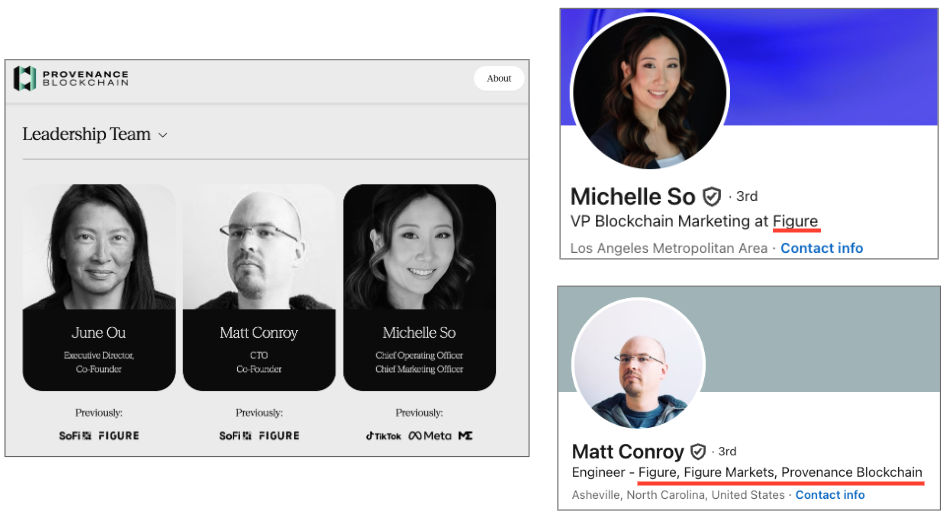

Provenance Blockchain’s Executive Director is June Ou, Cagney’s wife and a member of Figure’s board. Since at least July 2025, Provenance’s leadership team has been composed of Figure employees, according to archived and current versions of Provenance website and the employees LinkedIn profiles. [1, 2]

Moreover, it appears to us that Cagney is perceived to be a de facto leader by the Provenance Blockchain community, according to our analysis of his interactions on the Provenance Blockchain Telegram channel.

Particularly convincing to us is the fact that, since at least February 2025, Mike Cagney has used the pronoun “we” when addressing community concerns, providing insights into Provenance’s priorities and strategies and suggesting to us that he holds a leadership role within Provenance Blockchain. [1, 2, 3]

Our opinion that Cagney leads the Provenance Blockchain community is also driven by the fact that Provenance’s native utility token, HASH, appears to be concentrated in the hands of Figure, the Provenance Foundation controlled by Cagney and his wife, and Cagney himself, per our review of the Provenance Telegram channel. This implies they control the network.

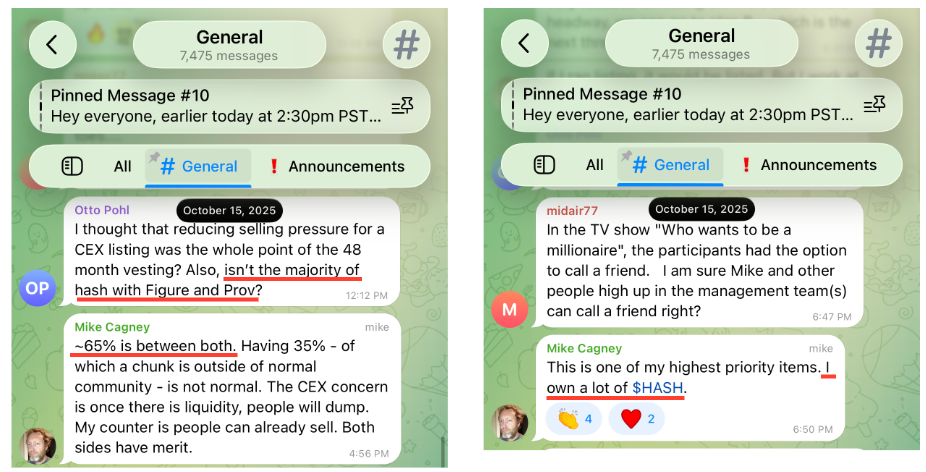

On October 15, 2025, Cagney said that Figure and Provenance together owned ~65% of Hash, while Cagney also stated that he owns HASH directly, saying: “I own a lot of $HASH.”[^1]

[^1] On August 6, 2025, Cagney posted on X, saying that Figure owns 20% of HASH supply. This implies that Provenance holds 45%. (1, 2)

Furthermore, Figure has financed the working capital and corporate expenses of Provenance. In 2022, Provenance, through a note, borrowed $5 million from Figure, “to assist with its initial setup of operations” and borrowed further for “ongoing working capital and other general purposes.”[1]

On January 21, 2026, Figure took over the responsibility of executing the community directives for the Provenance Blockchain Foundation, according to a press release issued by the company, but maintained that Provenance would remain “independent.”

Yet, despite this concentration and the association between Figure and Provenance, Figure’s CEO stated in an October 2025 interview: “Figure has about 20% of the tokens outstanding [HASH] … we are obviously an important player in the [Provenance] ecosystem but we absolutely don’t have control.”